Updated on 15.03.2017

No Longer a new kid on the block. Religare health insurance which came up as a 4th stand-alone health insurance company in India after Star, Apollo Munich and Max Bupa, has no doubt given a tough competition to its rivals. Its first product Religare care mediclaim policy has led others in the league to change their product features to answer the competition.

This post is all about the features of Religare care health insurance policy and its comparison with the other similar products available among stand-alone health insurers.

Religare Care health insurance – basic features

Over a period of time Religare care features have become much more comparable to its other peers. Now a days health insurance policies majorly compete on the services rather than the product features. Let me point out some of the Important features in Religare care Health Insurance.

1. Lifelong Renewability.

After Apollo Munich and Max Bupa, Religare health Insurance also has come up with Lifetime Renewability, through Religare Health insurance –care.

2. Wide range of sum assured – up to Rs 6 crores.

Religare care has different versions in its plans which offer different sum assured. It has feature of providing higher cover to get treatment outside India also. Maximum cover you can get in Religare care is Rs 6 crores.

3. Annual Health check-up for insured members – regardless of claim history

All Major policy members can get the annual health check up (Pre-defined medical tests) done at authorized medical centers Free of cost.

4. Automatic Policy recharge if the claim amount exhausts the current coverage.

Religare health insurance Care, when launched broke the monopoly of “Apollo Munich optima restore” with this feature. But practically Recharge and Restore have different workings and recharge is much better.

5. Co-payment –

If someone is above 61 years of age, and buying Religare care for the first time then S/he has to bear with this copayment feature and pay 20% of the claim amount from own pocket. However if looked upon or compared with other insurers, which don’t offer covers to this age group 20% copay is not a bad feature.

If you are looking for health insurance for parents, then Religare care can be a good choice. Else you may also look at some health insurance policies as offered by nationalized banks like PNB oriental Royal mediclaim or canara apollo munich plan.

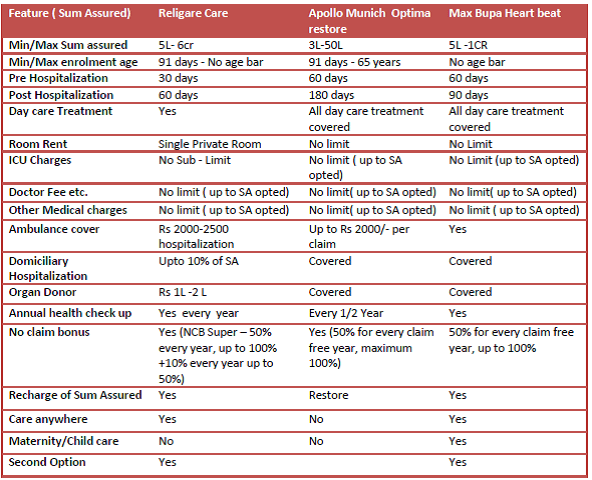

Religare Care – Comparison with Apollo Munich and Max Bupa

Should you Buy Religare Care Health Insurance?

As i said above that now days you will find much similarities in product features, its all about customer servicing now. And customer servicing is something which can not be judged sitting on the sidelines. you need to dive in and have to have practical experience with the services to make an opinion about the same.

Due to Portability provisions available, every other company knows that if they do not provide better services customer can move to other insurance company easily. So service quality has improved a lot in last few years.

Health insurance policies should have lesser conditions attached to keep it simple for the insured. Religare care looks like a simple policy. Those who wants to buy a fresh policy can have a look at this. This has a mix of many popular features like the recharge of sum assured, Free Annual health check up etc. which makes religare care worth considering while searching for good health insurance policies. For the lower sum assured like below 4 lakh Room rent limits may be a deterrent, but for higher sum assured this product looks suitable.

Do share your opinions or experience with Religare care in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

i think the Ambulance cover starts from 1500 and goes upto 3000.

Agree. It ranges from Rs 1500/- to Rs 3000/-, depending on the coverage amount.

Thks manikaranjee for update -However we need to check the premium comparison too for different age Groups.

Thanks anil ji. Sure. Premium calculation is must to check the affordability aspect. Premum calculator is very much available on Religare health insurance website.

why star health is not in comparision chart

Rajni, actually at the time of writing article i was not aware about star’s new launch.

Readers, Star has also come up with a comparable and decent health insurance option with the name “Comprehensive”.

but in Star Comprehensive” plan star will load your renewal premium because you claimed or fell ill after taking policy.

and Star only providing 101 Day-care treatments in Comprehensive” plan. but in religare or other campny providing all day care .

Star Health Insurance Company just here to make money out of innocent people by showing their attractive rate cards. Star Health is never concerned us and the loss we had to bear by opting for such a pathetic company. The sales reps just try to grasp you in buying the policy and later when the policy holder is admitted they try to turn their backs.. ! They just try to find stupid and baseless reasons to deny your claim and even don’t reimburse your expenses..!

The worst part is the people handling your claim are senseless bloody MBA guys and not educated people who would understand better..!

Please never opt for Star Health, I myself am a victim here…!

Star health and Indian Health Organization are two companies with worst reputation, be away from these crooks as much possible.

Raghu, you seem to have a bad experience with these 2 companies. Do you want to share it for the benefit of other readers?

between star comprehensive and religare care health insurance policy, which one is a good policy (in terms of service and benefits, premium not a constraint).

For now i would say you should wait to go with Religare as the ownership and management is going to be changed since Religare Health has been sold out. So it may or many not lead to service issues…only time will tell.

Bought a policy online from religare health insurance website for myself and my two kids. The site does seem easy to use and they gave an instant policy….

Thanks for sharing your experience. Hope religare people to be this fast even at the time of claim.

Thanx hina for ur comment i am also planing to take policy for my family so r u satisfied with religare health insurance?

Is religare good enough to be trusted…I’m willing to buy a floater for 5 lk but very confused with apollo optima ..max Bupa ….my primary concern is to get good support and claim at time of incident……who can be trusted more out of these3

No one and every one. See, you cannot be sure of service standards sitting outside. There are both good and bad experience in the markets which you can hear from different client reviews and stories. Religare has a decent track record now and got a good exposure in the market. I feel that a company should be old enough so it has seen decent number of claims to make opinion on. When it was launched in 2012, i was a bit worried to recommend it to some one, but not now.

To me all 3 you have mentioned are same

Can I go for a mediclaim for my father whose age is 68?

Is pre-existing diseases covered?and what is the waiting period?

Yes of course

Read this

http://goodmoneying.com/insurance-planning/health-insurance-for-parents

Pretty simply htealh care is more than extremely expensive. Just routine testing which should be done on a yearly basis is very necessary in preventative care and at the same time very expense without htealh care insurance coverage. I work in a Laboratory and do the billing. It’s incredible! Even if you have a htealh care plan that requires such things as deductibles and co pays and employee contribution, it still is worth every penny when you are ill and need medical treatment. Of course there are a ton of variety of plans out there that cater to different needs. Therefore it is always wise to do your research if your employer gives you options in htealh care plans to choose from.

Respected 2 all,

I have a 3 options..

