Health Insurance for parents is equally important as it is to you. It carries more weightage due to the high probability of falling ill in that age. For finances sake, it is wise to transfer the risk of medical expenses to insurance company, due to the reasons like

- Increasing Medical expenses

- Low surplus left after saving for other important goals, thus not much for unforeseen medical expenses

- Increasing Life expectancy and deteriorating health

A person’s medical needs increase with age. With health related expenses increasing exponentially, any treatment could easily wipe out your parent’s savings kitty. Even if your parents are financially independent it is advisable to buy them a health insurance plan, which ensures that medical expenses should not impact their savings kitty much. It ensures that your parent’s health care is secured and they can enjoy their savings too. Don’t wait for any emergency as it may cost you huge

Though most of you are actually sensitized towards buying health insurance plans for parents but even then you find it difficult to buy any mediclaim with the reason of not finding a Suitable or BEST policy.

Many of corporate employees feel that they have added the name of their parents in the employer-provided coverage so there’s no need to buy a separate Health Insurance policy for Parents. But this is not wise to depend on the employer’s policy only. Reasons are same as for them not to depend on employer policy (Read: Ensure you are ensured).

This post is all about the various health insurance policies available in the market which you can buy for your parents. With coming up of standalone insurers, this health insurance segment is flooded with many innovative products. Which are quite similar with each other but some features may or may not suit your requirements.

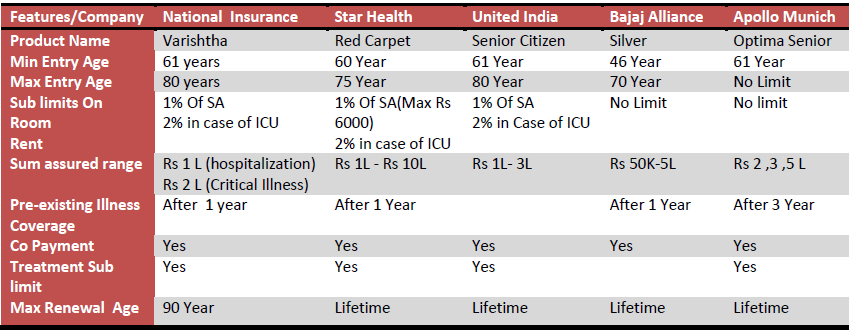

Health insurance for Parents / Senior citizens – Some products.

If your parents have crossed 60 years of age then the options are bit limited with some restrictive features. However these days there are many heath insurance companies where there is no restrictio on the entry age, so anyone can buy anytime. Following companies has got special plans for Senior citizens

1. Star Health Insurance – Star Senior citizen Red carpet plan.

2. Bajaj Allianz General Insurance – SILVER Plan

3. Apollo Munich Health Insurance – Optima Senior

4. National Insurance – Varishtha health Insurance.

5. United India Insurance – Senior citizen plan

Health Insurance for parents – Comparison

(Updated on 14.03.2017)

Check out detailed review of Bajaj Allianz Silver Policy here

As you can see that with the various options available for health Insurance policy for parents, you are bound to get confused. Below I have shared few pointers which will help you in selecting the suitable one.

1. Always go with the policy with Maximum Renewal age. Though this is no longer applicable as all policies now days come with Lifetime renewal limit.

2. Work on your expenditure and buy the maximum possible coverage. Believe me; you just have to reduce your expenses by Rs 1500-2000 per month.(Read: How much health Insurance cover is enough)

3. Check out for the First Year, Second year, special and permanent exclusions if any in the plan.

4. If there’s any Pre-existing Illness, and you are more worried on that front then you should go with the plan with the least waiting period on Pre-existing illness, like select between Star/National/United.

5. If Parents are fit and fine, with no pre-existing illness then select Policy with least compromises like as on room rent.This is because the total hospitalization expenses depends on the room rent only.(Read : Managing Hospitalisation cost)

6. If Parents are diabetic then one should go with nationalised insurances like National/United, to get easy coverage. As they cover these cases with some extra premium/loading.

7. If the company doesn’t want to get the Pre-Insurance medical check up done, then make sure you read the declaration of medical condition form in detail before signing it.

