Here is a new safe Investment option for you. But this safe is a bit different as though it will provide you with safety but no fixed rate of Interest. To start with, this will give 7.15%, but only till Jan 1′ 2021, and will be reset every 6 months.

Also read: 6 safe investments in India 2020

Yes, RBI Bonds new Avatar, has got the features of Post office small savings, which also behave the same way and the rates will get reset starting every financial quarter.

Many Investors were disappointed when on 28th May 2020, 7.75% RBI Bonds (taxable) 2018 were withdrawn by Reserve Bank of India. The rate was fixed, guaranteed, and that too with RBI surety. Who does not want to be in that product when FD rates are going down, Mutual funds are getting wound up, and perceived risk of credit defaults are at peak.

Also read: What is Side Pocketing in Mutual funds?

Paying a fixed rate of interest for 7 years, in the falling interest scenario is not easy for anyone…not even for the Government. So, In replacement of these bonds, on 26th June 2020, Government announced the launch of another series of RBI Bonds namely, 7.15% Floating Interest RBI Bonds 2020.

But with the feature of Floating rate, does the Investment still make sense in New RBI Bonds 2020?

In this post, let us discuss the features of these new RBI Bonds and try to answer these questions.

What are Floating Interest RBI Bonds 2020?

These are Government of India savings bonds, issued by RBI. Unlike the previous bonds, which have a fixed interest rate, the rate of these bonds would offer a variable or floating interest rate. The starting rate would be 7.15% and would be paid semi-annually.

The rates would change every six months in line with the prevailing interest rates, which means the interest payouts would increase when interest rates rise and lower interest rates would mean lesser payouts.

Also read: Tools RBI use to manage Inflation and Growth

The benchmark for setting up the rate would be the NSC rate and a spread of 0.35%. The current rate of NSC is 6.8%, which is the basis of arriving at the 7.15% rate (6.8+0.35). Do note that NSC rates are dependent on Government securities rate and get announced every quarter.

The issue of RBI Savings Bonds 2020, opens on 1st July 2020 and the first interest installment would be paid on 1st Jan 2021. There is no cumulative interest option in this unlike the old RBI bonds (now discontinued).

Floating Interest RBI Savings Bonds 2020- some important features:

- Any Individual or HUF Indian Resident can invest in these Bonds. Investment can also be done through joint accounts and on behalf of minors. NRIs are not allowed to invest. However, the persons becoming NRIs after investing can continue with the same.

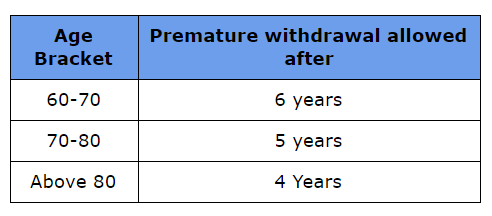

- These New RBI Bonds 2020, come with a lock-in period of 7 years. However, premature withdrawal is allowed for senior citizens as per their age brackets.

- The issue price of the bond is Rs.100. The minimum investment is Rs. 1000 and there is no maximum limit of investment.

- These Bonds can be purchased from SBI, other Nationalised Banks, and specific private sector banks- HDFC, ICICI, IDBI, and Axis.

- These are non-tradeable bonds and cannot be used as collateral for any loan.

- Nominations are allowed in the bonds and only legal heirs of the investor can inherit them.

Also read: Sovereign Gold Bonds – Why, What and How?

Floating Interest RBI Savings Bonds 2020- Taxation:

The interest received on these RBI bonds 2020 would be taxable as per the income tax slab rates of the investor. No other tax deductions are allowed on this investment. (See:Income Tax Deductions 2020-21- Infographics)

Also read: Old or New Income Tax Slab Rates: what to choose?

If the interest payout exceeds Rs. 40,000 in any financial year, TDS would be applicable.

Also read: How to avoid TDS on interest income?

Floating Interest RBI taxable Bonds 2020: Should You Invest?

First things first, these bonds do not provide any compounding benefit on the investment. It is just that you can generate income out of your investment, which is also not fixed, it would keep fluctuating. Also, the payout would be half-yearly and they come with a lock-in period as well.

So, the Government backing and better interest rates vis a vis other fixed interest Investments, makes these bonds suitable for risk-averse investors who want a secured income, without putting the principal into much risk.

These new RBI Savings Bonds may suit retirees or senior citizens as a part of their income-generating bucket, which may also include PMVVY, Senior Citizens Saving Scheme, etc, which offers a slightly higher interest rate of 7.4%.

So among the 3 parameters of selecting any investments i.e. Safety, Liquidity, and Post-tax returns, it looks good on the first one and Good enough on the second one if the other investments are well allocated and taking care of the liquidity aspects.

On the third front it may look fine today but if we understand that we are in a falling rate scenario, and may see 7.15% to reduce further after 6 months and more later, then this 7-year lock-in product may lose its attraction. (Also Read: FD interest rates are rising in 2022- looking attractive again?)

Still, if safety is your first priority and in these covid times, you want to ensure that, then go for the new RBI Bonds 2020.

Hope you find the Article on RBI taxable Bonds useful. Do share your queries in the comments section.

{kind=link}

A balanced approach. Like your diplomatic advice!!

An excellent and timely article, well written.

Do we have to pay any brokerage or any other charges to the bank/broker if we opt for these bonds?

No. You do not have to pay any brokerage on the purchase of these bonds.

If I cancel with in 1 year then what is the penalty rule. Will penalty will be on interst Or will i loose anything on principle amount in any case.

Hi Anirudh,

You are not allowed to cancel the bond. Premature withdrawal is allowed only after 7 years, for non-senior citizens and for senior citizens, in the age bracket of 60-70 are allowed after 6 years, 70-80 are allowed after 5 years, and for above 80 years it is 4 years.