1.max bupa heart beat plan

2.apollo munich easy health care

3.Religare health ‘CARE’ plan

My age is 21.

Suggest me.. Iwant to get health insurance…if i compare the premium of these plan,religare has 2300 rs. Premium..

never buy insurance from any private company specially from Appollo Munich claim settlement ratio is 65.59% very low), these companies always hide required information from customer, Appollo Munich have increased the premium recently upto 40% by taking permission from IRDA, and according financial planners for a sum assured of Rs 3 lakhs at age of 60yrs the premium will be as below

according to company after every 3 yrs (may be every years according to policy terms) apollo munich will increase premium to 40 % and let us make calculations for sum assured of 3 lakhs at age of 33 yrs premium is 10000/- approx, if ur aspect-ed age is 80 years

total number of yrs for premium 80-33= 47 years

total number of times premium increases 47/3= 16 times

premium increases 1st time 40%> 10000@40%= 4000/- total premium of next 3 yrs= 4000+10000=14000/-

and 2nd time increase in premium 14000*40% =5600/- total premium of next 3 yrs= 5600+14000=19600/-

and soon… upto 16 or 17 times in ur life

in addition to this regular premium increase according to age group 36 to 45=5000/-

46 to 50=7000/-

50 to 55=23000-/-

56 to 60=32000/-

61 t0 65=70000/-

Now gross premium paid by you at age of 36=4000+10000+5000=19000/-

after 3 year with 40% increase in premium to 39 5600+14000+7000=26600/-

and so on……….

at age of 60 years ur gross premium may be= 2.7 lakh for a sum assured of Rs 3lakh and at age of 75yrs premium may be 6 lakhs for sum insured of rs 3 lakhs

this is how apollo munich optima restore plan lot the Indian people by a other country company

and also optima restore option will not act effectively at that age and no other company will give u an option to by any other plan.. its premium increases exponentially after age of 45 years

If u want to buy 2 lac S.I. then you should go for apollo easy health (2843) bcz there are no limit in room rent & ICU as well as other benifit like religare 1% for room & 2% for ICU bt u can Think about Religare 5 lac bcz your prm will be 3313-/ only and u will get 1 free anual health chekup also.

Regard.

[email protected]

trying to find answer of 1 query –

In religare’s ‘CARE’ plan, it has a feature of automatic recharge which is equal to the original SI which customer has opted in the beginning. suppose if i go for this plan along with spouse for 5 lac SI, and whole amount exhausts in the treatment of one of us, does additional recharge will automatically come into the picture and cover all expenses beyond 5 lac Rs.

OR

the recharge is applicable to rest of the family members only and an individual is limited to 5 lacs only i.e. SI.

further,

if 5 lacs is consumed completely in the illness of one family member, do others are eligible for remaining 5 lacs, or its just one additional treatment above 5 lac Rs for any amount (and not multiple treatments)

Do let me know if my query is difficult to understand

Dear Ashish,

With regards to your query please find the respone below

Benefit of Recharge of Sum Insured is available only once in a Policy Year and cannot be claimed for the same ailment by the same insured. Further it is clarified through an illustration as under:

a. Mr. A, his wife and his son are covered under a 5 Lac floater policy in CARE.

b. In case where Mr. A is hospitalized for heart ailment and entire 5 Lac is exhausted, then additional 5 Lac would be available to all the members (Mr. A, his wife and his son) under recharge.

c. The 5 Lac of recharge cannot be used by Mr. A for any hospitalization related to any heart disease or similar condition. However, Mrs. A and son can claim even for any heart related ailment.

d. The 5 Lac of recharge is available and the members can claim as many times as required up to 5 Lac.

For further details, we request you to read Benefit 6 of Policy Terms and Conditions.

http://www.religarehealthinsurance.com

Incase of any further query please feel free to get in touch

Vikram

I have been trying to get a policy for my parents aged 54 years.. However, I am too confused with so many policies.

I have shortlisted two companies:

Religare

Apollo Munich

Both policies are having almost the same benefits with Religare being a bit better. However, I need to know the claim settlement reviews.. They may offer awesome benefits but at the end if I do not get a claim then it is all useless.

Please help me in this regard.

Thanks,

Mayank

Mayank, as far as claim settlement is concerned , being a new company Religare does not have that much experience…so can’t be commented on. Apollo Munich has a good claim settlement ratio, so it would be better for you to go with apollo. If you feel religare features to be good then you may try to switch your insurer next year by opting for portability. Till then we can easily figure out the claim experience of religare too.

Thanks for the reply.. Would you like to comment on Max Bupa’s Health Companion Plan? They launched this plan to compete against apollo munich… premium comes out to be around 19k for 2 adults aged 54.. no day care exclusions.. Am I missing anything or Max Bupa’s is better?

Max bupa’s product is also good. But i don’t like 2 features in their product

1. rather than increasing sum asssured as a no claim bonus they offer some shopping vouchers of different brands. I personally feel that the way medical costs are increasing one cover should also gets increased, and No claim bonus is one way of supplimenting the cover.

2. Second point is that in max bupa policy there’s a clause of Co payment(20%) after 65 years of age. Though this does make the premium cheap as compared to other one’s but this the buyer has to decide. whether to pay high premium or go with co payment clause.

About the co pay, as far as I know, there is a co pay if the entry age is 65+. If I take the policy now and keep on renewing it then I guess there would be no copay.

Could you give your suggestion as to which out of Max Bupa and Apollo Munich is better in terms of hassle free claims, exclusions etc. (assuming similar premiums for both and ignoring the no claim bonus).

No Mayank its not like that. The feature that you are referring to is in Religare and not in Max Bupa. In Max even if you buy the policy today and keep on renewing it till 65 years, still you would have bear with Co pay after 65.

As i said earlier…i have experienced claim procedures of both – apollo and Max and could not find any difference. To me both sounds OK.

Thanks a lot! I missed the co pay fine print!!

Max bupa out of the equation now.. 🙂

Ah.. the painful research has to start again to compare some policy with Apollo Munich and to find out if it is really worth it..

Hi,

How would you rate ICICI Pru Health Saver compared to Apollo Munich??

replying to my own query for the benefit of others.. ICICI pru health is just a way to fool people.. rather invest your money in mutual funds separately..

These people take your money and invest in their own MF, which you cannot use for 3 years..

also the use is limited for the use in health claims only..

moreover they are charging very high fund management fees..

In short, they are trying to increase the fund AUM by policies like these.. risk of which is borne by the buyer himself..

Thanks for pointing these out Mayank. I will write a product review on icici pru health saver very soon.

Sir, supoose i am having religare health policy and after policy within a month i need to go for any type of surgery . will then it will be covered by the religare or i have to bear all the hospital expenses …

Ashwani, if this health issue is pre existing then you have to bear expenses from your pocket but if not then you can claim the expenses from the company.

Thankyou sir.

Sir i had already taken the religare policy of 5L, plz tell me that whether my decision was right towards taken the religare policy or not?

Hello Sir,

I am planing to buy a Health insurance of 3Lac SI for my family…. want to know which one is better Apollo easy Health standard/ religare Care..

