LIC Jeevan Akshay VI is an immediate pension plan, which creates a regular income stream from the very next month of Investment. You may ask for Annuity as monthly, quarterly or annual payment mode option.

Immediate pension plans are important to study especially for those who have invested in some deferred pension plans of any insurer or even invested in NPS. Both these products, on maturity, mandate investors to put some of their accumulated money in the immediate pension plan and buy regular annuity options.

In this article, I will be reviewing the features and benefits of LIC Jeevan Akshay VI for readers to consider it one of the options while buying annuity from their pension products. This Plan is replaced by a new pension Plan LIC Jeevan Akshay VII, which is also reviewed on this blog, click here to check.

LIC Jeevan Akshay VI – in Brief

LIC Jeevan Akshay VI is a guaranteed lifetime pension plan, which starts paying pension from the next month of the Investment or as per the mode was chosen. The other immediate pension plan launched by LIC backed by Government of India is Pradhan Mantri Vaya Vandana Yojana.

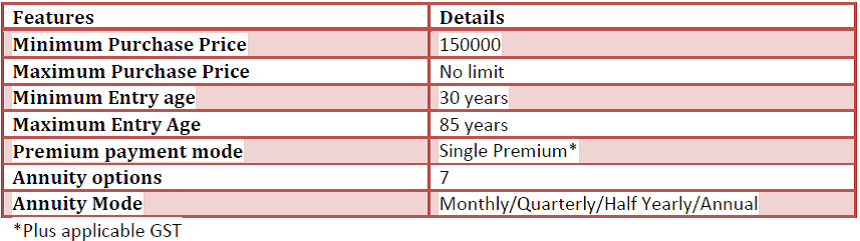

Unlike PMVVY, LIC Jeevan Akshay VI can be purchased by people aging 30 years and above, with a maximum age limit of 85 years. The rate of Interest is better in PMVVY but the tenure and the maximum investment limit is high in LIC Jeevan Akshay.

LIC Jeevan Akshay VI or any Immediate pension Plan for that matter, requires a Lump sum premium payment and depending on the Mode of receipt (Monthly/Quarterly/Half Yearly/Annually) you have chosen, starts paying the pension amount as per the annuity option you have opted for.

(Also Read: How pension Plans in India Works?)

LIC Jeevan Akshay VI – Basic Features

LIC Jeevan Akshay VI can only be bought Online on lic website

LIC Jeevan Akshay VI – Death/Maturity/Surrender benefits

There is no death benefit attached to LIC Jeevan Akshay.

There is no Maturity benefit attached to Jeevan Akshay. However, if you have opted for “Return of Purchase Price” annuity option, you or your family as the case may be will get the purchase price back on completion of the term.

(Also Read: Why Personal cash flow analysis is important?)

Being an annuity Plan there are no Surrender benefits attached as you cannot surrender the policy in between the policy term. This is what is mentioned in the product features too.

However, I have read some websites mentioning that in LIC Jeevan Akshay Plan, You are allowed to surrender the Plan in 2 conditions, provided you have bought the Policy under “Return of Purchase Price” annuity option. The conditions are:

- You have been moved to another country Permanently

- You get diagnosed with any of the specified Critical Illness.

But, it is advisable to confirm the surrender conditions from LIC office

LIC Jeevan Akshay VI – Annuity options

There are 7 annuity options in LIC Jeevan Akshay VI Plan. Below are the details

- Annuity Payable for Life at Uniform rate: The Pension/Annuity amount will remain same till you are alive

- Annuity payable for a certain term (5,10,15 or 20 years) and thereafter as long as the annuitant is alive: In this option, an annuity is paid for a certain period, irrespective of the Investor is alive or not, and thereafter till the annuitant is alive.

- Annuity for Life with the return of purchase price on the death of annuitant: This is something like bank FD with Interest payout. Where you will get the pension till you are alive and later on the Invested money will be returned to your nominee.

- Annuity Payable for Life increasing at a simple rate of 3% – In this option, your annuity will keep increasing at 3% annual simple rate. For e.g. you are getting a pension of Rs 20000 in the first year, 2nd year in this option you will get 20600, the third year the pension will be 21200…and so on. (HDFC Immediate annuity has 5% escalation clause)

- Annuity for life, with 50% payment to wife on annuitant’s death – Means if Rs 100 is the pension which the investor is getting, after his death, Rs 50 will be the pension paid to the spouse till she is alive

- Annuity for life, with 100% annuity to wife on annuitant’s death – Referring to the above example, the spouse will keep getting Rs 100 as annuity even after annuitant’s death.

