This post was updated on May 25, 2020.

In the budget 2017 speech, the finance minister had announced that LIC will come up with a new pension scheme for senior citizens with guaranteed 8% return. On 4th May 2017, his words turned into reality and LIC announced Pradhan Mantri Vaya Vandana Yojana (PMVVY).

The Idea was to keep this scheme only for 1 year, but every year it has been getting extended. and with the last announcement the scheme is available till 31.03.2023

The PMVVY is an immediate pension plan scheme, similar to the varishtha Pension Bima Yojana launched in 2014-15. It’s a limited period scheme where you need to invest a lump sum amount and you will start receiving the pension income as per the chosen payment mode.

This post is about the Pradhan Mantri Vaya Vandana Yojana details, features, and review

Pradhan Mantri Vaya Vandana Yojana (PMVVY)| LIC Guaranteed Pension Plan

PMVVY is an immediate pension plan which earlier provided guaranteed return of 8% compounded monthly, means the effective annual rate is 8.30%, now the rate have been reduced to 7.40% w.e.f 01.04.2020. The rate remains fixed for the complete tenure once any investor enters into the Plan. The Next Revision of the rate (for the then new investors) will be on 31.03.2021

This plan is to answer and take care the requirement of monthly income for senior citizens. Managed by LIC and backed by the government, you can depend on it for safety and regularity of monthly pension aspects.

Here’s the Govt. Press Release dated 20th May, 2020.

Other important features of this government pension scheme are as below:

- This plan is meant for senior citizens aged 60 years and above. No upper age limit

- The tenure of the product is 10 years.

- The interest rate is fixed and assured at 7.40% monthly or 7.66% annually (In the beginning the scheme was launched at 8% ROI) and would be reviewed annually. However, investors in 2020-21 will lock the 7.4% rate for 10 years.

- You can ask for pension in Monthly/Quarterly/Half Yearly or Annual Mode.

- There is a lock-in period of 10 years, but in the case of critical/Terminal Illness of self or spouse, you can withdraw the money prematurely. In this case, Surrender value would be 98% of the purchase price.

- The Plan will remain open for subscription upto 31st March, 2023.

- The maximum limit of pension is applicable on per senior citizen and not on the family as a whole. Means if more than 1 member of the family has bought this plan, then they can individually invest in the same up to Rs 15 Lakhs and every member would receive monthly/annual pension upto Rs 10,000/1,20,000.

- No tax benefit on premium paid, and also the pension will be taxable. (Read 4 new tax benefits for Senior Citizens)

- On maturity of PMVVY, the policy holder will get the complete Invested amount (Purchase Price) back.

- In the case of the demise of the policyholder in between the policy term, the purchase price will be refunded to the nominee.

Also read: HDFC Life Immediate annuity Plan Review

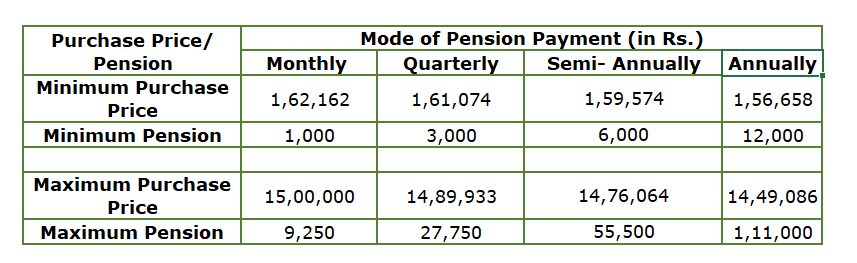

Purchase Price and Pension details | Government pension plan

The minimum investment in PMVVY has been revised to Rs.1,56,658 for pension of Rs.12,000/- per annum and Rs.1,62,162/- for getting a minimum pension amount of Rs.1000/- per month under the scheme.

You can invest any in between the minimum and maximum range. The below table shows pension amount you will receive with different deposits:

Pradhan Mantri Vaya Vandana Yojana| PMVVY Pension scheme – Should you invest?

PMVVY is a very simple pension plan. You invest the money and you will start getting a pension from at the end of the period as per the chosen mode of payment. Means if you have chosen monthly then the first pension installment will start from next month, if mode chosen is annual then you will get the first pension from next year.

It is the simplicity of the product, which makes it a decent investment option, especially in today’s kind of scenario when interest rates are falling.

Although the interest rate have been reduced slightly but when we compare it with other fixed income options available for senior citizens, for instance, SBI senior Citizen FD which offers 6.5% p.a. interest or a Post Office Monthly Income Scheme, which has an interest rate of 6.6% p.a., it looks on a higher side.

Also, risk is lower as it is backed by the Government.

(Also Read: 6 ways to generate regular income)

Since PMVVY is completely taxable and with long lock-in period, then one should be very sure before putting their money into it. Why am I saying this because any scheme announced by LIC always attracts a lot of eyeballs and without understanding the suitability of the product, people tend to invest in that.

People take the tag line – “LIC hai to kahi aur kyo jana” very seriously.

Senior citizens can also earn 7.4% in Post office senior citizen saving scheme, though that is not a 10 years product, it comes with a lock in period of 5 years. So, as of now both of these look like identical products, only difference is that in Senior Citizens Saving Scheme the interest frequency is quarterly and in PMVVY it can even be monthly, quarterly, half-yearly or annual and the lock-in period.

There are many Secured NCDs (though not backed by the government) coming in the market time and again and one can take advantage of the high returns they offer, some highly rated corporate FDs are also offering 8+% kind of returns to senior citizens, but higher returns come with higher risk as well. These can be avoided as far as the current economic scenario is concerned.

Many people may think that they can invest in the name of the spouse who doesn’t have taxable income, but then please note that such transactions attract Clubbing of Income.

And when taxation is the concern then one may look up to debt mutual funds. But important point here to consider is the quality of the funds. In the current siuations, not all debt funds are devoid of risks anymore. They have their own risk which was visible with the recent debt market events, defaults across various papers etc.

However, this option would be more suitable for investors in the highest tax bracket.

Also read: What is equity – It’s much more than just stock market Investments

How do you find Pradhan Mantri vaya vandana yojana (PMVVY), Guaranteed pension plan by LIC? Do you find it worth investing? Please share your views

Featured Image source: healthintelasia.com

{kind=link}

Policy period should be upto the age of 80/85 and not for just 10 years period.

Fixed income from this LIC Policy should be made available to the couple,separately as their earning potential in 70s and beyond will be negligible or possible only for a few

Great.Thanks for sharing.

nice post. it’s Really usefull

????

Informative, clear all doubts. Better options are also available. Thanks !

Agent’s name appearing in policy bond can make any fraud while getting back purchase price after 10 year maturity in pmvvy?

yes

Sir,

1) Is annuity earned on PMVVY is subject to TDS?

2) Is the final payment after the term of 10 years (Purchase price+Annuity for last year) is taxable?

If yes, is the whole amount taxable?

If not then under which sec. of I.T. act it is exempt?

Can I go for pmyvv now ? LIC office told that it is closed on march 31/20.

Pl inform me.

Yes as per the current information, the last date for subscribe for PMVVY was March 31st, 2020. But not sure, Govt. may extend it due to COVID- 19 situation.

PMVVY is an excellent plan for Senior Citizen. Security with reasonable hassle free income credited direct in one’s account is highly beneficial. I will opt for it .

Very good information shared, thanks for this.

You have shared a really good article, Thanks for this.