Sumit…in comparison definitely Religare scores over Apollo…but do keep in mind that religare does not have much claim servicing experience.

thanx sir…. but religare is new company… in the field of insurance…. how about optima restore by apollo as compared to care…. the plan seems to be same… as it seems to me… plz do let me know

which one is Better Reliagare Care / Apollo easy health for 3lac SI

Kindly suggest a policy for my family between Apollo munich , max bupa and religare . Sum insured looking is for 15 lacs. Kindly suggest

Rajeev, there’s no specific comparison which leads to the selection of the policy. As per me all these policies are almost same as far as basic features are concerned . Personally i have had bad experience with max bupa on services. Also the feature of not giving no claim bonus and having 20% copayment after 65 years of age makes the max policy less attractive. I find Religare as a mixture of Apollo and max, but since this is a new company so one may want to give it sometime to settle down and experience some claims too. Apollo has a strong underwriting and standard waiting periods.

I would advise you to go through the specific policy brochures and select as per requirement.

Religare, on it’s website states that there shall be no loading on premium payable because of claims made (premium may increase because of age but shall not increase because of claim made).

However, it is silent on this in the policy document. It only states in its policy document that it may, at it’s sole discretion, revise the premium.

What are the IRDA guidelines on this issue (claim based loading of premium). How can I ensure that what Religare is writing on its website is followed by it.

Thanks in advance for your response.

harsh if there’s nothing of this sort mentioned in the policy wordings then you may write to religare customer care and get the clarification. and if at any time during renewal they increases the premium due to claim made than the reply from customer care would be the suitable and sufficient proof with you.

Kindly suggest me one ideal policy for my family out of appollo or religare for sum insured of 3 lac in comparision of all features available of these.I am very much confused about it.please give me the reply as soon as possible because I want to buy it in these one or two days.

Thanx

Well Rajan, I encourage you to go through both company’s policy wordings or product brochure. There are some features on which religare is better than Apollo. But as apollo is comparatively old company and has a good claim servicing ratio so from other angle Apollo seems to be good. There’s nothing good or bad, choice is purely personal.

Sir leave all the matter and just put your finger only on one policy which is suitable for my family of four members, two at the age of 40 years, two kids at the age of 10 years. My family is just a mediocker family,so just taken into care pros and cons of all the policies, just name any one out of all.

Rajan, i believe that though religare is a good product but looking at the experience of the company and product, you should go with apollo. Later on…sometime next year or so , if you feel like porting to religare you can do that…and till that time market will also experienec more of religare servicing.

I agree with Rahul. We should give more time to Religare to prove its credibility.

SIR

IS THERE IS NO PLACE FOR MAX BUPA IN COMPARISON TO APOLLO MUNICH?

Rajan, that’s why i wanted you to go through the fine print of different plans. There should not be any doubt left after purchasing the policy.

Hi All, I’m 23 years and I would like to go for an health insurance for myself. Please suggest good companies for the sum of 3 – 5 Lacs.

Hi Manikaran,

I’m confused between two policies for my mother who is 59 years old

1. Apollo Munich Easy Health (5 lakh cover) + Apollo Munich Top Policy (Rs 5lakh) – Top up because the premium is low with a deductible of 5 lakh

2. Religare Care (Above 5 lakh cover)

From what I’ve heard you say is that Religare is a new company so servicing still not sure.

So does it make sense to go for Apollo Easy Health – 5 Lakh cover + Apollo Munich Top up Policy of Rs 5lakh.

I’m aware the top up will not work like Religare Care.

e.g. being if I make a claim of 7 lakh then 5 lakh will be contributed from Easy Health and 2 lakh from Apollo Top up policy

and in Religare 7 lakh from Religare Care plan.

But now if I want to make another claim of 2 lakhs, it will not be possible in Apollo, even though my top up of 3 lakh is left because the deductible is 5 lakh.

And this is where Religare Care will come into the picture.

So Manikaran you will suggest Apollo because we have some history to go by right..

Thanks,

Ravi

which is the best product out of Religare “CARE” & Appollo “Restore” for 2A(32&30yrs) +1C (1 yr.). what is the difference between restore(appollo) and auto-recharge(Care)? which one is more advisable and best to opt. please guide……

thank you.

The Religare CARE policy – clause 5.5 (ii) – clearly states that if a room/ICU acco has been opted for that is higher than eligible limit as applicable, then variable medical expenses shall be pro-rated as per applicable limits. i.e. If your room / ICU rent is higher than the 1% / 2% of SI, then all expenses such as doctor’s consultation, tests, procedures – everything – will become pro-rated. Further accrued bonus does not account as SI for the above purpose (as per clause 2.1).

As per my interpretation, if your room rent is 5,000 and limit is only 2,500 – ALL other costs will be paid only at 50% of actuals. My current New India policy has a similar clause and this is how they have applied it.

So it is not strictly correct to say Religare has no sub-limits. I also do not like that this clause is hidden in the fine-print… I would rather prefer Apollo or Oriental – who place no limits or pro-rata clauses on non-room-rent expenses.

I LOVE RELIGARE, BECAUSE I TOOK POLICY FROM RELIGARE, NOW , I AM NOT WORRY ABOUT MY HOSPITAL EXPENSES.,

hi mr. manikaran,

first of all nice initiative. i have a employer insurance of about 4lacs for us family of three.and 2lacs for parents.over and above that was planning to buy new policy.i am 35 wife 32 and 2.5 year old daughter. i also want to add my mother 59years to the list.i have thought about apollo and max…i am open to other suggestions.also let me know about top up plans.since i will be claiming in company first is having fresh policy suitable as i will be submitting my documents in company policy.

regards

amar

Thanks Amar.

This is a wise thought of getting a separate cover in addition to the employer’s provided cover. One should never be dependent on employer for his personal responsibilities.

Regarding policy, you may not be able to add your mother in the same policy which you buy for your immediate family. There are few policies which allows the addition of Parents in the same plan. Max bupa Family first is one of them.

http://goodmoneying.com/financial-planning/max-bupa-family-first-review-2

In the age of 59 there’s complete universe of policies available for your mother. Max bupa has only one feature which personally i don’t like which is co payment after crossing 65 years of age. But otherwisse the feature of annual health check up is an attractive one in this particular age group.

Top up policies comes with a fixed deductible, (3 lakh, 4 lakh or 5 lakh). Whatever is over and above the deductible will be taken care by the insurance company.

In nutshell, no policy can be called as best …you have to understand the features and select as per premium affordability. Go through Apollo, max, Religare or icici. Even national and oriental has comparable policies.

hi there

thanks alot mr. manikaran.but is it advisable to go for a top up kind of plan or a entirely new policy? will i be able to further claim after exhausting my company limit or will it be a problem in fresh policy?in apollo do they have a top up option? incase they have can we convert into regular plan in future? ii know thats a lot of q? but can’t help it.

regards

amar

Amar, top up plans helps in extending the cover at less cost. Thus if you are looking for a big cover , which sometimes is not available in your choice of product…you may buy a top up plan to enhance the coverage. You can claim from your separate policy after exhausting your company’s coverage or even without claiming from your company’s policy. But the same amount can’t be claimed from both.