Health insurance for Parents – Some other options

The options are limited in case your parents have crossed 60 years of age. But if you are acting proactively then it is wise to get them entry in this health insurance space before 60 years to take full benefit of health insurance plans that too without any co-payment, sub limits and with lifetime renewal.

There are plans with almost every health insurer now, like Religare health insurance, Apollo Munich Health insurance and Star health (Comprehensive).where if one takes entry before 60 years i.e even at 59 years , he/she can enjoy all the benefits even after crossing 60 years with continuos renewal.(Read : comparison and Review). Even though these plans doesn’t have any entry age restrictions but still it has co-payment clause if anyone takes entry after 61 years of age, so make sure you go through the policy wordings in detail.

You have other options from health insurance policies offered by nationalized banks to its account holders. There are some fantastic policies like as provided by Canara bank in tie-up with Apollo Munich health insurance; PNB Oriental Royal mediclaim policy and even the one offered by Bank of India with national Health Insurance.

Conclusion

If you are still waiting for a good a policy for health insurance for parents then this is the time to act. Your wait may cost you with some limits on the coverage. To get a comprehensive coverage get your parents Insured them right now. There are many health insurance plans which gives the continued, comprehensive coverage for lifetime if taken at appropriate stage and at right age.

Health insurance for parents is a wide topic and many times results into lot many confusion. New products keep coming which increases the confusion. So let me answer your queries in the comments section below. I believe more discussion may be of great help to you and me too with learning from your experiences.

{kind=link}

Very good analysis. It will surely help me in buying a suitable policy for my parents.

Thanks

Thanks Shipra.

Do share your selection with us too.

A very good service done to people taking a right & good decision of protecting the health of their parents and that too in a very straight, transparent & easy manner!

Thanks

Sir,

Seems like you forgot to mention Religare Health insurance – CARE.

Religare doesn’t have any specific policy for senior citizens. However as it allows entry at any age so can be looked into . So i have mentioned this in ” Some other options”.

Good article.

I am surprised you forgot Max Bupa, which is the BEST according to me.

they are open with their clauses which is what I like

Good, It will surely help me in buying a suitable policy for my parents. BUT Doesn’t have any specific Or better policy for my parents which shows min entry Age 50.

Hi Manikaran,

Could you please suggest health insurance plan for my aunt aged 59 years who is completely fit and fine. Just precautionary want to take it. Please guide.

Regards,

Nilesh

Nilesh, at the age of 59 you have the complete universe of policies available with you for selection . Go through stand alone health insurers plan like apollo , max , Religare and select what suits you.

Hello Manikaran,

My Mom is 62 years old and has diabetes. Last week only it has been discovered that she needs an open heart surgery. Is there any health insurance policy which can cover her surgery immediately?

Does the insurance company tests the heart conditions before giving policies?

Thanks!

No Raja. There is no policy which can help you at this stage.

Yes, companies do thorough medical check up before issuing the policy and even if they don’t do the tests for heart conditions it becomes duty of the insured to declare the pre existing diseases. Concealment of ailments will lead to rejection of claim.

But if you have a group policy through your employer, you may check the terms of including your mother in that.

could u pls suggest health insurance plan for my mother whose DOB is 1/1/1954.She has BP.pls guide.

Meghna, your mother is 58 years old and thus she has the whole universe of health insurance available with her. BP is not such issue. Some companies may put some loading for this but this will not restrict them to give your mother health cover. I encourage you to go through the brochures of various companies, so you can get a basic idea of what a health cover can provide you with and then zero down to a specific selection . Start with stand alone health insurers like apollo munich, max bupa, religare and star.

Dear Meghana ji,

If your mother is already suffering from BP, then opt for a policy which has following features.

1. Every year Annual checkup.

2. PED is covered as early as possible ( say 2 or 3 years)

3. That company must have a top up policy, which you must buy along with the basic policy.

My recommendation is Icici Lombard CHI in this particular case.

Hi,

Its very detailed post and lot of good information is posted here.

If you allow, can I recommend other senior citizen policies available here.?

Sumit, this is your space. No permission is required for knowledge sharing. Pls feel free to give suggestions.

