Sanjeev (35), like many others, feel Equity is risky. He’s afraid of seeing RED in his portfolio, even if it is notional and for short term, and thus prefer to invest much of his savings into fixed return instruments like PPF, FDs, RDs, etc. Actually he’s inherited such behavior from his father who had always been wary of stock market investments. (Also Read: 6 safe investment options carrying sovereign guarantee)

Sanjeev has 2 Public provident fund (PPF) accounts, one in his own name and the other in his wife’s name. Last year he also opened the Sukanya Samriddhi account for his daughter. He is of the opinion that by using the partial withdrawal options in all his investments, he would be able to manage the major goals of his life. His father used to do the same thing in his working years.

But the recent changes announced in the Small savings interest rates space made him apprehensive about his goal achievement.

Moreover, he is also not sure if his strategy of depending on “TAX-FREE” fixed interest instruments would pay in the future or not. Budget 2016 provision of taxing EPF raised his doubts. Though the provision has been rolled back but it has shown the intention of the government.

He’s seeking the answer to “Is it possible to achieve long term goals by investing in the small savings schemes only?”

Well, Sanjeev’s apprehension is quite genuine. There must be lakhs of other investors who are feeling this way. Before dipping into the question, let’s first understand what changes in small savings interest rates have raised such doubt in his mind.

Since 1st April,2020 , the small savings interest rates has to be reset and notified every quarter unlike every year earlier. Every March, June, September, and December, revised interest rates will be announced.

Revision in small savings interest rates will be based on FIMMDA (Fixed Income Money Market and Derivatives Association of India) month-end Government Securities (G sec) rates for the last quarter.

Updated Small Savings Interest Rates :

Starting January 2023, the Government of India has changed the interest rates on some of the small savings schemes. The updated rates are as below:

| Instrument | ROI, w.e.f. 1st January 2023 | Revised ROI w.e.f 1st April 2023 |

|---|---|---|

| Savings Deposit | 4% | 4% |

| 1 Year Time Deposit | 6.6% | 6.6% |

| 2 Year Time Deposit | 6.8% | 6.8% |

| 3 Year Time Deposit | 6.9% | 6.9% |

| 5 Year Time Deposit | 7% | 7% |

| 5 Year Recurring Deposit | 5.8% | 5.8% |

| 5 Year Senior Citizens Savings Scheme (SCSS) | 8% | 8.2% |

| 5 Year Monthly Income Scheme | 7.1% | 7.4% |

| 5 Year National Savings Certificate (NSC) | 7% | 7% |

| Kisan Vikas Patra (KVP) | 7.2% (will mature in 120 months) | 7.2% (will mature in 120 months) |

| Public Provident Fund (PPF) | 7.1% | 7.1% |

| Sukanya Samriddhi Account | 7.6% | 7.6% |

Small savings Interest rates gets decided on G-Sec rates of the comparable maturity of specific schemes, plus a fixed spread. Spread is the extra rate which the government offers above the G-sec rates.

As per the recent changes announced, the spread remains the same as earlier in all schemes except in Term deposits of 1y/2y/3y, KVP and 5-year Recurring deposit. In these schemes spread has been reduced to NIL from 0.25%. The Government has tried to keep these schemes at par with bank deposit rates, so in future, its rates would be more or less similar to the rates being offered by banks.

Spread in Sukanya Samriddhi account is 0.75% and in PPF is 0.25%, and both follow the same G-sec maturity periods (10y). Thus, if for e.g. FIMMDA last quarter’s month-end G-sec rate was 8%, then Sukanya account would earn 8.75% and PPF would get 8.25% in the next quarter. Sukanya earns 0.50% higher than PPF.

But do remember that as per rules, whatever the new small savings interest rates announced will remain same for one-quarter only.

Besides, change in the Reset period and spreads in some schemes, the government has also changed the frequency of compounding in NSC and KVP. Earlier it was half-yearly and from 1st April 2016, it would be annually.

How are G-sec rates and Small saving schemes linked with each other?

You must be thinking that what is the connection between G-sec rates and small saving schemes? Why G-sec rates be taken as the benchmark for small saving interest rates?

Before answering this, let me ask you a question. Let’s assume you need a loan, and you have 2 options:

Bank A offers the loan at 8% and Bank B offers at 9%. All terms and conditions are the same. Which bank would you prefer? The answer is obvious, right?