Apollo do have top up option. But amar, its better if you first understand the difference between top up and super surplus policies. Top is what apollo offers, super to up is with United and HDFC.

Religare does not have any critical illness rider, so which company has a critical illness rider?

Critical Illness rider is available with apollo munich only. But you will find stand alone critical illness policies with all general insurance companies.

Standalone critical illness cover very few are offering as current age is 59.

Also the premium is quite high.

Well Ravi, don’t expect critical illness rider/policy to be cheap in this particular age. Mostly CI policies expires at the age of 65 -70 i.e mostly companies don’t renew CI policies after 65-70 years of age, but Max bupa has one policy which continues with the cover after this age also

http://goodmoneying.com/insurance-planning/max-bupa-health-assurance-product-review

CI policy will come into effect once patient gets diagnosed with a particular defined illness with specified severity. I am always of the view that rather than having a CI policy one should increase the hospitalisation cover and maintain a savings fund specific for CI .

http://goodmoneying.com/insurance-planning/critical-illness-policy

HI Manikaran,

Good initiative taken!!

Myself Pavithra, I wanted to take up health insurance policy to my parents and was doing research and their found this article…..

Lot of confusion I had in my mind!!

My parents had met with an accident, they have undergone surgery and its been two years now. Dad gonna step into 60yrs this August. Planning to take Religer SI 5lakh package.

Please suggest.

Pavithra

PS: Once again Keep up the Good work Going!!!

Pavithra…thanks for your appreciation.

As your parents had undergone a surgery so you may face exclusion or pre existing clause for this particulr treatment in any policy you buy for your parents. As they are below 60 years of age, so you may also look at the features of other policies too like apollo, max, icici etc. which are more experienced than Religare.

Hello everyone,

I want to buy a comprehensive health insurance policy for my father (59 yrs, 9 months), mother 50 yrs, and younger brother (24 years). I have done lot of research while going through plans of various companies, but still i am totally confused, which one to go for? ‘Religare care’ and ‘Max Bupa Heart Beat Family First’ seemed to be ok to me now. My main concerns are Critical illness coverage, life long renewal and hassle free claim settelment . Religare seems not to have critical illness coverage. In Apollo Munich i found too many exclusions compared to others. Based on your experience and knowledge, please help me selecting a better health insurance policy.

thanks and Regards

Gaurav, i would advise you to understand the Critical illness policy features first.

http://goodmoneying.com/insurance-planning/critical-illness-policy

Hi sir,

My name is Vinayagamoorthy ( age 41 but my passport mentioned age 47) I’m currently working outside of India, but my family they are in India, I lake to take for them the best health insurance policy, they are four members, my wife age 39, and my three children is age between 11 to 16, kindly suggest me witch health insurance policy is best for them, And also want to know I can joint with the same policy, even I’m out of India.

As i always say, there’s n single health insurance policy that can be called as best. Also, almost 80% features are nowdays same in most of the policies. Better to have a look at some of them. I would like to you see apollo munich in standalone health insurer, ICICI Lombard in general Insurance policies and Oriental happy family floater in Nationalised health insurer. and then decide as per suitability.

Yes , you can also be part of your family’s policy, but for that you need to be present in india. Also pls note that you will not be able to claim such policy outside india.

Hi Manikaran

As per my understanding on top of health insurance, its advisable to have a critical illness cover as well.

In that case if I go for an HI SI of 10L with Relgare Care, which product should I go for a critical illness cover?

Regards

Karthik

Karthik, personally i am not in favour of any Critical illness policy. I may be wrong. But the reason of my objection is the policy wordings of CI policy. It says that diagnose of illness is not enough, but it should be of specific severity. And in that severity i don’t think anyone will be able to survive or can be treatment out of hospital. So in both cases, as the stay in hospital is going to be longer, so better to have a extensive hospitalisation cover.

Its better to do some savings and keep it as medical corpus for such kind of medical condition. Till the time you don’t accumulate such amount, you may take CI cover.

http://goodmoneying.com/insurance-planning/critical-illness-policy

I am 52 and my spouse is 51 now; Can I take Religare Care Policy for myself and spouse online ? shall we need to do any medical test for same?

Hi,

I am 29 years old and I am looking for a good coverage, preferably 20-25 lacs. I am bit confused between religare and apollo. my query is about auto-renewal, Lets say someone got a policy of 25 lacs (auto recharge)and he consume 24 lacs in 8-9 months and after that in 11th month he undergoes hospitalization for 3 lacs, Now my ques is “will i have to pay rest 2 lacs by my own or it will be covered under the policy”. I want to know the exact meaning of “exhaust” in the policy term which both religare and apollo are telling.

*If due to claims made, you ever exhaust your health cover, we reinstate the entire sum insured of your policy, in the policy year. All this at no extra cost! …… RELIGARE

*Automatic re-instatement of the basic sum insured, if the basic sum insured and multiplier benefit has been exhausted during the policy year. ……. APOLLOMUNICH.

Thanks

Its a very good point raised Kuldeep. See, this feature is different in apollo and religare. Answering out of your example…in case of Apollo, on second claim, only 1 lakh will be paid and balance to be paid from own pocket. Now as the complete basic cover has been exhausted , so if there comes another claim of Rs 2 lakh in the same year then it will be paid from the restore of cover amount.

In case of Religare, it is different as if the second claim itself crosses the basic limit as you have mentioned in your example…full claim will be paid. part from the basic limit and part from the recharge limit.

But do note in both the cases recharge/restore amount will be paid only when the claim is for illness other than already claimed for.

Hi, I guess you are right in advising readers not to go with the new player. Your reason was that the company’s not that experienced in health insurance space , but i feel that for new company and especially like religare which doesn’t have that big standing in the financial market (be it religare securities, religare mutual fund etc.) one should be more cautious.

You need time to understand the product features too, as…. they say that all that glitters is not gold, and the same thing applies in this product too. So many good features and as you rightly said that this is a mix of apollo and max, are enough to raise doubts on the product.

I would like you to go through the Policy wordings – page no. 2 – 2.1 (hospitalisation benefit), specially 2.1 (c) iii)…This clearly tells that there’s sub limit of 25% on the surgeon’s fees.

The definition of Single private room is also ambiguos and creates doubt that whether my complete claim will be passed or not.

Hi, I am little bit confused to compare between Religare Care and Apollo Munich Optima Restore. I want to buy policy of Rs. 3 L. Please suggest me, which is best?

Besides this all these companies are new in Market as compare to government insurance policies. How much faith we can keep in these private companies.

Why government companies cannot give best service than private even though they are very old in Market?

Sir, i want a hospital cash benefit plan with daily cash of rs 1000. can you suggest me a good plan and also my options….

This specific benefit is available with mostly all life insurers health policy. better to chk with them- LIC, icici pru etc.

DEAR SIR WHICH HEALTH INSURANCE PROVIDER IN INDIA IS HAVING BEST NETWORK HOSPITALIZATION WITH THEM AND HAVING VERY GOOD CUSTOMER GENERIC APPROACH TOWARDS MAKING CLAIM.