- Annuity for life, then 100% annuity to the spouse, and then return of purchase price to the nominee.

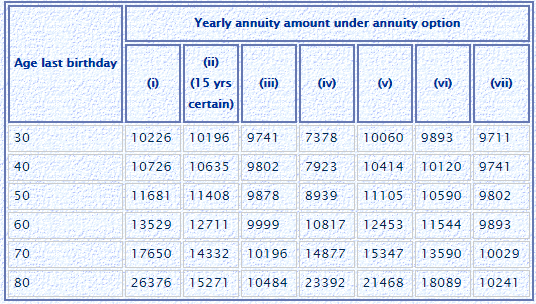

LIC Jeevan Akshay VI – Annuity Rates

The below table shows, the INDICATIVE Annual payments, in the case of Rs 1.50 lakh of the Purchase price. Please note that along with the purchase price you will be charged with 1.8% of GST.

These are the indicative rates. The final rates at the time of actual purchase will apply

You may clearly see here that Higher the age, Higher will be the Pension amount and More you leave with the company, higher will be the pension amount.

The annuity rates in case of 30 years old for Option 1 and Option 7 comes out to be 6.81% and 6.47% respectively (Excluding GST)

The annuity rates in case of 70 years old for Option 1 and Option 7 comes out to be 11.76% and 6.68% respectively (Excluding GST)

LIC Jeevan Akshay VI – Should you Buy?

As I wrote above that in some cases you have no option but to consider immediate annuity plans. It is a mandatory buy in case of the new pension scheme and deferred pension plans. The question comes should you go with LIC Jeevan Akshay VI?

In my view, it is worth considering. Now days almost every insurer has this kind of product in their portfolio, I have reviewed HDFC Immediately pension plan earlier on this blog. You have to compare what you are getting from where and decide what suits you the best.

Some days back I read LIC Jeevan Akshay is being discontinued by LIC and it may be relaunched with revised rates. The same article says that this pension plan generates 25% of new premium income for LIC and is termed as a Cash cow for the insurer.

So I do not think to discontinue may even be a considerable option for LIC…but, yes In falling interest rate scenario, Rates may get revised soon.

LIC Jeevan Akshay VI offers returns that are half a percentage points more than the 10-year government securities.

But if the requirement is just to provide for or supplement monthly/Annual income, then you may also consider other fixed return instruments like Post office MIS, Senior citizen schemes and even Bank FDs.

Hope you are clear on the workings and features of LIC Jeevan Akshay VI Pension Plan. Feel free to ask your queries or doubts in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Hello,

Please advise, what if I invest 20L in Jeevan Akshay VI. My age is 51 and currently unemployed.

Unsure of getting employed, I require some immediate guaranteed monthly income lifelong. Any other suggestions is also appreciated. Thank you sir,

I think you should not block your money in LIC Jeevan Akshay. Better to get all the options evaluated like SWP in Mutual funds, post office deposits and other instruments and then decide as per your requirement.

You should also review your Health insurance and other goals along with.

In short get a Holistic Retirement Planning done for you.

what is the rate of interest for jeevan akshay VI considering monthly annuity

LIC has withdrawn Jeevan Akshay VI plan, it will not accept any fresh investment in the same.

LIC is deducting Rs. 3600 every month on jevan akshay monthly annuity of 11867. This single premium of RS 20 lakhs came out of NRE account. And income tax rule exempts me from taxes upto 2.5 lakhs per year. So why is LIC deducting 3600 every month. its more than 30%. How should I stop LIC from deducting.

Looking at your query, it can be said that LIC is right in deducting TDS.

As per our knowledge, if you do not want the TDS to be deducted as you feel that you might not generate any taxable income then you may file application u/s 195(3) to jurisdictional tax officer to obtain a certificate of Non-deduction of TDS or Lower TDS.

If the Income-tax officer grants the waiver then you can submit that waiver certificate to the LIC office to not deduct TDS on high rates.

KIndly, also contact LIC, asking for the solution of the issue.