Hi Manikaran,

I’m confused between two policies for my mother who is 59 years old

1. Apollo Munich Easy Health (5 lakh cover) + Apollo Munich Top Policy (Rs 5lakh) – Top up because the premium is low with a deductible of 5 lakh

2. Religare Care (Above 5 lakh cover)

From what I’ve heard you say is that Religare is a new company so servicing still not sure.

So does it make sense to go for Apollo Easy Health – 5 Lakh cover + Apollo Munich Top up Policy of Rs 5lakh.

I’m aware the top up will not work like Religare Care.

e.g. being if I make a claim of 7 lakh then 5 lakh will be contributed from Easy Health and 2 lakh from Apollo Top up policy

and in Religare 7 lakh from Religare Care plan.

But now if I want to make another claim of 2 lakhs, it will not be possible in Apollo, even though my top up of 3 lakh is left because the deductible is 5 lakh.

And this is where Religare Care will come into the picture.

So Manikaran you will suggest Apollo because we have some history to go by right..

Thanks,

Ravi

Ravi, i would advise you to understand the difference between Top up and super surplus policy. Top up is what you have gone through in apollo, super surplus is what united and HDFC is offering.

Also rather than apollo easy health , you should go with Apollo optima restore . I hope this will solve the issue of having a decent sum assured.

Dear Ravi ji,

Whenever a person wants to insure their parents , these are the 2 major deciding factors.

1. Renewal premium at later age . (As there are huge jumps in premium after the age of 60, 65 and 70 )

2. Whats actual (basic) Sum Insured in case of a critical illness , where costs are huge these days and what will happen for a prolonged illness.

In such a case, A basic product of 5 lac and a super top is best Combo.

What do you suggest , Manikaran ji ?

Hi Manikaran and Sumit,

The plans for which I’m thinking of going are

1. Apollo Munich Easy Health Individual Standard (Four lakh cover) plus Apollo Munich Optima Plus (Five Lakh cover) with a deductible of 5 lakh.

Or

2. Religare Care (Five lakh cover)

Apollo Optima Restore Premium is quite high if i compare it against combination of Easy Health Individual Standard and Optima Plus.

Features of Religare Care are much better and premium is also low but it is new in the market.

So the confusion.

I’m aware that the premium will increase till 70 in Apollo.

Ravi …as i replied earlier. I would like you to go through the HDFC ergo Health suraksha top up policy.feature and structure wise it is better than apollo munich optima plus.

Dear Ravi,

Keeping in mind the statistics of health insurance claims for last 5 years, Major claims (Around 85%) are below the amount of Rs 1 lac.

Manikaran ji , Pls correct me if I am wrong. In Financial planning, I believe its important that if we choose a long term path for an objective, we must be able to sustain it in case of worst financial scenario.

Ravi ji, Your mother’s age is less than 60, so lots of options are available right now. You must choose a combo, which you can easily carry forward beyond age 80. Insurance companies charge very high premium after age 70 or 75.

I hereby recommend to make a combo of a small policy of 4 lac Sum Insured and a simple Super top up/Top up of 4 lac deductible will do. Total Sum Insured must be 10 lac. Apollo and Religare are dedicated health insurance insurance companies and they don’t have any other product to back on. Their premium will be hiked every now and then. Where as HDFC and Icici are banking institutions, so there premium have always been steady.

G0 for a steady company.

Don’t choose a flashy product like Optima restore, whose premium is very high and it fails in case of a prolonged critical illness.

Choose a product where annual checkup are available as our parents normally avoid them.

Have extensive body check done for her every third year for heart and kidney.

Sumit, can u pls share the source of the statistics on health insurance claims. It would be an interesting read. But readers should not base there decision on selecting the sum assured for their policies on this data only.

Yes, planning does mean that one should be able to handle all kind of scenarios with comfort (as far as possible). Worst scenarios do include the health issues which has the capacity to wash off all your finances on treatment costs only. That’s why adequate insurance coverage is must. I advise on as much you can afford. Now affordability itself is a subjective word, and unless one has a documented version of financial planning, one cannot ever define his affordability.

Anyhow, I like your idea of getting into a combo…infact this is what Ravi is planning to do. But don’t you think that being Apollo/Religare/max etc. companies are only into health insurance space, this makes them more specialised in this area which is beneficial for the insured. I mean this will make the underwriting strong and if accepted you hve very less chances of claim rejection. Ofcourse customer services also play a big role in this. Also if I agree with you that premiums of icici and HDFC have been steady in the past…but they also have a feature of loading of Premium in case of a claim and this loading can go upto 200% of premium. I don’t know how one should do the cost benefit analysis in this kind of case.