I M AGED 26 AND FROM LUCKNOW(UP) LOOKING TO BUY ONE INDIVIDUAL HEALTH PLAN I HAVE SOUGHT TWO PLAN

1-APOLLO OPTIMA RESTORE

2- ICICI LOMBARD COMPLETE HEATH COVER

OTHER THAN ABOVE TWO IF YOU CAN SUGGEST SOME OTHER COMPANIES ALSO WHICH HAVING GOOD NETWORK HOSPITAL AND HASSLE FREE CASHLESS FACILITY WHENEVER CLAIM RAISED. KINDLY SUGGEST

Mohd, it very good that you have understood the importance of health insurance in such a young age. It will definitely pay you in future.

See, as far as network hospital is concerned, it is very difficult to find out the best networked health insurer, almost all insurers has same kind of hospital list. I would encourage you to go through the list after zeroing on the policy. I mean , this network keeps on changing. Hospitals comes in and go out without intimating to the insured. So this should not be the only criteria while buying policy. Apollo and ICICI , both has decent policies with them, with one major difference that icici has a provision to increases your premium based on claim ratio which apollo won’t. You may also check out policies of Religare and max bupa. I believe that one should go with a company which has in-house claim settlement, their claim servicing is much better (as far as i have experienced)

Dear Mr. Manikaran Singal,

I am 55 and my wife is 49 years old. We are currently covered under corporate health insurance provided by my company. I have been taking medicines fro hypertension and high cholestoral for the last 15 years and my wife has been taking medicines for high cholestoral. I would like to by a health insurance plan to cover us after I retire at 60 years.

I will be grateful to you if you would suggest the best/most suitable cash-less plan for us.

Best regards,

P.Verma

Mr Verma, based on your health condition and age, you should be prepared for the loading which insurers might charge on your premium.

Without considering premium which in any case is going to increaese with increase in age and Sum assured, and keeping in mind with the policy benefits, i believe you should look at Religare care , Apollo Munich Easy health. Though policy of max bupa is also good, but due to the condition of Co pay after 65 years of age, i don’t prefer it for old age people. You may also look for Topping up your policy with “Super surplus” policy if you want to go with less sum assured in your base policy.

I request for your observation regarding Religare’s claim settlements since they are now in the health insurance market for over 2 years

Hi Manikaran,

I am 35yrs old and looking for health insurance for my family under family floater plan. My employer and my wife employer are both giving us insurance but still we would like to go for it.

After all my researches with icici, apollo, max and religare, i have finalised two of them viz, apollo optima restore and religare care for 5L SI.

Now i am little confused in finalising between these two. cos when it comes to recharge option, premium amount, higher SI(may be useful at later stages of life when medical expenses are going to cost more),annual health check up, religare care scores over. But it has got the limit on room as it offers only single private room which should be the most economical in any treating hospital as per the policy wordings.

Also there is a clause under 3. Special Condition is that “The company’s maximum, total and cumulative liability, for any and all claims incurred during the policy year in respect of all insured persons, shall no exceed the Sum Insured.’

Does it mean that even if my insurance recharged, my total claim amount cannot be more than my SI?

These are the points i get confused with religare than apollo.

Kindly suggest me so that it will help me in finalising my health insurance.

Regards,

Saravanan

Saravanan , first of all i would like to state that yours going for a separate cover (in addition to employer provided) is a wise decision and i really appreciate that.

Now coming to your choice of health policy. See, among your selected options i believe that both have some attractive features, so one has to weigh as per his own requirement. Religare looks better due to majorly 2 features – 1. is the annual health check up feature and other is recharge feature which is much better than restore. You may check the difference in restore and Recharge here http://goodmoneying.com/insurance-planning/what-is-restore-and-recharge-in-health-insurance

In Religare there’s one more additional feature of NCB super which will grant 50% of SA as NCB benefit each unclaimed year upto maximum of 100%, and this is along with the normal NCB benefit of 10% of SA per year upto maximum of 50%

regarding your doubt as per clause 3 (special condition), it is specifically mentioned that special conditions shall be applicable only if the same is mentioned on the policy certificate. So if your policy gets accepted under special condition only then this condition applies.

Now the benefit of apollo is that unlike religare there’s no condition of room type or surgeon’s expenses.

Room rent is the main condition on which your complete hospitalisation cost depends, but i think single private room is the one which patient generally opts for. I think this room rent condition of single private room is there in max bupa policy also.

I would recommend you to visit any nearby big corporate hospital and check for room rates and figure out the one you or your family will opt for in case of emergency and decide your policy accordingly

Thank you very much for your useful reply. I will do the check accordingly and decide.

Regards,

Saravanan

RELIGARE have rejected the proposal of my 14 year old healthy kid on the grounds of the 2-3 years old past medical history of SYNCOPE, although the doctors then had given clean chit after performing ECG, MRI etc.

RELIGARE refused to do a fresh medical examination on him to verify condition of health in case of doubt, stating that state of his current or future health is immaterial.

RELIGARE even refused to arrange for a discussion between me and the underwriter who had rejected his proposal thereby closing all avenues of any discussion. (In all probability, the under-writer has not even understood the old medical reports of my son, sent by me).

Their replies to specific and pointed questions in my emails are vague and round about.

Such a stand by RELIGARE will affect my son’s future since other insurance companies also will tend to go by the precedence of past rejection by RELIGARE and reject his proposals even though he may be enjoying perfect health.

They have only one standard response for everything and they do not answer any specific questions. If this is the state of affairs before policy issual, imagine how they could deal with the insured persons when they put up a claim. You could be up against a wall everytime,

I recommend the readers to be very careful while choosing insurance company for your health insurance and spread such information to your colleagues so that they don’t fall into such a mess with insurance companies like this who do not seem to espouse any value.

Sir, Kindly let me know your opinion about claim settlement of Religare Health Insurance CARE.

I personally have not found any problem with the claim settlement of Religare.

Infact i have not experineced any hassle in cash less claim of any company, but once one get into reimbursement process then one should be ready for the hardships.

Dear Sir,

I want to buy family floater health insurance plan for myself(31), Wife (31), Daughter (1). I have shortlisted Reliance Health Gain & Apollo Munich Optima Restore. I need Good claim service & affordable renewable premium ( no claim based Loading). In the policy wording of Apollo munich optima restore ..In General Condition -Insured person-100-150% risk loading applicable on premium.Since Apollo munich broacher says no claimed based loading.can you explain this clause? I have read that ICICI lomabard is leader in market share of health insurance. can I go with ICICI lomabrd?

Also please review Reliance health gain plan , I think it is mixture of apollo munich optima restore & religare Care.

Which is best plan according to you? & other plans options I should consider (like ICICI, Religare, Max Bupa ..etc).

Sanjeev, the main point is that you should be adequately insured. Whether with apollo, reliance or icici, it doesn’t matter.

What apollo says is that at the time of accepting case in the first place they may put loading on premium amount depending on their risk assessment of that profile, but once case is accepted there would be no claim based loading.

I will surely review Reliance health gain plan soon.