Same way if Government can get a loan from the market through G-sec at 5.79% for 10 years term, why would it take loan from you through PPF at 7%? and every year or every quarter when the government asks for a loan and finds a new rate, then why would it want to stay fixed on a higher one?

Small savings is just a mechanism to borrow from retail clients, and since the government has some social responsibility towards country people, especially as in India where there’s no social security available, so, it asks loan from the public with some spread which in turn becomes a saving tool for investors.

The way interest rates have moved in the past, the government like all borrowers feel that the Floating rate is better than fixed.

(Also Read: New RBI Bonds 2020: Safety of capital, but interest is not fixed)

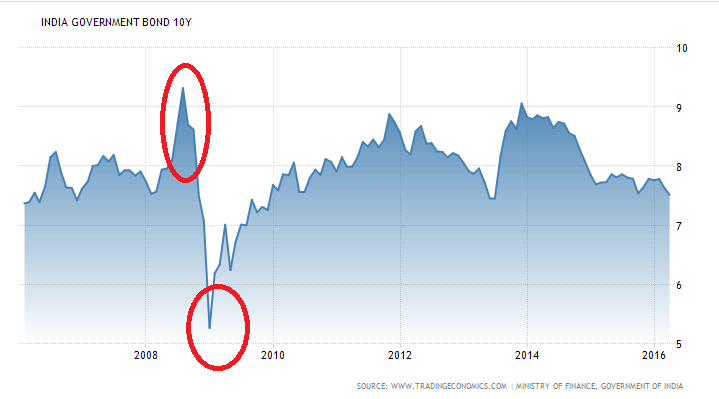

G-Sec rates in the last 10 years

G-sec papers come in different tenures – 5y, 10y, 20y, 30y. All tenures have different rates. G-sec market is more of an institutionalized, where papers are purchased by banks, Insurance companies, Mutual fund houses, PF trusts, Pension funds, PSUs, other corporates.

To manage liquidity, these papers get traded in the debt market. Depending on the Liquidity requirements, demand and supply, international factors, market interest rates, currency movements, these G-sec papers are valued and traded. Due to trading, the yields keep on varying on daily basis. Just like Share prices, these G-sec rates also move up and down.

The above graph shows the variation in “10 years G-Sec bond rates”, in the last 10 years. This will give you an idea, how volatile your small savings interest rates can become in the coming years.

From the above graph, it is easy to gauge that Period of 2008 – 2010 has shown huge variation. If the Small savings interest rates were G-sec linked in those days, then you could have seen PPF rates @ 9%+ in some quarter and also 5%+ in some.

What should Investors do?

See, since almost all the investment instruments have been market-linked now, so active management of the portfolio is what is required. Now from Active management, I don’t mean to go for trading or something, but you need to have such a diversified portfolio that you will be at the gain in all kinds of market situations. ( Read: How prepared are you for stock market fall?)

Regular revision of small savings interest rates may not impact much on close-ended instruments like Senior citizen savings scheme or National Savings Certificate, as once invested rates would get locked in. But for regular investments product like PPF and Sukanya, this does matter.

With the fall in G-sec yields, PPF interest would also fall, but you can benefit out of this by allocating some portion of investments to long-term Gilt Mutual funds. Interest rates and bond prices are inversely related, so when interest rates fall, Bond prices rise and vice versa.

