These days health insurance policies have come up with feature name like Restore of sum assured or Recharge of sum assured, there are some policies with a feature of Replenishment of sum assured also. With the somewhat similar names, it leads to confusion in the mind of buyer who starts believing that these might be one and the same thing, which actually is not. It varies considerably in the actual benefits. This article aims to understand in detail the restore or recharge feature with a specific reference to Apollo Munich optima Restore and Religare health Insurance Care.

Both Restore and Recharge means reinstatement of the complete sum assured in the policy year, but with different conditions.

What is Recharge of Sum assured?

The Recharge feature is available with Religare health insurance. Taken from Policy wordings of Religare Care, the explanation of Recharge of Sum assured is as Under:

Recharge is the Reinstatement of the Sum assured. If the claim is payable in the policy, then the company agrees to automatically make the reinstatement of upto the sum assured for that policy year only provided:

1) Recharge will be utilised only after the sum assured and No claim bonus has been totally exhausted in that policy year.

2) The Recharge shall be available only for all future claims and not in relation to any illness or injury for which a claim has already been admitted for that insured person during that Policy Year

3) The total amount of Recharge shall not exceed the sum assured for that policy year

4) The Recharge amount will not be available in case there is only a single claim in the policy year.

5) The balance of recharge amount shall be available during the policy year till it is exhausted completely.

6) Any Unutilised recharge cannot be carried forward to any subsequent Policy Year.

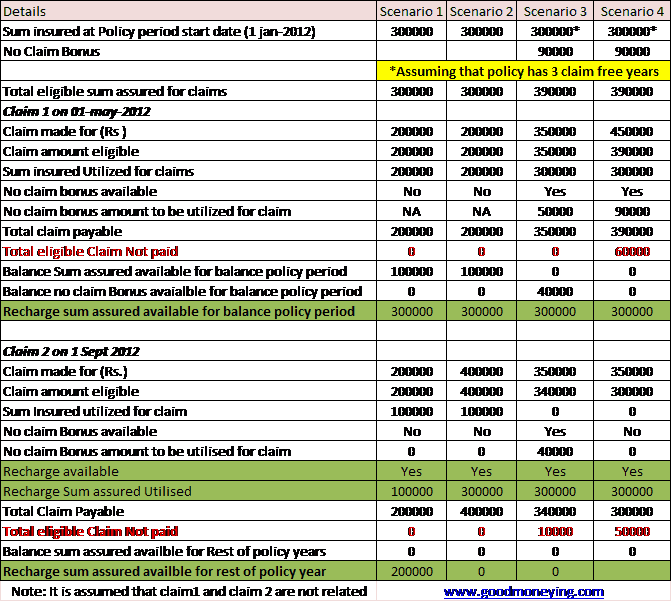

To understand the Recharge of sum assured in detail, below is the exhibit taken from the policy wordings of Religare with some modifications.

Now what the above exhibit shows is that Recharge was not available for the first claim, and as per the policy wording also recharge amount cannot be claimed for the first/single claim in policy. But for second claim where the sum assured was not proving sufficient, recharge gets activated and supported the claim payment. There’s only one condition, which is that the claim where recharge will be utilised should not be related to any of the previous claim in that policy year. This means that if in all the scenarios above the Claim 2 was related to claim 1 then No Recharge of sum assured benefit would have been available. Read More: Health insurance Case study

What is Restore of Sum assured?

Restore is again the reinstatement of the sum assured in a policy but with different conditions. The Restore feature is with Apollo Munich Optima Restore plan. Policy wordings of Apollo Munich Optima restore explains restore as :

If the Basic Sum Insured and multiplier benefit (if any) is exhausted due to claims made and paid during the Policy Year or made during the Policy Year and accepted as payable, then it is agreed that a Restore Sum Insured (equal to 100% of the Basic Sum Insured) will be automatically available for the particular policy year, provided that:

a) The Restore Sum Insured will be enforceable only after the Basic Sum Insured inclusive of the Multiplier Bonus ,have been completely exhausted in that year; and

b) The Restore Sum Insured can be used for only future claims made by the Insured Person and not against any claim for an illness/disease (including its complications) for which a claim has been paid in the current policy year;

c) The Restore Sum Insured will only be applied once for the Insured Person during a Policy Year;

d) If the Restore Sum Insured is not utilised in a Policy Year, it shall not be carried forward to any subsequent Policy Year.