Thanks

Dear Sir

I’m confused between Religare Super NCB, Apollo Munich, Max Bupa ICICI Lombard Family health insurance Plan. I find Religare Super NCB is attractive and affordable for 5L policy for my family of me(50Yrs), Wife(44Yrs) & daughter(14yrs).

I have the symptoms of Diabetic since 2006 on border level with tablets 2 times daily(Under control), wife has BP & Thyroid TSH under medicine daily(quite under control). Whether I shall be rejected by any health insurance co or not !! and if not & accepted then what plan option of which co above cos is best. Kindly advise.

Sushant, first thing first you should be having health insurance, be it from any company.

Every company has its own underwriting guidelines and your case acceptance purely depends on that . As per my experience apollo is very strict in its terms. and it does not accept Diabetic cases. However it has recently launched “Apollo Munich energy” a special health insurance plans for diabetics which can also be considered (http://goodmoneying.com/insurance-planning/apollo-munich-energy-health-insurance-plan-diabetics) , but before that you should try your luck with other insurers, which sometimes accept controlled diabetic and thyroid cases

You just have to understand the exclusions ,waiting period and sublimits of those plans.

BEWARE. Religare is very quick to call you on the phone to take payment. At no stage do they inform you that there is a Rs300 fee for declined policies. Your card is charged immediately, without the policy being issued. After a week they inform you that you policy has been declined and it will take 10 working days to process a refund. Why should the card be charged without a policy being issued? And to add insult to injury, a Rs 300 fee is charged for declining the policy. Horrible service

I have used Max Bupa Heartbeat 2L for 1 year and now i have ported out my policy to Apollo Munich Optima Restore 5K, I am planning to take a new Policy of Religare Care with Super No-Claim Bonus 5L. I will cancel Apollo as i haven’t received documents yet, so i have 15 days time to cancel and go with Religare. I just want to know that am i taking right decision?

Vinay, both the policies i.e. apollo restore and religare are equally good. Though religare super NCB has few different features like higher NCB and annual health check up. See if you want to move out from apollo due to the bad service experience or high premium then its fine otherwise doing same exercise to buy new policy does not make sense to me.

Every year you will find companies launching new products, so one should not keep moving between insurers. Stick to any one you like and continue your policy for some years. there’s no point in moving out unless there is some very attractive feature…atleast attractive to you.

Hi,

I have taken Easy Health Plan for my father age 58 from Apollo Munich.The policy issue date is 12 Sep.2014. My father undergone pre policy health checkup and at that time all medical reports came normal . He has no high B.P, no Diabetic, no Cholesterol,E.C.G is also normal. Also my father did not hide any disease in the proposal form .He is fit & fine no health issues in the past.

But on 24 sep2014 he is suffered chestpain & admitted to hospital, Doctors perform angiography & in the test 1 blokage found & then doctors done angioplasty, now he is stable. My father has employer health insurance so I made claim & claim is approved.

Can I inform my father post policy heath condition to Apollo? if yes then Apollo will increase premium or rejected policy at the time of renewal? My fear is that if I do not inform the Apollo then if there is claim in near future there is chance of Apollo will reject the claim?

Please advise me what should be I do in the above case.

Apollo has no claim based loading & I have not made claim yet so can they then increase premium on the basis of current health history after issuing health policy. Please advise.

Can you explain me following clause in Apollo easy health policy document.

.Loadings & Discounts:

We may apply a risk loading on the premium payable (based upon the

declarations made in the proposal form and the health status of the persons

proposed for insurance). The maximum risk loading applicable for an individual

shall not exceed above 100% per diagnosis / medical condition and an overall

risk loading of over 150% per person. These loadings are applied from

Commencement Date of the Policy including subsequent renewal(s) with Us or

on the receipt of the request of increase in Sum Insured (for the increased Sum

Insured).

We will inform You about the applicable risk loading through a counter offer

letter. You need to revert to Us with consent and additional premium (if any),

within 7 days of the receipt of such counter offer letter. In case, you neither

accept the counter offer nor revert to Us within 7days, We shall cancel Your

application and refund the premium paid within next 7 days.

Please note that We will issue Policy only after getting Your consent and

additional premium (if any).

Also I have received soft copy of the policy but physical documents not received yet due to my home is locked. now Apollo will be sending documents again

As the heart problem arose after the issuance of Apollo Policy so there’s no point of Loading the premium or rejection of policy. You are also under no obligation to inform apollo people about the current health condition, but if you want to you may go ahead. This should not affect your policy in any way.

Just keep all the medical documents like first diagnosis report and test reports and maintain a proper file for this. In case in future you claim from apollo they will ask for these documents to verify that this problem was not preexisting at the time of policy buying.

The policy wording clause is applicable at the time of policy issuance and says that company may put a loading on the premium depending on the underwrting process and health condition of the proposer.

Hi Mr. Singal,

I am looking for a Policy for My Father(age 53) , Mother(age 46) , Wife(29) ,Me(29) and My grandPa (85).

What you can suggest?

Best Regards

Ajo

You may go for a separate policy for your parents, a floater plan for yourself and your spouse and another plan for your grandpa.

For your parents and yourself, there is complete universe of health plans available , but for your grand pa you have to search out. There are policies from Apollo, Star, Max, and from nationalized companies too which offers cover to Senior citizens.

Hi Mr.Singal,

thanks for the reply and I appreciate the way you are responding for everyone’s query, which is fantastic.

What is the meaning of SI and SA?

Why did you suggest separate plan for parents, is it to get more insured sum?

I heard normally companies won’t allow for senior citizens, do you have any particular suggestion for that ?

Hi Ajomon

Thanks for the appreciation.

SI stands for Sum insured and SA is sum assured. Generally Sum insured is something from insured perspective and sum assured is from insurer’s . There’s very thin line between these terms and normally it is being used interchangeably.

You may go through this link to understand the terms better

http://www.livemint.com/Money/Ksp8iZvMDxOm9wdYSXuwnK/Did-you-know–What8217s-the-difference-between-sum-assur.html

The reason for me suggesting separate plans for parents is because of :

1. High probability of illness due to age. and thus they should have their own separate adequate cover .

2. Claim frequency can be high due to which other members of floater policy will have to suffer with reduced no claim bonus.

3. In many floater policies, the premium is calculated from the age of person with higher age group. so this unnecessary increase the the overall premiums.

These days many companies offers policy to senior citizens – Max, religare, apollo, ,star even nationalised companies also have specific plans for senior citizens.

Dear Sir,

I want to buy a family floater policy of Rs.10 Lakh for my family(2 Adult, 35&32 Year and 1 Child, 2year). I have short listed Apollo Munic Optima Restore, CignaTTK Prohealth and Religare Care. Please let me know which one will solve my purpose.

Thanks & Regards,

Pramod

Any of your selected policy will solve your purpose. Go ahead. All the best!!

Hi Manikaran,

I have following queries

I am 28 year old and am confused whether to go for health insurance (single or double) or critical illness plan.

1) Could u give me difference between the above 2?

2) Also I have a brother. So whether we both can take a combined health insurance plan? If yes, which companies offer that?

3) I have shortlisted 3 companies a) Religare Care b) Apollo Restore c) Cigna TTK.