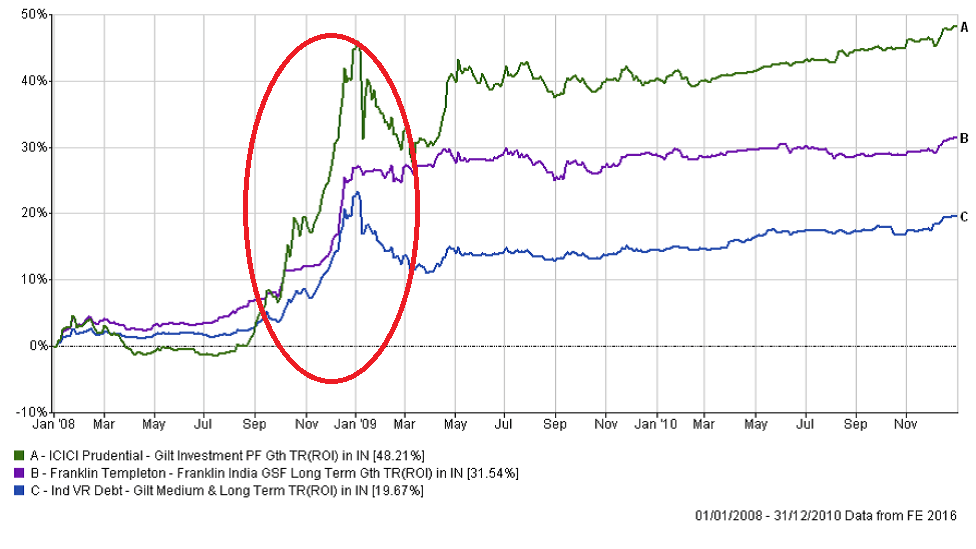

Just have a look at how actively managed long-term Gilt funds have performed during 2008-10 when we saw sharp movements in G-sec yields as per Graph shown above.

Below is the return graph of 2 of the popular Gilt funds during the same period

It is clearly visible, how long term gilt has performed in falling interest rate scenario. Now here, I am not saying that such situation may repeat in future, and neither am I saying that the referred funds in the graph above are worth buying.

What I am trying to point out, is to have a diversified nonrelated portfolio, so one instrument’s loss could be other instrument’s gain, so your goal achievement should not be hampered. When you are investing in PPF or Sukanya Samriddhi account with long-term view, do look at other long-term debt funds along with. And when your investment horizon is of short to medium term, through NSC or KVP or bank FD, you may also look at the same maturity debt mutual funds portfolio too. ( Read: Asset location is as important as Asset Allocation)

I know what you are thinking. Now you want to know, how to select Gilt funds? How much to invest in them and when? How can you sense which side Interest rates are going to go? And above all are gilt funds taxable? Right?

Well, if you are DIY (Do It Yourself) investor, then I am sure you will study hard and find out the answers, but if you are not, then better to have a financial plan first, so you can figure, what is actually required in your overall portfolio. Do you actually require gilt kind of fund or short-term portfolio that can help you.

This answers Sanjeev’s point too. No single product can help achieve goals; it is the combination of different unrelated products, based on your Asset allocation decided out of your risk profile and goals targeted, which needs to be there in a Portfolio.

Gone are the days of fixed interest rates for long term. I will not be surprised if you see these tax free instruments going taxable in the coming years. You need to have hold on to your money, your investments and should be sure why you are doing what you are doing.

Hope you find this article on Small savings Interest rates useful. By the way how you have planned to deal with these volatile products now? Do share your strategy and queries if any.

{kind=link}

This is an eye opener on PPF/SSY investments. Thank you.

Reg spliting up of investments between PPF and Gilt: Since if one raises and other falls, we should invest equally in both the products. Say 1.5 lacs is planned for SSY previously, but now onwards, 3 lacs to be planned and split between across SSY and Gilt to achieve the required corpus? Please clarify

Sunil, there cannot be one line answer to your question. Equal investment in Small saving products and Gilt funds, depends on your overall asset allocation required to achieve your other goals. This article is just to make you aware how things work and what can investor do. But should you do it or not and how much to be invested where totally depends on your financial Plan.

Sorry if its duplicated comment!

So if one is planned for 1.5 lacs p.a in SSY, previously for a girl child, now onwards he/she has to plan for 3 lacs and split across SSY and Gilt funds ? Please clarify

nice thought about new plans. keep sharing more updates. thanks for the wonderful blog post.

I’m having short term lumpsum investment goal say for 6 months duration. Will it be right to go with Short Term – Gilt fund say SBI Magnum – Gilt Short Term, being interest rate is softening

Can’t comment on specific fund. But yes, in falling interest rate scenario Gilt portfolio should be helpful. In my view long term portfolio would be better to gain better from falling rates.

how tax caliculated for nsc bonds

though the interest received is taxable but it also gets clubbed with 80C investments.

how to deposit in post office schemes online

To deposit in the post office schemes online you have to open an India Post Payments Bank Account. After that, you can download the IPPB mobile app through which you can deposit money in the post office saving schemes.

You can download the app from the link below:

https://ippbonline.com/web/ippb/mobile-app

Please let me know whether the interest rate of post office saving schemes (except PPF and SSY) is floating (every quarter or so), Or get fixed as per applicable rates at the time of invetsment ?

Hi Shubham,

The interest rates on Post office savings are fixed. This means you would get the same interest rate that you locked at the time of investment.