Estimated reading time: 10 minutes

There are 3 kinds of Investors. One who are risk-takers and understand that there is nothing called guarantee in Investments, and thus to gain good returns you have to take the risk. The second type of investors needs a guarantee- as safety and certainty are the prime requirements, even at low returns.

Then there are third ones, who desire to have high returns and that too with Guarantee. These are the confused lot, who are the Gullible ones and thus easy enough to catch attention by showing them the Guarantee.

Mutual funds are not allowed to use the word “Guarantee” in their schemes and are mandated to disclose all the known and possible risks in the Information documents. But Still, Investors are pitched and are attracted towards Past returns and feel this is something the fund will keep giving.

Insurance companies can freely announce guaranteed products and market them as well. However, they will also mention some risks in the Policy document, But the Power of Guarantee always overpower the Risks.

Bajaj Allianz has also launched one such Guaranteed Pension product, with the name Guaranteed Pension Goal. These days you will find full-page advertisements of this product in many leading newspapers and so the queries have been pouring in, to Review this product. So here it is.

Read: Retirement Plan or Pension Plan – what to chose?

Bajaj Allianz Life Guaranteed Pension Goal- In Brief:

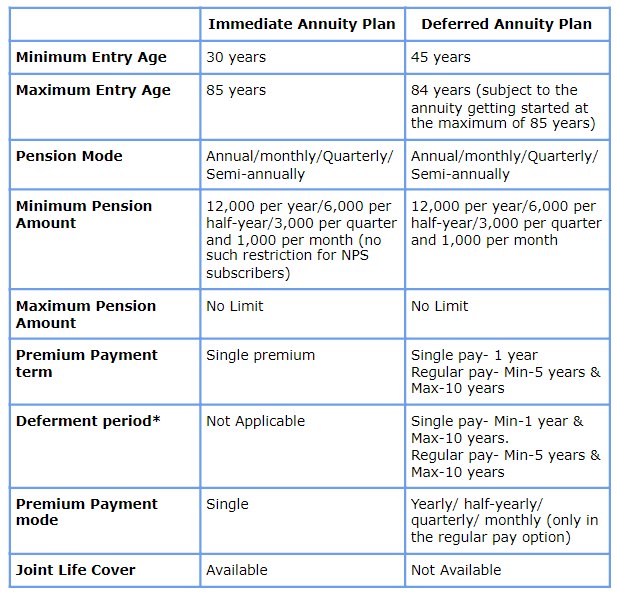

Bajaj Allianz Life Guaranteed Pension Goal is a Non-Participating, Non-Linked Annuity or Pension Plan. It offers both Immediate and Deferred Annuity options.

In the immediate annuity option, you will have to invest a lump sum amount in this pension plan and the regular pension payout would start from the next month/year/quarter/half-year as opted by you.

In the deferred annuity option, you may either invest a lump sum (single premium) or pay regular premiums for a number of years (1-10 years), which is called a deferment period. The pension payout would start after the deferment period chosen by you.

It has various annuity options to choose from wherein you may opt for a pension for the years you are alive, pension with the return of purchase price after a fixed number of years (as specified), or on death. A joint-life option is also available with a 50% or 100% annuity payable to your spouse after your death. These options are discussed in detail later in the article.

Bajaj Allianz New Pension Plan- Key Features:

Here are some of the key features of Guaranteed Pension Goal- Pension plan from Bajaj Allianz:

How does this plan Work?

In this pension plan, first, you need to decide whether you wish to receive Immediate Annuity or Deferred Annuity. Then, you are to choose from the Annuity options available under both Immediate and Deferred Annuity Plans. The option once chosen cannot be changed during the policy term.

Decide the purchase amount and payout frequency you wish to receive from the plan and receive the pension amount as desired.

