The pandemic has once again taught us the lesson on how important it is to take care of our health. It is equally important to have decent health insurance as well, to protect the finances from the health emergencies that may arise anytime. (Also Read: Lessons learned in the year 2020)

LIC has come up with the Arogya Rakshak Health Insurance Plan in July 2021. It is in succession to the Jeevan Arogya Plan, which stands withdrawn.

The plan mainly covers the cost of major surgeries and the daily hospitalization expenses. Some other benefits are also there.

Let’s see how it works, some of its distinct features, and does it makes sense to opt for a health insurance plan from LIC?

LIC Arogya Rakshak- in Brief:

Health insurance plans run by general insurance companies will cover hospitalization expenses up to the assured amount. It is referred to as indemnity-based coverage.

Unlike the indemnity-based cover, the LIC Arogya Rakshak is a health insurance plan from a life insurance company that provides a fixed benefit in the event of hospitalization, despite the costs incurred on the treatment.

It can be taken both as an Individual Cover and a Family Floater cover with the main family member being the Principal Insured (PI). Other family members may include- Spouse, Children & Parents.

The minimum age for the Principal Insured, Spouse & Parents is 18 years and the maximum is 65 years to enter into the policy. They would be covered until they become 80. Children can be covered between the age of 91 days to 20 years, until the age of 25 years.

(Also Read: How to get Health Insurance for Parents?)

How does this work?

Rather than choosing the sum assured, as we normally do while buying a health insurance cover, here you need to opt for the daily benefit required for each family member at the start of the policy. You can choose between Rs. 2,500 to Rs. 10,000, in multiples of 500. It is called Initial Daily Benefit (IDB) or Hospital Cash Benefit (HCB). Other benefits available in the policy would also be based on the IDB chosen by you.

The premium of your policy would also be decided on this and other underwriting criteria like- age, gender, etc. However, to encourage you to go for a higher cover, LIC has provided a premium rebate on choosing an IDB of more than Rs. 4,000.

In the event of hospitalization exceeding 24 hours (only in India), the Initial Daily Benefit chosen would be payable for each day, irrespective of the costs incurred, during the first three years of taking the policy. Post-that, this Applicable Daily Benefit (ADB) would increase 15% every three years, a maximum of up to 1.5 times the IDB opted. It is called Auto step-up Benefit.

In case of ICU admission, exceeding 4 hours, twice the benefit chosen would be applicable for all the days spent in the ICU.

However, it is important to note that, in the first policy year the ADB would be provided for a maximum of 30 days, and from the second year onwards it would be extended till 90 days. Also, a maximum of 900 days of hospitalization can be covered during the lifetime of the insured person (including the ICU stay).

If the hospitalization is done for undergoing any major medical surgery, a surgical benefit equal to 100 times of the IDB chosen would also be payable over and above the Hospital Cash Benefit, subject to certain categories. It is called Major Surgical Benefit Sum Assured.

A maximum of up to 10 times of the Major Surgical Benefit Sum Assured would be covered in the lifetime of the person insured.

However, if the sum assured for major surgeries is exhausted in a particular year the plan provides the Restoration feature as well, subject to certain conditions, not exceeding the maximum lifetime limit. (Also Read: What is Restore & Recharge in Health Insurance?)

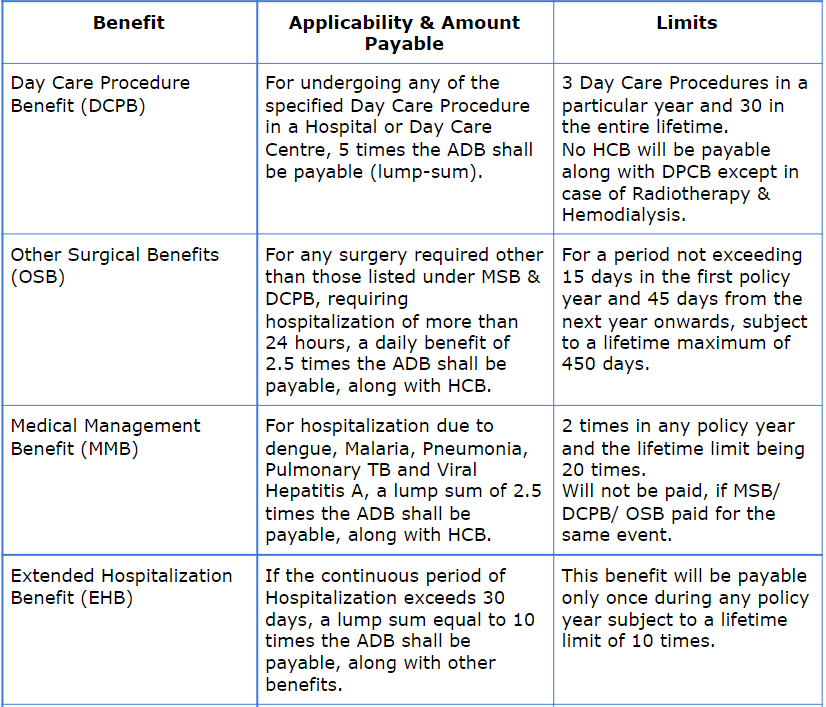

Other Key Benefits & Applicable Limits:

