Post office MIS is quite a popular and sought-after product to create monthly income. The name “Monthly Income Scheme” has its own attraction, and every second small saving scheme investor prefers this scheme. It is a favorite among the retired people.

Even if someone does not require Monthly Income, they were pitched Post office MIS in combination with Post Office RD. This combination is looked upon as the safest option which gives “2 ki Shakti” i.e. Returns of MIS plus returns of RD.

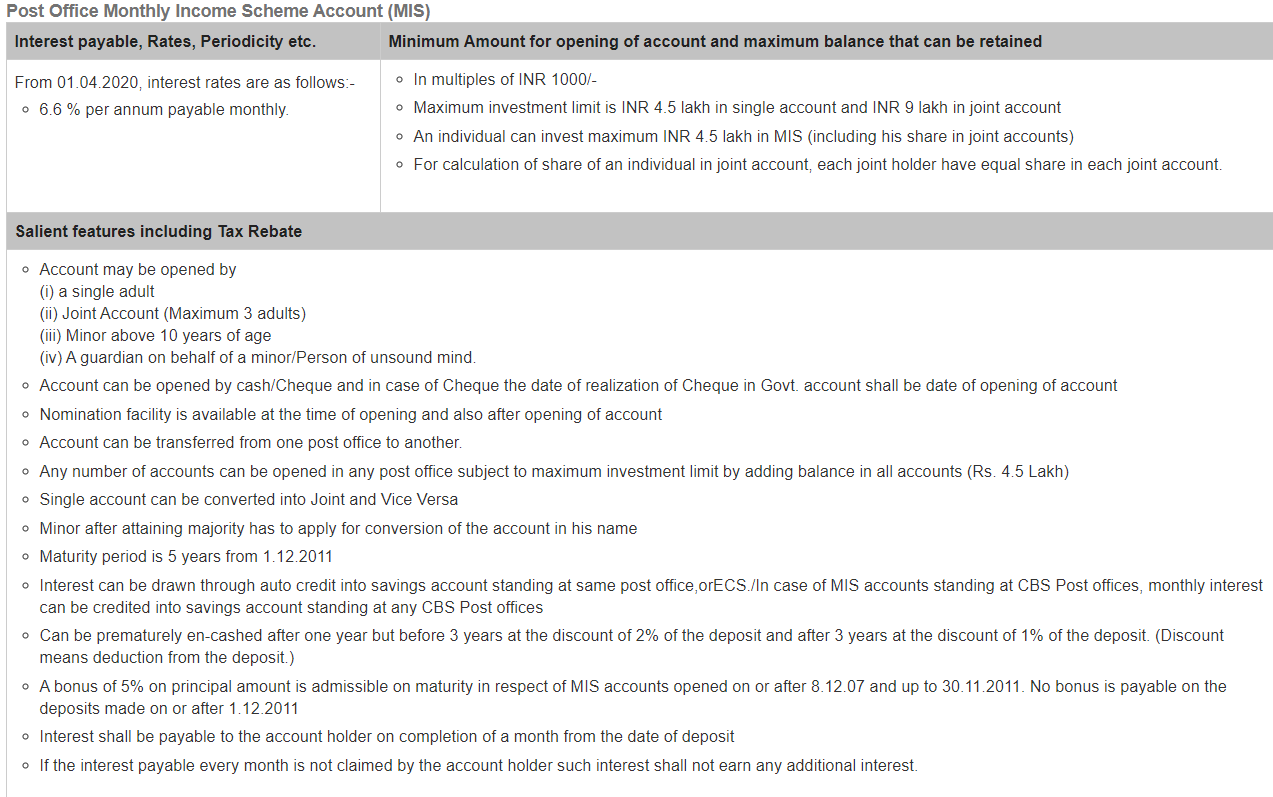

Post Office MIS (Monthly Income Scheme) – Salient Features

The salient features as taken from India Post website are self-explanatory. The main points to look upon are the maximum limit in single and joint Account is Rs 4.5 lakh and 9 lakh respectively. Now as per the Union Budget 2023 the maximum limit in the single and joint account is Rs. 9 lakh and 15 lakh w.e.f 1st April 2023 individually.

The depositor will get monthly interest payout. Though the Rate of interest in Post office MIS is reviewed every quarter, once opened the account will be at the same rate till maturity.