Annual health check ups are being provided by Max, religare and ICICI (may be)…Apollo offers this only after 3 years.

Every policy has some advantages and limitations. So Better to settle down with above average insurer.

Hi,

I have had health insurance for my parents from ICICI Lombart for the past three years via my company. I may go for a job change now. The company rules mention that if I leave the company, the insurance will be cancelled and there will be no re-imbursement of the cancelled policy.

Since the time has come to renew the policy, can I contact ICICI lombart and get the policy transferred via me instead of company ?

Tarun, what you were having was a policy provided by your employer (though you may also be contributing some premium) but the owner of the policy was your employer…and you have added your parents as one of the beneficiaries in that policy.

When you leave the job all benefits will stand cancelled and you cannot renew the policy in your name. This is the main drawback of being dependent on employer’s provided policy. That’s why we always advise to have a separate decent coverage separately other than your employer’s provided coverage.

Yes, you can convert employer policy to an individual one. However, this decision would be with the insurer whether they want to convert or not. Please refer these articles for more information:

http://profit.ndtv.com/news/budget/article-you-can-shift-group-health-insurance-cover-to-a-personal-policy-1292079

https://www.bankbazaar.com/health-insurance/converting-group-health-insurance-to-individual-policy.html

Thanks for sharing this Nishant

If the matter with ICICI Lombart doesn’t work,I have thought of going for Religare individual plan of 4 lakhs each for both my parents ( mother – 65 yrs and father – 70 yrs ). I need your advice on whether I should go for individual plan of 4 lakhs each or a floater of 7 lakhs ?

Tarun, religare is a good policy. Hope you have made necessary comparison among other available options.

But i would advise you to go with individual plan for each of them with SA Rs 5 lakh and above. Individual plan will increase the coverage and the benefits are on higher side when SA is above Rs 5 lakh.

Thanks a lot.

How would you please recommend a policy for my mother. She is diabetic and has hypertention. She is 66 yrs old.

Diabetic cases are not easily acceptable to private insurers. better to chk out options with national insurers. Oriental and national has some good policies.

Hi I am planning to take insurance for my parents . father 68yres and mother 58 years. i have narrowed down to Max bupa… Religare. and Apollo munich.. for my mother. and for father. i would like to go for Religare..apollomunic… but.. will want an advise..as to what plan will be better which wil have less involment of copay. for my fathers policy.

As your father is 68 years of age, there’s no escape from co pay in any policy. Apollo munich optima senior has co pay, even religare asks for copay where someone has taken the policy after 61 years of age. Max Bupa has a feature of co pay for all insured after 65 years of age.

For your mother you should consider among apollo munich and religare as she is just 58 years and is eligible for entry into all policies.

Hi,

I have read through your write up and found it very helpful, i need to take a health plan for my parents & inlaws.

My mother in law suffers from Diabetes, and my mother has gone suffered from cancer 4 years back, however she is normal now. I plan to evaluate National & United Insurance policies, whats your suggestion, also do you suggest i go through an agent to procure these policies or should i walk into a branch off, also would you be able to comment on the claim services offered by both these companies? I would also like to know any other recommendation that you can make.

Both parents are senior citizen

Regards

Supriya

Supriya, Private insureres would normally be reluctant on accepting such cases with diabetes and cancer history. You better check with national insurer only. As you case may demand lot of search and service so better to go through an agent. The premium will not be different in case you go directly or through agent. But do disclose everything regarding the health history on the proposal form .

Hi all of you iam very good to see this site it is very to choose insurance police to their parents. i too also.

Still i need some clarifications that means whether above all companies supports Inpatient ,outpatient bills please any one could explain then it would help very lot.

Vasu, features varies from product to product. Where Inpatient treatment is covered in all the policies, but oupatient bills get rembursed in some specific products. You need to select among various policies as per your requirement.

Hi

Thank you for very informative post about health insurance for parents.