Could u guide me as to which one you be better in terms of cheaper premium, more benefits, more critical illness covers, more bonus for no claim, regular health checkups, more domicilary coverage, no cap on room rent and on diseases and that includes dental cover. Suggest me which one is good for SI of 10 lacs.

Arun, Health Insurance cover and Critical illness plan are totally different from each other. Where a health cover will take care of the hospitalisation expenses even due to critical illness, Critical illness is meant only for some specific illnesses. You can understand more about these from the link below

http://goodmoneying.com/insurance-planning/critical-illness-policy

You cannot take a joint policy with your brother.

The main thing is you should be having adequate health insurance cover. Apollo is older than Religare and Religare is older then Cigna TTK, so definitely experience wise Apollo as a company is better, but in comparison product wise religare product is better than apollo restore. I have no idea on Cigna TTK policy, so you have to work on the comparison front.

Dear Sir,

1.Is it true, that in a family floater health insurance policy, if senior most person expires then whole policy lapse and rest of the member need to take policy again?

2. Can I take 2 floater health insurance policies, one myself as proposer jointly with my wife and another my wife as proposer jointly with me.

Thanks

Vasu

1. It used to be the case earlier. I am not sure about the national companies’ policies, but in private policies the second senior member can take over the policy and policy will remain continued.

2. Yes. But why?

Dear Sir

I’m confused between Religare care, Apollo Munich, Max Bupa ICICI Lombard Family health insurance Plan. I find Religare care is attractive and affordable for 5 L policy for my family of me(58Yrs), Wife(54Yrs) .

I have the symptoms of arthritis and hip replacement may be needed in future i am taking sazo 2 tablets per day.

plz suggest which plan is good for me.

Hello Mr. Singal,

I wanna buy insurance policy for my Mother(Age-59). She is Diabetic and I am not aware of any other health insurance policy and its details except Religare as Religare customer service has been calling me these days many times. I liked some features of religare like auto recharge,no co-payment and free annual health checkup.

i just want to confirm the reliability of Religare and its claiming & reimbursement process. will it be safe to go with religare ?

As i read some negative comments too about religare above.

In this internet age its very easy to defame anyone. If people like something they may not give positive comments, but if they don’t like then will surely give negative comments. In my personal view Religare is like any other health or general insurance company. You should look at the product features and if it suits you then go ahead with it.There’s nothing to worry.

But make yourself comfortable first. Otherwise go with the one which you are comfortable with. Check out Nationalised insurers.They must be having good name in Janta.

Dear Sir

I an interested to Buy a Healt insurance policy

for my Father & mother from Max Bupa Heart Beat Plan ( 2 Lakhs )

Age is 55 & 50 Years

Till now there is no critical health issue.

this plan is better or not

Please suggest m,e & guide me.

Max bupa heart beat is a good plan. Pls do understand the condition of co payment after crossing 60 years of age, and other conditions attached

Dear Sir,

My company is providing 3L coverage to my family ( me, spouse and 2 children). I am planning to take 5L health insurance policy. I have gone through current policies and not able to take decision. I have gone through Appollo Munich, Religare, Star, Max Bupa. Please suggest and guide me which one is better for my case. My age is 37 and both kids are 8 years old.

Waiting for your comments

Ganesh, this is because you don’t find any difference in the features of these products. So now the best way to select among these is write down the slips and tell your children to pick any one.

To me all these policies are good.

Thanks for your quick reply. I hope ICICI Lombard also have same features compare to earlier list. I will take any one of these products. Let me know if ICICI Lombard is not that much good compared to above mentioned products.

One doubt here is, compare to all other product Religare is offering less premium. If all products have similar features then Religare is better option in premium perspective.

Hi,

I am little confused on Religare care and Assure.

Currently I am holding care so do i need to take assure as well for critical illness. If heart related surgeries are not included in religare care then what the use of it. Need some light on it. why two are different product on website. Customer care guys says it includes heart surgeries and all.

Religare care includes Heart Surgeries. Infact all hospitalizations of more than 24 hours are covered, unless it comes under exclusion or pre existing upto specific years. Critical illness policies come into scene, when one is diagnosed with specific illness with specific severity and survives that llness for atleast 30 days. Read out this article to understand CI policies better http://goodmoneying.com/insurance-planning/critical-illness-policy

hi,

Mr. Singal, I need some help to you I have policy for my mother MAX BUAP HEART BEAT 2LAC since last 5 year with pre-exist asthma declared my mother age today around 58,i looking for sum-assured 5lac for her.may in future my mother need some treatment(don’t have any sing. yet) as age grow.. what you suggest,I totally confused between religare care,max bupa hertbeat gold or heart beat companion or any other if you suggest.

I already take super top up of 20 lac for my mother.

Sir

I would like to buy individual health insurance policy of 5L each for my minor children, in which I would be the proposer. My son is now 15 yrs and daughter 10 years old, also my age is 43 years.

I am confused between Religare Care and ICICI Health Advantage Plus Plans in terms of any cap on doctor fees/hospital room/OT charges etc, cashless facility and claim settlement ratio. Pl suggest at the earliest and oblige

Thanks

On ICICI Site, i could not find much details about health advantage, but as far as religare is concerned, for SA of Rs 5 L and above it doesn’t have any cap on doctors fee, OT Charges. Yes it has one limit on Type of room- which should be single and the most basic in its category. cashless facility is available with almost all the policies these days in network hospitals. There’s no ready data available on claim settlement ratio in health insurance policies, but referring to the claims made by company people, both religare and icici are good.

You pl go through the policy wording of ICICI policy too, before making the final call.

I am 42 yrs old and looking for health insurance for my family ( 2+ 3) under family floater plan. My employer is giving us insurance but still i would like to go for it. After all my researches with Star, apollo, max and religare, i have finalised two of them.

Max bupa health companion and Religare care for 5L SI.

Now i am little confused in finalising between these two. My first priority is settlement of claim if any and efficient customer service. I am based in Delhi

Pls help me to resolve this and finalizing one between Max and Religare.

I am looking to buy policy within this week hence your prompt reply will help me a lot.

As far as my experience goes, both religare and max has good customer service. You cannot bet on other people’s experience, as situation may differ. These days there’s very hard competition and due to porting out feature available, health insurance companies are giving very prompt service to retain the customer. So in my view you can go with any one of these.

Thanks for your response. Since you are handling such cases regularly and having in depth knowledge, Can you suggest me which one is better?

Also which company is having higher claim ratio?

One more point, Is TPA is better then direct claim? Pls advise

I am health insurance policy holder with maxbupa for last 3 years, if i port my policy from maxbupa to some other

insurer eg. religare health this year(2014) i will get continuity benefit of 3 years, and again if i port my policy to some

other insurer eg. hdfc health next year(2015) will i get continuity benefit of 1 year of religare or 4 year(3 years of maxbupa & 1 year of religare).

I am health insurance policy holder with maxbupa for last 3 years, if i port my policy from maxbupa to some other insurer eg. religare health this year(2014) i will get continuity benefit of 3 years, and again if i port my policy to some other insurer eg. hdfc health next year(2015) will i get continuity benefit of 1 year of religare or 4 year(3 years of maxbupa & 1 year of religare).