Apart from the Hospital Cash Benefit & Major Surgical Benefits, some other benefits are also available in the LIC Arogya Rakshak health insurance plan, with certain limits as summarized in the table below:

LIC Arogya Rakshak- Important Highlights:

- In case of a major surgery, if emergency use of Ambulance is done for transportation, a lump sum amount of Rs.1000 would be payable and the premium would be waived for that year.

- Reimbursement of Health Check-up bill once in 3 years upto a maximum limit of half of the Applicable Daily Benefit (ADB).

- After every claim-free period of 3 years, a No Claim Bonus equal to 5% of the IDB would be added to the Applicable Daily Benefit (ADB).

- On death of the Principal Insured, if the age of insured spouse/parents is less than 70 years and that of insured children is less than 25 years, a Auto Health Cover (AHC) benefit would be triggered. Here, they would be covered in the policy till they reach that age (70 & 25, respectively) without any further premium payment, subject to a maximum period of 15 years.

- The insured has the option of receiving 50% of the eligible major surgical benefit as an advance if he or she undergoes any eligible major surgery in a network hospital. The amount would be credited to the insured’s bank account during the hospitalization period itself instead of waiting to make a claim after discharge. This would be adjusted in the final settlement.

- A general waiting period of 90 days is there in case of hospitalization due to surgery or sickness. No waiting period if the surgery is due to any Accidental Injury. There is also a specific waiting period of 2 years for covering hospitalization or surgery on account of diseases like- Cataract, Hernia, Piles, Gallstones, Kidney Stones, Ulcer, Slip disc, Knee/joint replacement (other than accident), etc.

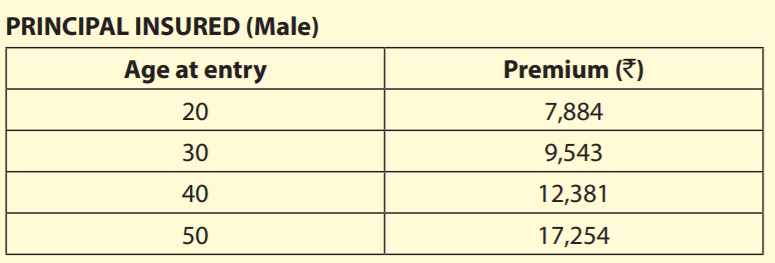

- The premiums can be paid annually or half-yearly and are subject to a revision after every three years. Insured has an option to cancel the policy upon such revision. Here’s the indicative premium chart for the IDB of Rs. 5,000, provided in the policy sales brochure by LIC.

(Also Read: How to choose the best health insurance policy in India?)

LIC Arogya Rakshak- Should You Buy?

LIC Arogya Rakshak is not a replacement for a Comprehensive Health Insurance Plan. Although the plan offers a number of lump-sum benefits, irrespective of the costs but with various limits attached.

Seeing the cost of healthcare in today’s scenario, the Daily Benefit limit seems quite less and may not be sufficient to cover the hospitalization costs. Even if we consider the step-up benefit, it may not cope-up the rising medical inflation. (Also Read: What is inflation & how it impacts your financial plan?)

Also, the costs of all major surgeries may far exceed the ADB limits and may not get fully covered. For other facilities like Day care treatment, other surgical benefits, etc. the maximum limit is only 50,000.

In addition, the premium seems to be a bit on the higher side as compared to the indemnity health insurance plans which offer a far superior coverage than this plan. The premium revision period of 3 years is also a red flag, it is generally 5 years in the indemnity plans.

Pre and Post Hospitalization Expenses, other Modern Day Treatments are not covered along with a long list of more than 30 exclusions.

You may not be in a position to port the policy to any other insurer, as it is offered by a life insurance company that doesn’t come under the IRDA Health Insurance Portability norms.

So, all in all, do not fall into the trap of this Arogya Rakshak health insurance plan from LIC and go with a comprehensive indemnity-based health insurance cover for all family members of adequate sum assured. (Also Read: Is your health cover enough to cover all risks?)

To further enhance the health cover, you may go for the super top-up plans offered by health insurance companies. (Also Read: Ways to enhance health cover)

A medical emergency fund of an adequate amount is also advisable for the expenses which are not covered by health insurance plans. (Also Read: How to manage financial emergencies?)

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}