My parents are 69 & 65. Dad has better health , Mom’s overall health is fine but she has hypertension and takes thyroid tablets. Along with them I am planning to take health insurance as well. I am single and 41 yrs.

I have been reading your article and other insurance related ones since morning as i got a wake up call with my friend got hospitalized and expenses of 50K covered by ICICI Pru – I did not like this ULIP product though )

Insurance, the riders, the critical illness, the top ups, etc is all bit confusing to me honestly. I am still trying to get myself trained.

However, I have zeroed in Religare Health Care policy. It looks good for me as well my parents. There is one draw back of it being new entrant, but then every company is new at some point of time, I think we have to take chances and then IRDA does not allow just any ‘other’ company to enter into insurance market.

Two queries please

1) Should I go for 5 lac each for all three of us Individual or Floater . Premium for 5 lac each is going to kill me – I do not belong to elite class.. but then you have suggested that Individual works best. Please note, I sincerely do not want to claim from the word ‘go’.. we are all health conscious but for that ‘nasty big surprise’ somewhere down the lane, I thought of getting ourselves covered. So hopefully, we will have NO Claim bonus for some years.

2) Any insurance buying is easy with click of button, but how to find out which company is the most culprit and they try to find out how to get some reason to reject the claim. I am worried that we pay premium through nose, medical emergency does not come with pre-planned date, so at that point of time, we are focused in getting the patient admitted and minimum insurance procedures of just intimating them.

If you have some insights, it will helpful for layman like me .

Thanks for your time in advance.

Regards

Vikas

Vikas,

Lets first analyse your demography , then we will consider the available options .

Age 65 and 69.

Mother :- Hypertensive and Thyroid (Pre existing disease)

Dad :- Fitness level is better

Any product , which you buy now has following crucial parameters.

1. Premium (now and after age 70)

2. Waiting periods

3. Pre insurance Medical exams

4. Sufficient Sum Insured.

5. Companies, which allow entry at this age.

Mother’s case

At age 65 ( I assume she has not turned 66 now) , Apollo Munich , Max Bupa , Religare , future generali and Royal sundaram offers products , where 100% claim settled.

A person with Hypertension as PED will not be issued policy by Apollo , royal and Future. Max is very costly and have 20% co pay after 65, so Religare is the on;y right choice. But it has 20% co pay if you take 5 lac Sum insured. So take a 4 lac cover for her.

Father’s case

At age 69 Religare and future generali offers products , where 100% claim settled.

Try for 4 lac sum insured with religare or 5 lac with Future.

Q Any insurance buying is easy with click of button

A . unfortunately , for the above demography its not very issue to buy a policy.

Q Which company is good or bad?

A Insurance is a one sided contract , which a person has to accept. Advisor’s role is to explain you all hidden terms and conditions to you and facilitate you in case of claim. If you buy a product, its a legal contract. Nobody can cancel or issue a claim on his own. Its a process , which has to be follow.

Last but not the least

Company is not gud or bad , it the intermediary who may or may not be transparent.

Its India , any company or agent or customer or a system can go rogue anytime.

Hi,

I am thinking of taking a health insurance policy for my dad and mom who are 63 and 57. I found Religare’s Senior Health Insurance plan to be having the least premium for 10 lakhs coverage for both of them under flaoter plan… Could anyone throw some light on the policy and whether its reliable to go with Religare….

Ram, pls go through this link to understand Religare policy

http://goodmoneying.com/insurance-planning/religare-health-insurance-care-review-comparison

I’m looking for family health insurance .my dad age 55 ,mom age 47,I’m 23, my bro is 16 can u help which is best insurance to take.

Don’t make mistake by searching for best…settle down for suitable. Understand the waiting period, sub limits, and other conditions of different policies and chose as per affordability. Your parents are well with in the acceptable range for all company’s policies, so you may also go for floater policy. You should lookt the features of Apollo Munich, Religare health insurance, Max Bupa .