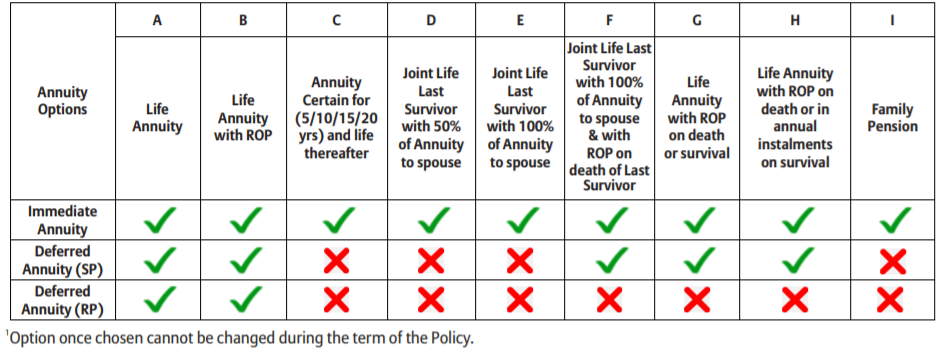

Guaranteed Pension Goal- Annuity options available:

Following are the Annuity options available under the Bajaj Allianz Guaranteed Pension Goal- Pension plan:

Annuity options under the Immediate Annuity Plan:

Let us look at the Annuity options available under the Immediate Annuity Plan. In these options, Annuity will be payable to you on each Annuity installment date according to the frequency opted by you at the inception of the policy.

- Life Annuity (option A): Same amount of annuity/pension would be payable to you (the policyholder) till you are alive.

- Life Annuity with ROP on death (Option B): Annuity will be payable to you till you are alive and on death, the Purchase price (invested amount) will be returned to your nominee. It is just like Bank FD with interest payout.

- Annuity certain and life thereafter (Option C): If you remain alive or not, you would be paid the pension amount for a fixed period of 5/10/15/20 years, as chosen by you while taking the policy and thereafter till you are alive.

- Joint Life Last Survivor with 50% of Annuity to spouse (Option D): Annuity will be payable to you till you are alive and on your death, your spouse will receive 50% of the initial Annuity amount throughout his/her life. For instance, if you are getting a pension of Rs. 10,000, after your death, your spouse would receive 5,000 as pension till he/she is alive.

- Joint Life Last Survivor with 100% of Annuity to spouse (Option E): Annuity will be payable to you till you are alive and on your death, your spouse will receive the same amount as pension throughout his/her life. For instance, if you are getting a pension of Rs. 10,000, after your death, your spouse would also receive 10,000 as pension till he/she is alive.

- Joint Life Last Survivor with 100% of Annuity to spouse with ROP on death (Option F): Annuity will be payable to you till you are alive and on your death, your spouse will receive the same amount as pension throughout his/her life. Also, the purchase price (invested amount) would also be returned to the nominee on the spouse’s death.

- Life Annuity with ROP on death or survival (Option G): Annuity payment would be continued till you are alive also if you survive more than 25 years after taking the policy or reach 85 years (whichever is later), the purchase price would also be refunded. If the death happens before then also the invested amount would be paid to the nominee. For instance, if you took the policy at 55 years of age, the annuity would continue till you are alive, let’s say 90 years, on completing 85 years, the invested amount would be paid. Now, if you die before 85, then also the invested amount would be returned to the nominee.

- Life Annuity with ROP on death or in installments on survival (Option H): Annuity payment would be continued till you are alive. If you survive more than 15 years after taking the policy or reach 70 years (whichever is later), the purchase price would also be repaid in installments as per the Annuity payment frequency chosen. In yearly payment frequency, the survival benefit will be in annual installments equivalent to 5% of the Purchase Price. Under monthly, quarterly and half-yearly, each installment, respectively, will be (5%/12), (5%/4) and (5%/2) of the Purchase price. Survival benefit will be payable till the total of all the installments equals 100% of the Purchase Price. On death, an amount equal to Purchase Price less sum of the Survival benefit paid (if any) shall be paid to your nominee.

- Option I (Only for NPS subscribers): If the NPS subscriber has a spouse/spouse who is alive, Annuity will be payable as per Option F above and if the spouse is not alive Option B would be applicable. On the death of both the policyholder and spouse, the purchase price of this plan shall be used to purchase an Annuity under Option B, on the dependent mother/father whoever is alive.

(Also Read: All You Wanted to know about the New Pension Scheme)

Annuity options under the Deferred Annuity Plan:

Under the deferred annuity plan, the following options as mentioned above are available, the only difference is that the annuity payment would start after the completion of the deferment period as opted by you at the time of taking the policy.

- Option A- Both Single and Regular premium payment terms are available.

- Option B- Both Single and Regular premium payment terms are available.

- Option F- Only a Single Premium payment term is available.

- Option G- Only a Single Premium payment term is available.