Hi Manikaran,

I’ve Apollo Munich Optima Restore from last 2 years; SA = 3L. Now for this year’s renewal they’ve given me an option to increase my SA to 5L. I would like to know if there’ll be any waiting period/other limitations for this increased SA, as I couldn’t find it anywhere mentioned.

I’m thinking of going for this increased SA option, but it seems Apollo has higher premiums compared to other players for the same SA and almost similar features. Also, premium increases hugely especially after 45 yrs. According to you are there any good reasons to justify this huge gap in the premiums?

Thanks,

Vaibhav

Vaibhav, the “plus offer” that comes with renewal notice of apollo says that you can increase your sum assured with no medicals tests required. All the conditions of waiting period and others stays as it is.

Apollo do have higher premiums. If you want to increase your insurance coverage, you may try any of these 4 ways http://goodmoneying.com/insurance-planning/4-ways-enhance-health-insurance-cover.

Manikaran sir,

Your suggestions are two good.

I took a Religare Care policy on Jan 2nd 2016. But I want to cancel this policy and later on I want to take a Star health optima plan. I think star health optima is better than Religare Care. Am I right sir, is it a right decision. What’s your suggestions may I continue with Religare or join Star health.

If you think, then you must have read something about star optima. Point is you should be adequately insured, with the plan you are more comfortable with.

Hello Manikaran,

I wanted to know the claim settlement ratio of Religare to proceed further. As far as comparison is concerned i found Religare Care a suitable plan for my family for Rs 5 Lac policy with super top-up of 10 lacs from L&T Health insurance. What is your suggestion, please share?

Abhinav, claim settlement ratios of health insurance companies are not readily available. So you need to decide only on the product features, comfort with the brand and knowledge and service quality of agent.

I’ve Health insurance coverage from my employer with “United India Insurance Co. Ltd.” and we’ve Portability option even if we leave

the company. That meas we can continue with the this insurer even after resigning and below are the features will be covered.

1) With stadard benifits

2) Pre-existing conditions will not be applicable as I’ve completed the pre-existing period (3 or 4years) with my current employer

Is it suggestible to continue with the same or shall I take one more out of employer? I was trying to contact on “United India

Insurance Co. Ltd.” customer care number but could not connet (either number does not work or waiting or not picked up).

Please suggest.

On the face of it, i don’t think you should go with any other separate policy. Its just you should look at the sum assured which should be more than enough for you and if it’s not then you may buy a super top up plan to add on to your total coverage. Also have a look at the policy conditions. Normally national insurers have lot of conditions attached in their policies. They also have some list of network hospitals where they will pay as per terms else with some co payment.

See you need to be convinced on the features, sum insured and the service quality of your insurer.

Hello Sir, I really appreciate your efforts to reply almost every individual Query. I would like to ask that I have taken PNB Royal Sundaram policy of 3 Lakh SA for my parents if I want to increase SA to 7- 10 lakh in that case will it be beneficial to opt for super top-up policy from L&T?

Will PNB Rolay Sunderam policy be beneficial is there any other drawback other than following:

1. Caping on Room rent to 1% of SA

2. Caping on ICU to 2% of SA

3. Caping on Domiciliary treatment to 10% of SA

Please suggest will it be benefial as the premium in this policy do not increase on increase in age.

Himanshu, You may increase the cover through Super top up policy. But do understand that if you have 2 policies from different insurers, then in case of high claim you may have to make a Reimbursement claim from the second insurer. I mean total claim may not go cashless.

There are other ways of enhancing the health insurance cover too http://www.goodmoneying.com/insurance-planning/4-ways-enhance-health-insurance-cover

and yes, what you have written about PNB policy are just features and not drawback, as long as you know/understand it

Sir,

I want but an individual policy for the first time for my mother (age :46 yrs),SI 5LAC,shall I go with private insurance company or nationalised insurance company ? I need your precious suggestion !

Can I go with National insurance Co? what about its cashless claim payment ?? Plz ans ?

You can go with any insurer as per your suitability. National insurance is also fine. Cash less payment should not be a problem if treatment was taken as per their terms and conditions. I recommend you yo meet some agent or visit their local office and read out the terms and conditions first. Public insurance companies work with in specific defined network of hospitals…so you should know how this arrangement works.

Hi,

I’m looking for a life-long health insurance policy for my parents:

Dad age:will be 70 next month

Mom age: will be 67 in August

I got to know about 10 best health insurance plans in India,out of which I shortlisted Star, Religare, ICICI Lombard and Max Bupa.

But I have also read very bad reviews on all of these,but I need to take one urgently.

My dad has slight diabetes and mom has slightly higher pressure,otherwise in general they are of good health.

Can someone guide me.

Thanks and regards,

Lakshmi

I WANT TO BUY A NEW POLICY FOR ME AND I AM SO CONFUSE BETWEEN TWO COMPANIES SO PLEASE SUGGEST ME WHICH I BUY STAR HEALTH OR RELIGARE.

I have got a oriental health insurance family floater gold plan of SI 9 Lacs, in the 3rd year , should I continue it or shift to religare family floater.

Hi Mani,

you are doing really great job. i greatly appreciated your valuable time and response to every user’s query.

great job done by you.

i am planning to buy health insurance plan for me (29 yrs) and my wife(28 yrs).

i am also planning to buy separate health insurance plan for my parents, father(55 yrs) and mother (53 yrs).

i came to know many plans through R & D in google by self. but i am confused which one should i select ?

can you please guide me which plan is suitable for us.

every one is fit and fine except me, 6 month back i was suffered from High blood pressure. now it is under control due to medicine. will it effect on health insurance plan ? will company consider this one as pre existing disease ?

will maternity cover by health insurance ?

can we buy health insurance policy online ? is this trusted or not ? or should we go through agent ?

Thanks & Regards

Sanjaysinh

Hi Sanjay

Thanks for your appreciation.

See, nowadays i do not find much of difference in most of the health insurance policies, except for their underwriting conditions.

Since you said that you have High BP and that too at such a young age, so some companies might put this into exclusion. If not, high BP and related illness will surely be a preexisting condition, and will not be covered for first few years.

All of you in the family are below 60 years of age so for you all policies are available. Just go with a policy with no sublimits.

Maternity cover are there in some of the policies upto a specific limit and covered after some years of continuing with the policy. Like max Bupa and apollo has maternity cover, Religare has specific maternity related policy.

You can buy health policy online, however, it may not result in saving on premium cost.

I have health insurance with max bupa under health companion family floater. I am using this policy for last 3 yrs. We got claim for year 2015-16 and 2016-17 for my husband (both times). policy included 3 members till my husband’s death last yr. Now we are 2 members. Myself 45+ and my son 10+,

Though there was no problem in taking claim but i found its premium is on higher side n increase every yr.

I am satisfied with service and claim settlement but would like to know is there any other policy which gives same benefits/felicities in less premium?

Now its time for renewal and I have not claimed for 2016-18, Shall I go for portability or continue with same policy?

My view you should continue with the same policy. Max Bupa health companion’s premium and benefits are very much comparable to others and its a good policy