With stock markets going highly volatile, equity market movements are not making sense, debt funds are facing defaults and downgrades in papers and schemes are getting wound up, in such a scenario, investors, especially the conservative ones are looking for investments with safety of capital and steady returns.

And why not, after all, safety has always been a primary concern of any investor, and if there are some options which can provide you some growth too, then it’s always wise to consider the same.

Also read: Follow the Lockdown rules, keep your investments safe

However, it is important to note that no investment is devoid of risk. Some sort of Risk will always be impacting your investments, you just have to be aware of the same and accept it. (Read: Types of Risks in Investments)

This post is about some of the Investment products which are considered safe investments, as in which are devoid of Credit and Default Risk.

Safe Investment Options in India

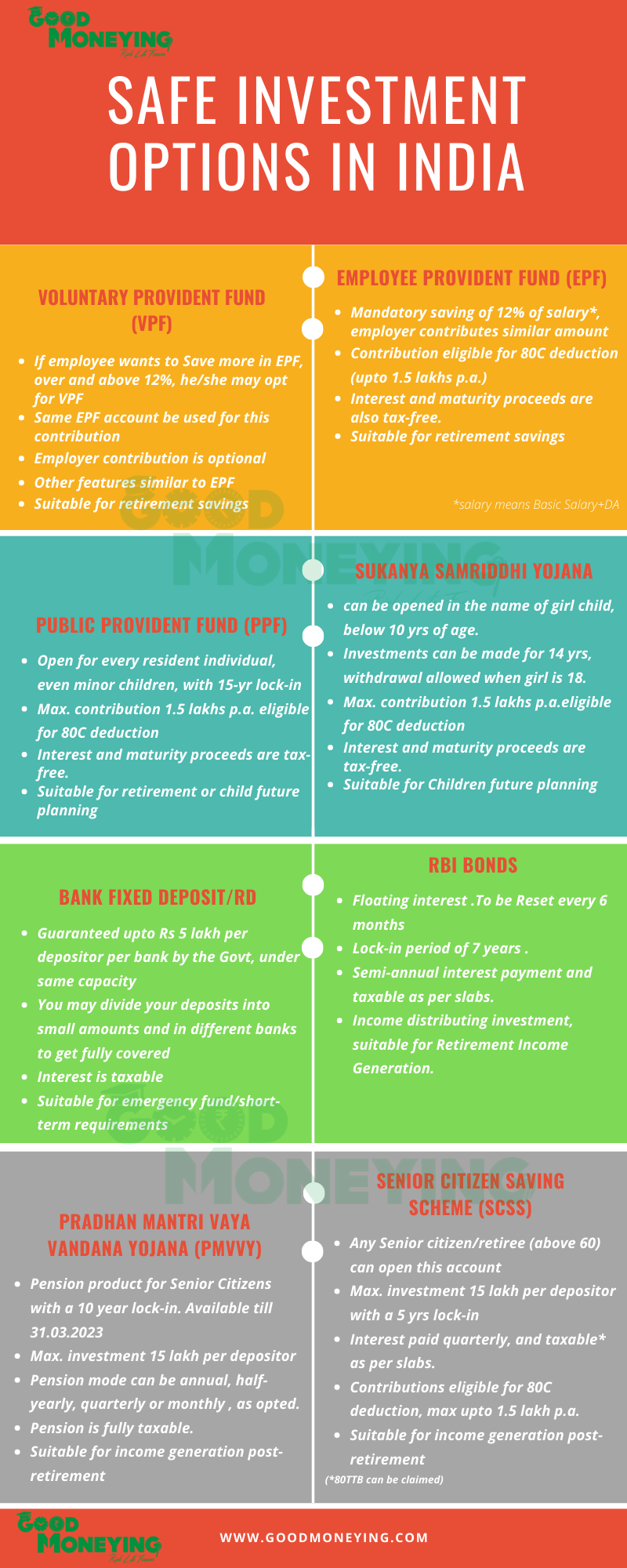

- Employee Provident Fund / Voluntary Provident Fund

It is the mandatory saving made by an employee, towards retirement. Under this scheme, a fixed percentage of salary (12% of Basic salary + DA) gets deducted from the employee and a similar contribution is made by the employer. The EPF saving generates decent interest which gets decided by the Central Board of Trustees in consultation with the Financial Ministry.

Also read: Read a detailed article on the EPF basics

The Rate of Interest for FY 2021-22 was 8.10%. The employee is entitled to the corpus along with the accumulated interest in retirement, that too tax-free.

However, due to the covid-19 lockdown, Finance Minister reduced this contribution to 10% for 3 months, may, june and july 2020, to give necessary liquidity in the hands of employees.

Premature withdrawal is possible in case of resignation and during the job tenure, but subject to some conditions. You may know more about these provisions here.

Employee contribution, upto Rs. 1.50 lakhs per annum is eligible for Income tax deduction under section 80C. Read more about Income tax deductions FY 2020-21 (infographics)

Government backing, fixed and tax-free Interest, tax deduction and tax free maturity proceeds makes it an attractive bet and also a safe investment option.

Seeing these features, if you want to contribute more than 12% of your salary, then you may do that by opting for the Voluntary Provident Fund (VPF). However, in EPF employer has no compulsion to contribute and maximum employee contribution is also restricted to 100% of the Basic salary.

VPF also carries the same features as EPF and the same rate of interest is applicable.

Budget 2021, proposed that interest on Employee Contribution to EPF/VPF beyond Rs. 2.50 lakhs per annum would be added to the total income of the individual and taxed as per Income-tax slab rates applicable, from FY 2021-22.

This Instrument is best suited for Retirement Savings along with Equity Mutual funds.