- Option H- Only a Single Premium payment term is available.

In case of death during the deferment period, the purchase price plus attached Guaranteed Additions, subject to a minimum of 105% of Total Premiums paid, shall be paid to your nominee.

On death after the deferment period, nothing shall be payable in option A, In all other options, an amount equal to the Purchase price plus attached Guaranteed Additions after deducting the annuity installments already paid shall be paid to your nominee, subject to a minimum amount equivalent to the Purchase price.

However, in option G nothing shall be payable if death happens after receiving survival benefit and in option H where survival benefit is also paid in installments, survival benefit already paid would also be deducted from the purchase price along with the annuity installments.

Here, Guaranteed Additions mean one annuity installment shall be added at the end of every month, during the deferment period depending upon the annuity frequency chosen. The amount would be either:

- Yearly Annuity installment/12

- Half-yearly Annuity instalment/6

- Quarterly Annuity instalment/3

- Monthly Annuity installment

Guaranteed additions would not be payable if the policy is lapsed (i.e. you stopped paying premium in between).

The table below summarizes the Annuity options available under the Guaranteed Pension Goal- Pension plan:

Guaranteed Pension Goal- Annuity Rates and IRR calculation:

Here’s the sample illustration provided on the sales brochure on the company:

In the case of an immediate annuity plan, the rate of the annuity (annuity amount/purchase price)*100 comes in the range of 6.7%-7.7% (pre-tax).

Now, if we calculate the IRR assuming that the life expectancy of the person investing in this pension plan would be 85 years, it reduces to below 6%, pre-tax (even in the ROP option). Obviously, the rate of return would increase if you live longer than 85 years.

In Deferred annuity, the annuity rate looks attractive in the range of 12%-15% but the catch is in the deferment period. What about the interest during this period?

The IRR of the deferred annuity plan also comes at par to the immediate annuity plan only i.e. below 6% p.a. (pre-tax) assuming the life expectancy of the annuitant is 85.

As you may see, a guarantee of returns comes with its own costs. The opportunity cost of your investment is getting lost in the fall of the guarantee.

Should You Invest in this Guaranteed Pension Goal- Pension Plan?

Annuity plans are suitable for generating regular income, particularly in the post-retirement phase. The main advantage of these pension plans is that they offer a fixed rate of Interest for a lifetime, which will ensure the continuity of a specific cash flow after Retirement.

Also, it is mandatory for NPS subscribers to purchase an immediate annuity product where you invest 40% of the retirement withdrawal for a lifetime pension. (Read more on the NPS withdrawal rules here)

Bajaj Allianz Guaranteed Pension Goal- pension plan is also a “me too” kind of pension plan offering similar kinds of features as other products in the market. Nothing unique is offered.

Annuity Rates too are comparable to the other pension products. Like- if we compare it with HDFC life Immediate annuity plan or Pension guaranteed plan, LIC Jeevan Akshay VII which was launched a few months back, which I have reviewed earlier.

(Read a detailed review of LIC JEEVAN AKSHAY VII here)

In the deferred annuity plan too, the rates look high on the face of it but the zero interest in the deferment period makes it at par with the immediate annuity plan. It is also somewhat comparable to the Sanchay Plus plan, which is also a popular annuity product from HDFC.

(Read a detailed review of HDFC life Sanchay Plus here)

Although the rates don’t look that bad (may vary in future) especially in today’s kind of low-interest rates scenario. Plus safety of corpus and guaranteed income would be a larger concern while planning for post-retirement income generation, but going forward when the interest rates will rise, even then once invested your return would be fixed at these numbers.

The immediate annuity option may fit in the regular income generating bucket along with other products like:

- Senior Citizens Savings Scheme

- Pradhan Mantri Vyay Vandana Yojana

- Fixed Deposits

- RBI saving Bonds

- Post office Monthly Income Scheme

- SWP from debt/balanced mutual funds (though relatively risky)

which would help manage inflation and taxation in a better way. Read More about the Bucketing Strategy here.

But it is also a fact that interest rates would not remain lower for longer in a developing country like India. So, it is wise to add some open-ended products for now and may like to add such lifelong lock-in pension products in a better interest rate scenario.

This Review on Bajaj Allianz Guaranteed Pension Goal Plan is Done by Mr. Varun baid, CFP Professional

{kind=link}