I am looking for Health Insurance Policy for my Parents. My Parents are 72 (father) and 67 (mother) years old. Finding a policy at this stage is challenging. Not only premiums are high, there are high rejection ratios, low claim settlement ratios, high premiums, Co pay and sub limits. Thankfully My Employer has covered my Parents in group Insurance, but I believe the Max age they cover is 80, also I dont want to entirely depend upon my Employer for Health Insurance. My Father has history of hypertension & prostate and mother has diabetics, but thankfully they are under control after taking medicines and never have to go to Hosp for that issue. At their age they are active and take health seriously. I have selected both National Insurance (Varishtha) and New India Health Insurance Sr Citizen Policy, because Max. Sum Insured are low ( I can claim both policies if Bill Amt is greater than SA. in ratio of SA) and Hospital bills are taking new highs. Please suggest me if it is a correct decision and what should I do now to insure health cover for my parents?

Mandeep, I understand your concerns. This is true that at this age it is challenging to get a policy. You have to compromise with the features that are available with sub limits or co pays and all. See acceptability on the part of nationalised health insurance company is very good. I have experienced them accepting riskiest of the cases and as you have written the health issues your parents are facing, so going with nationalised companies is a wise choice.

But how much cover you are actually looking for? As it is cumbersome to claim from 2 insurers. from convenience perspective i advise you to deal with only one insurer.

You may chk the policy available with United India and increase the cover with Super TOP up plan available with them only

Hi,

I’m planning to purchase religare individual insurance with 5 lack cover…she s aged 53 and in good health..

Any inputs with the selection..Also My dad is aged 59 and had a bypas surgery 2 years before, any suggestion for him?

Please advise

Somashekar, for your mother the options are open with all companies. Even Religare is fine.

But for your dad you have to try with different insurers. Every company has its own underwriting guidelines, so its difficult to say which will accept this case.

Generally nationalised companies are seen to accept many difficult cases with ease, and many of them has some good policies too. There are some banks which in tie up with insurers offers some policies where they generally accept pre existing cases, of course with waiting period, like the one offered by PNB in tie up with oriental. You may check those also. But be sure that these tie up policies stays only till the relationship between bank and insurer stays. Do understand the aftereffects if at all you want to go with such plan.

I am confused btwn star n appolo..my parents dun want to go for medical..only pre existing disease is bp. Plz advise.

You cannot escape medical at this age and specially with private players.

There are some nationalised insurers which offers policy in tie up with some banks to its customers where they don’t ask for medical check up. You may try with them. Check with PNB.

What abt red carpet by star ins

.. Ive read its good.. premium is affordable..suits r requirement fr no medical..plz advise.

You are right. Star Red carpet policy is also there. But you should go through its terms first. I feel that this policy tentatively covers 50-60% of medical expenses only due to the multiple restriction it puts on various surgeries and treatments.

I have taken red carpet policy only. Thnks. Nw im confused for investments. Im a small time investor mainly in sip, rd, fd. Are ppf and share trading suitable for my profile ?

Aditi, its better if you consult any financial planner, who can guide you on your requirements looking at your financial profile.

Dear Mani,

I am 28 yesars old and have 2 lacs medical insurance cover provided by my company. I would like to know whether is it required to take additional medical cover with critical illness or to go for critical illness cover directly? Further

1) Is there any company that provides comprehensive health insurance that covers most of the critical illnesses offering sum insured for 10-15 lacs?

2) Could u provide me the claim settlement ratios for Apollo, religare and Star?

3) For only critical illness, which of these gives maximum coverage with cheap premiums for life long: Apollo, religare or Aviva?

4) Among the apollo health insurance plans, which plan is cheaper and has wide coverage and suited for individual

Dear Arun

First and foremost thing one should never be dependent on employer provided cover. One should always have adequate separate and individual health cover.

All companies cover hospitalisation expenses due to critical illness. But if you want specific critical illness policy which makes a lumpsum payment after being diagnosed with illness and surviving for particular time frame, then that also is available with almost all health insurers even life insurers.

– Chk out bajaj alliance, icici prulife crisis cover, and religare and apollo which offers 10-15 lakh of cover.

– Health insurers doesn’t have readily available claim settelment data. You have to search it up with IRDA.

– Health plans have different features which buyer has to understand first and buy the policy which is affordable with in the liked features. Check out the below link to figure out what needs to be checked in a health policy http://goodmoneying.com/insurance-planning/select-best-health-insurance-policy-india

Hi ,

When buying health insurance for parents who are senior citizens , is it advisable to go for a single plan or individual ?