- Bank Fixed & Recurring Deposits

Fixed or Recurring deposits offered by banks are also a safe investment option, popular among investors, due to the simple structure and kind of guaranteed returns.

The government under the Deposit Insurance and Credit Guarantee Corporation (DICGC) Scheme ensures the bank deposits per depositor per bank (includes both principal and interest), in the same right and same capacity up to Rs. 5 Lakhs (w.e.f.) 4th Feb. 2020.

If the deposits are held under different capacities, then all such deposits are insured up to the upper limit (Rs. 5 lakhs). Read more on the Deposit Insurance Scheme.

Rather than going for a single FD of a higher amount in a single bank, divide it into smaller amounts and spread them across different banks and capacities to ensure all your deposits come under the deposit insurance limit.

The interest on fixed/recurring deposits is not tax-free. It is added to your income and taxed as per slab rates.

Also read: FD interest rates are rising in 2022- looking attractive again?

This can be considered for an Emergency fund and even the near-term goals when you do not find any suitable option on the debt side.

- Public Provident Fund (PPF) & Sukanya Samriddhi Account

PPF is also a very popular investment among investors, open for every resident individual. It has a 15- year lock-in, but premature withdrawal is permitted on certain conditions. It can also be extended in the block of 5 years. The government has made some changes in the features of PPF in Dec.2019. You can Open PPF in the name of Minor Children too. Read a detailed post (with infographics) on PPF 2019.

If you are a parent/guardian of a girl child below 10 years of age, then Sukanya Samriddhi Account can be opened in her name to save for her higher education or marriage. Investments can be made until 14 years from the date of opening of the account. It offers a 0.5% rate of interest higher than PPF. Read a detailed post on Sukanya Samriddhi Account.

Also read: Interest rates on PPF, Sukanya and other Small Saving Schemes are reviewed every financial quarter.

The maximum amount one can invest in PPF and Sukanya is 1.5 lakh per year and can avail deduction under section 80C. Interest and maturity proceeds are tax-free as well.

Further, since the interest earned and the principal invested is backed by sovereign guarantee, in both these schemes, makes them safe investment options.

These are the best suited Instruments for Children Future Planning. You may also use PPF to save towards your Retirement.

- Senior Citizens Saving Scheme & PMVVY

If you are a senior citizen/retiree then these two schemes can become a part of the regular income generating bucket in your portfolios. Any person above 60 years of age can open these accounts.

The Senior Citizens Savings Scheme (SCSS) has a tenure of 5 years and can be extended for 3 years. Pradhan Mantri Vyay Vandana Yojana (PMVVY) is a 10 years product.

The maximum amount one can invest in both the schemes is Rs. 15 lakhs. Contributions to SCSS are also eligible for tax deduction under section 80C.

Interest on SCSS is payable on a quarterly basis and in the case of PMVVY, it can be monthly, annual, quarterly or half-yearly as opted by the investor.

Interest is fully taxable as per the income tax slabs. But senior citizens are eligible for a deduction of Rs. 50,000 on interest income under section 80TTB.

Simple structure, assured returns and Government backing make both of these a must-have safe investment options for senior citizens. Read a detailed post on PMVVY.

- RBI Saving Bonds

Recently, after discontinuing the 7.75% fixed interest bonds, the Government introduced a new series of RBI Bonds, but with 7.15% floating interest, not fixed. It is also another safe investment option as it carries sovereign guarantee.

Interest would be paid semi-annually and the interest rate would be reset every 6 months. The issue of these bonds, opened recently on 1st July 2020 and comes with a lock-in period of 7 years.

The first interest installment would be paid on 1st Jan 2021 and it is taxable as per slabs. Read a detailed post on RBI Bonds.

This Investment Option is open for all, with no limit on the quantum of Investment. Since it’s an Income distributing investment, so better not to use it at accumulation stages like Children’s future or your retirement savings.

- NSC, KVP and other post office deposits

NSC, KVP and other post office deposits are also safe investment options. These are the oldest saving instruments in India.

NSC comes with a 5 year maturity and is eligible for deduction under section 80C. The Interest is compounded annually but payable at maturity, and the interesting part in this is that though taxable in itself, its interest payments will also be counted for tax saving under section 80C.

KVP is meant to double your investment after a predetermined period. It has a minimum lock-in of 30 months. Investments can be made in multiples of 1000 and there are no upper limits for investing in NSC and KVP. HUFs and trusts cannot invest in NSC and KVPs.

Other post office schemes include- post office Monthly Income Scheme, post office time deposits, and post office RD. You may read the features here.

Safe Investment options- conclusion:

These days, safety has become the prime concern of investors. Weak economic sentiments and low mutual fund returns and news of defaults and winding up of schemes and Covid 19 Pandemic has added to the concerns and investors are really not sure what would happen in future and when the economy would revive again.

So, in order to enhance the overall portfolio returns, these safe investment options should be a part of your asset allocation. Yes, the interest rates are low and fluctuating, some of them come with a lock-in period, and are taxable, but as they say “safety has its own risks”, so some you have to accept.

At the accumulation stage, you may also add some Gilt funds which invest in Government of India securities, and thus are devoid of Credit risk, but being a tradable instrument, and so are impacted by Interest rates movement and may make your portfolio bit volatile.

But I think that should be acceptable at the accumulation stage when you have many years in front of you. Fixed Income and Interest rate linked products without Credit risk can be a good combination for a long term allocation on the debt side.

So, in the end, though you may consider these safe investment options, but do consider adding these as per the asset allocation suited and the goals targeted. Do not spoil your portfolio and compromise with long term returns in the name of safety. Be in touch with a Good Financial Planner and select these instruments as per the advice.

Also read: 3 only reasons you need a financial planner

{kind=link}