The Interest earned is taxable in Post office MIS

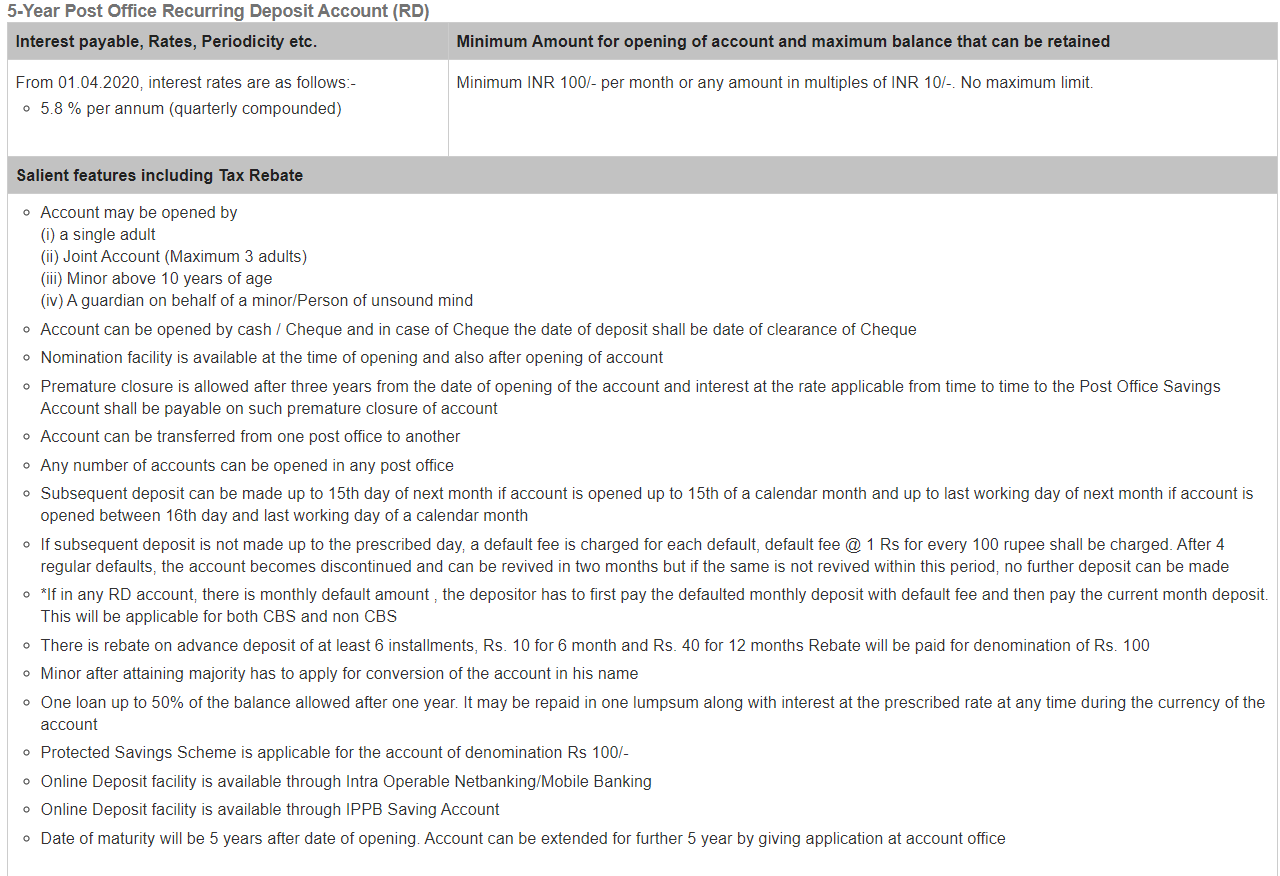

Post Office RD – Salient Features

A Recurring deposit is a product where you can deposit on monthly basis and earn better interest than the saving bank account. Unlike the Bank’s Recurring deposit which can be taken for any tenure, the Post office RD has a single tenure of 5 years.

Post Office MIS with Post Office RD – How much return can we expect from this combination?

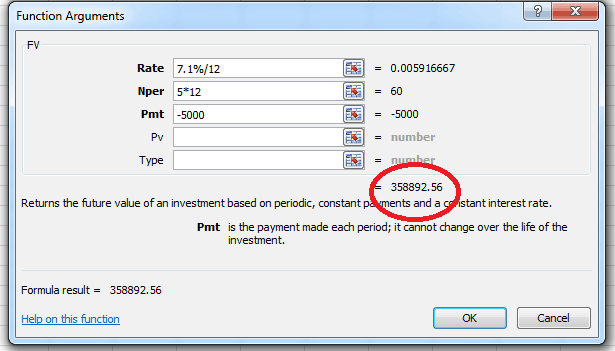

Both are 5 years products, Post Office MIS pays monthly Interest (@7.5%) and Recurring deposit Accepts monthly deposit (@7.1%). Please remember the rates mentioned are the current rates on the date of writing this post, and the rates get reviewed and may get revised every financial quarter.