Thanks,

Srinath

As probabilty of health problems in such age is high, so better to buy your parents separate health insurance plan to provide them with adequate cover in case of both of them fall ill or met with some eventuality simultaneously.

This applies to young families too. Atleast after 45 years of age if possible every family member should have a separate insurance cover

Thank you very much for the inputs . How would you rate Religare care insurance plan? The benefit with this plan (in my opinion) is auto-recharge of sum insured if used by 1 person . Apart from that , the benefits like Yearly health check-up , lifetime renewability etc are definite plus .

Would really appreciate if you can give your inputs on this .

Thanks,

Srinath

Srinath, yes Religare care is a good Plan. But keep in mind the co-payment clause if you are buying it for your parents http://goodmoneying.com/insurance-planning/religare-health-insurance-care-review-comparison

Hello Sir,

Plz share your view on max n aviva ‘s new term plan with returns on regular interval.premium is same as compared to all life companies..i have existing life cover which is not as per my hlv..its 60% of my hlv..plz advise..

Aditi, even HDFC has this kind of product, you may check my review of the same here http://goodmoneying.com/insurance-planning/hdfc-click-2-protect-plus-online-term-plan-plus. This will give you my thoughts on this too.

Hello Sir, thanks for info. This plan suits me more max n appolo as its offering long tenure. However my only concern is I am having my existing term plans from hdfc only.its covering 60% hlv.will there be any problem in claiming 3 term cover from same company.Or shall I surrender policies I have taken in 2011 and 2014 and just keep 1.

No aditi, there won’t be any problem in claiming 3 term plans from the same company, provided you make disclosure of your existing insurance policies,every time you purchase a new one. But i think it is better to buy it from different company, and better to restrict number of policies to maximum of 2 or 3 if you can justify the 3rd purchase.

Also last thing I have in my investment list is a health plan for myself. Im confused between star and appolo. In health plan my premium will be constant throughout or that will change with increase in age.

Your premium will change with age. Companies have predefined age slabs on the basis of which your premium will be changed. Understand the policy’s terms and go ahead with what suits you best.

need guidance as my parents are of age 67 and 65 respectively an i plan to have health insurance for them. Could you please suggest the best insurance.. my father has diabetes but he is in good health. My mother also is in good health without any ailments…

Dipesh, you should first try for general health policies. Most companies now days provides cover to senior citizens, with some conditions like copayment clause. Try with Religare or Max bupa in pvt sector and with National or new India in public sector. Since your father is diabetic so it may be difficult to get him good and economical cover, but still make a try. Your mother is healthy and can get cover easily.

For your father if no company accepts his case, then try with Apollo Munich or Star health…these companies have specific policy for diabetics, which should suit your requirement.

Hello Sir,

Please advise about Capital Protected plans by AMC’s. the returns are phenomenal of icici funds.. and also plz advise shall i surrender term plan policies taken 1 and 4 yrs back for 10 and 60 lakhs where i am paying almost 10000, and purchase a new one online for 1 cr in less than 5k?

Hi Aditi.

You are asking wrong question in wrong post. But anyhow, its good that you’ve asked. I have written a detailed post on capita protection funds, you may go through that http://goodmoneying.com/mutual-fund/should-you-invest-in-capital-protection-funds. There’s nothing special about icici funds, moreover its always better to go with vanilla diversified funds so you can re balance your asset allocation at regular intervals.

And shifting your term plan is a good idea if there’s this much of difference. But buy the new one first and then discontinue the existing ones. By the way which plans you are talking of?

Hello sir,

I want to take a health policy for my wife,mother and me,the age of each are 27 years,59 years and 28 years.

All are medically fit.kindly suggest me some good plans to take for my family with a good sum assured as medical expenses are quite high these days.

Better to get your mother a separate policy, otherwise your complete policy’s premium will be calculated on her age. This is also advisable due to high probablity of illness in this age, so its better that she should have an independent cover.

You guys are young, so can go with any company. Just understand the terms and conditions. Check with Apollo, Religare, ICICI and Max bupa. Even for your mother Apollo/Religare should work.

Sir,

1.is the premium to pay one time annually or Monthly ???

2. After how many days/months after paid premium does the Health insurance plan we claim ??

please reply sir my father is 64 years old and suffered from several diseases like Catract, Asthma,Haernia, Liver Chirosis, Gastrics…plz help sir….