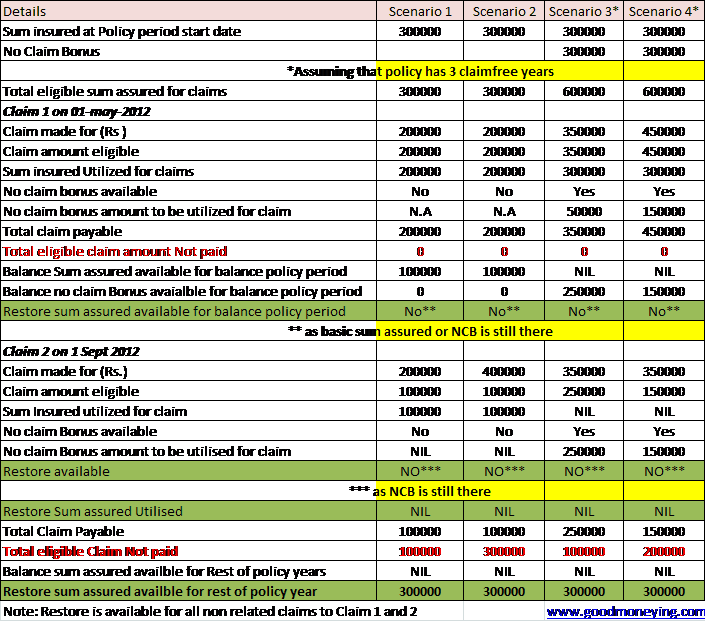

Lets try to understand the Restore feature through exhibit below (with the same scenarios as was in exhibit above):

The above exhibit clearly shows that Restore benefit will get activated only when the basic sum assured plus accumulated bonus will become ZERO. As in the above example in the case of second claim the sum assured was still there in the policy in all scenarios, so the restore benefit does not get activated.

Which one is better – Restore or Recharge?

First thing first, your decision to buy any health insurance policy should not be based on this feature only. You have to understand the various waiting periods, sublimits, exclusions if any in a health insurance policy before taking the decision to buy any.(Read: How much health insurance cover should you buy)

Now as far as among recharge and restore, on the face of it recharge looks much better option. But the major drawback in both the options is that these are for unrelated claims. If you are getting treated of some heart ailment and exhausts your complete sum assured in a policy year, you cannot claim out of Recharge or Restore unless the claim is for some problem not related to heart. Second drawback, specially in restore is that it gets activated only when the sum assured and no claim bonus is completely exhausted .

So in my view, one should look at the basic sum assured and take it to the maximum of affordability. These restore and recharge option will be added benefit which may or may not be used as they have certain condition attached to it.

{kind=link}

Hi Manikaran

Nice Job. I would like to know is it better to buy a top up or a super top up plan to enhance health insurance sum assured or one should buy policies like religare or the alike as you have mentioned which has this inbuilt feature of automatic increase in cover.

I must tell you that this health insurnace space is getting complicated with additional features. Please guide.

I don’t see any difference between the 2 policy terms.

Both recharge and restore are available only after basic sum assured and no claim bonus are exhausted.

The 1st point of both policy terms is exactly the same.

How are you saying the condition is only for Apollo?

Restore can be claimed only after finishing up of your basic sum assured, where as Recharge can be claimed even if the claim amount is exceeding the basic sum assured ( in case of second claim, in policy year)

Sir,

I am 62 yr old, had undergone with two surgeries of large intestine.in 2012.Total expense was 3rd.12 lacs.I was admitted in local hospital where surgery was done,since I went into coma,was transferred to foetus.My policy was of 2 lacs.Star paid rs.2lacs.Then in d year 2015 ,Star stopped S.A.2 lacs.So I paid premium of for 3 lacs.for 2015 / 2016.During 2012 in d second operation I had stoma.( d diagnosis for cancer , which was not ) So on March 2016 I plan for operation of stoma closer of large intestine and joining of intestine to rectum.operation went on for 6 hrs.due to that Dr.was forced to do illestomy I.e.small intestine stoma and on May 20 th, it was decided to close.accordingly I went for cashless ,initially star approved rs.10000 and on d admission 3rd.50,000.00. But on d operation day it was withdrwan.The reason was given that for same ailment restoration is not eligible.My Dr.Lakdawala from Saifee gave me a letter which was forwarded to star cashless dept.But their Dr.denied.

Pls let me know.

C.M.Kulkarni

9322004599