If someone does not need monthly income, then one may invest in both these products simultaneously and keep investing the Interest payout from Post Office MIS into Post office RD.

Post office MIS with RD calculations

To keep the calculations simple, i have assumed the Investment amount in POMIS to be Rs 8 lakh, and that generates Rs 5000 per month @ 7.5% (Current Rate of Interest).

This Rs 5000 to be invested monthly in Post office RD @ 7.1%.

The maturity amount in Recurring deposit comes out to be Rs 358892.56.

Total Investment – Rs 800000 in POMIS

Total Maturity value (After 5 years) – Rs 1158892.56 (Post Office MIS+ Post Office RD)

So the CAGR or the Annual Interest comes out to be as 7.69%.

Please remember that all the return numbers are Pretax, so whichever slab one may fall into the overall return will get reduced with the tax outgo.

Conclusion:

This is clearly visible from the above calculation that even after combining both the products the return percentage does not become as high as generally expected. The Pre-tax returns from this combination would be far lesser than the Senior citizen saving scheme.

I do not find any reason to go for this combination of products. It may suit the Post office agents as this leads to the selling of 2 investment products to the customer

However, on the other side, 7.69% is better than 7.5% of Post office MIS. And 7.5% is better than 6.75% as now a day’s bank FDs offer.

If one does not need monthly income then one may also consider Mutual fund SIPs, maybe into Some Hybrid kind of products which has better potential to generate better and tax-efficient return than Post Office RD.

{kind=link}

How I would like to understand this hypothesis?

I understand it simply that the interest earned from an MIS scheme is immediately (without loss of even a single day) invested in an RD scheme and that’s the only game here. And of course the discipline (which any how would have been there because both the Schemes are time locked).

Otherwise, you independently earn from an MIS scheme and independently invest and earn money from the RD account. And that would be the same.

Kamal Ji, this post is just to show the kind of returns one may expect from combining both the post office schemes. I have heard many stories where investors were told that this combination will generate higher returns than other available schemes, as in the article I wrote about SCSS, and people normally get misled.

Respected sir,

Please let us know if we can have a MF combination of MIP and SIP. Please explain what kind of returns can be expected. MF returns will be Tax free,

Therefore better returns can be expected. Please give your expert comments and views.

Yes, you may combine MF with MIP, but since MFs are not fixed return instruments so committing any return may not be possible. Still, give time to your investment, it has high probability of generating better returns than PO RD.

Dear Sir

I understand that returns from both PO MIS and RD are taxable. But how exactly the returns are treated under tax rules? Are returns taxable separately or they can be combined? Does the taxes are to be paid every year or after the maturity i.e. 5 years? Please give your expert advice on taxation of returns from combined MIS & RD in post office. Thanks

POMIS pays interest monthly so has to be counted in your income once it is received. RDs calculate the interest quarterly, so whenever the interest gets accrued has to be counted in your income.

Both have to be considered separately and counted in the year of accrual/payment.

Hello Sir,

Could you please suggest which is the best option to invest for 5 years? FD, RD or MIS in Post office.

Product selection depends on your requirement and risk appetite. For 5 years, i may have advised you balanced advantage fund, but still, it is wise for you to contact your financial planner for this.

At one side in your precious advice you are writing return of Post-office RD = 7.1% quarterly compounded but actually you are calculating Rs.5,000 monthly RD interest @6.91864% quart.comp. & due to this your figure of maturity comes Rs.11,58,892.5

In real position RD OF POST-OFFICE @7.1% quart.comp. GIVES FINALLY INTEREST Rs.3,60,614.8 + (M.I.S) 8,00,000= Rs.11,60,614.

Please make correction.

Thanks, Prabodh for checking the calculation and pointing out the mistake. However, since I know that I have not done the quarterly compounding so I have mentioned in the article that “The actual numbers would be a bit different since the above calculation is of Monthly compounding whereas in Post Office RD the compounding would be quarterly.”

But your point well taken.

Sir

Your views on investing in RBI floating bonds for a regular income. Or else which would be better PMVy pension scheme from LIC or a TD with Post office. I have a bank FD maturing this month and I want to invest this 10 Lacs

Kindly guide me

Thanks and regards

Shrikant

Hello Mr. Karadgi,

It becomes really difficult for me to comment on the suitability of the products without knowing your financial profile and other requirements. But I would say, if the requirement is regular income then, you can go with a combination of all these in equal proportion to optimize inflation and taxation.