Health insurance Premium generally goes annually.

There are different waiting periods which you need to be aware of, post that you could be able to make claim from the policy. For accident cases you may claim anytime.

Since your father is suffering from several diseases, so you need to make the disclosures in the proposal form and let the insurer decide whether they like to give you policy or not. and on what conditions.

Dear Sir – Thank you for your analysis on health insurance plans of banks in association with the nationalized insurance companies like united india, national and oriental especially for senior citizens ! The premiums of these insurance companies are close to 1/3 of retail insurance of private companies, thus making them quite attractive. In this context, appreciate if u can answer the following :

1. Since bank’s have no role in handling the claims, based on your feed back, which of the nationalized banks provide better service in order of merit ?

2. Will these policies have portablity ?

3. Which of these policies are likely to last for longer durations ?

4. What makes these policies premiums lower ?

5. How r these policies compared to policies directly with nationalized insurance companies?

Thanks and kind regards

Please find my answers in line

1. Since bank’s have no role in handling the claims, based on your feedback, which of the nationalized banks provide better service in order of merit?

Don’t think there is any. It is wise to be prepared that Insured and the family would be required to do all the work.

2. Will these policies have portablity ?

To the same Insurer only.

3. Which of these policies are likely to last for longer durations?

Can’t say. It is there prerogative and business sense, on when they want to stop the tie up.

4. What makes these policies premiums lower?

Economies of Scale. Banks can provide Big market to the Insurance houses.

5. How r these policies compared to policies directly with nationalized insurance companies?

Feature-wise i don not see much of difference in many policies. The major drawback is the service and breaking up of tie up anytime.

I have an AB Arogyodaan family floter policy. Who is your TPA. Does it cover naturopathy also?

We are not connected with Andhra Bank in any way, we are just bloggers. You have consult Andhra Bank for that matter.

Health insurance for my mother in-law age 70

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want we can share his contact details, but he may charge fees for the same.

I want to take health insurance for my parents

Father 60 years (Dinetic),Mother (54) (Bp)

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want we can share his contact details, but he may charge fees for the same.

need health insurance for me and my spouse m 57 and my wife is 48

health insurance sum insured 5lacs each

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want we can share his contact details, but he may charge fees for the same.

About medical insurance for my parents

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want, we can share his contact details but he may charge fees for the same.

Medicare insurance for my mother…she will be 70 in three days what is best medical insurance for her

Give quote for Medicare insurance for mother 70years

We are a Financial Planning Firm, SEBI Registered Investment Adviser, do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want, we can share his contact details but he may charge fees for the same.

I’m Dr S K Mishra , 53 years old and looking for health insurance of mine along with spouse and two children.

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want we can share his contact details, but he may charge fees for the same.

i want a medical health insurance to me and my mom

We do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want we can share his contact details, but he may charge fees for the same.

Need health insurance for parents at 76 age as Royal sundaram discontinuing the policy they are carrying.

After withdrawal of a policy they are offering lifeline product.

We are a Financial Planning Firm, SEBI Registered Investment Adviser, do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want, we can share his contact details but he may charge fees for the same.

Best health insurance plan for parents.

How to apply Andhra Bank Arogyadaan Policy through online. Please provide complete details. Thank you

We are an independent financial planning/Advisory firm, not associated with any banker/insurer. Please contact the banker/insurer directly with your query.

Hello very nice to meet you just i want to know i want to take health insurence for my mother it been very helpful if you guide me regard in health insurence and what is the mininim i have to pay for my mother insurance

We are a Financial Planning Firm, SEBI Registered Investment Adviser, do not deal in health insurance products. But we can provide you with a trusted source who can help you select the right product. If you want, we can share his contact details but he may charge fees for the same.

Health insurance plans for parents. Canara Bank is no longer associated with Apollo Munich. How to compare other plans?

TATA AIG -CANARA bank and Religare group care-PNB?

i am searching for a health policy for my parents… how about considering group policy offered by nationalized banks… which one is best

Yes, it is definitely an option, but these days many of these tie-ups are seen broken. So, when the tie-up brakes the premium shoots up. Plus, you may find service issues as well. So, it would be wise to go for an individual cover.