Pension Plans in India have gone through a sea change in the last 1 year. Earlier these plans used to be sold as Investment products and can be withdrawn any time after making few premium payments. But now days pension plans means the plans meant for getting pension in retirement years. I have done reviews of some pension plans in India like HDFC pension plan and Reliance pension plan which were launched with this new structure , and found that more or less all plans are same and even the new plans are also coming up with the same flavor. So here is the detailed structure that you will find in almost all pension plans in India. This article will give you the idea on how pension plan in India works and if at all you want to go ahead with any such product you would know what to ask the seller.

Pension plans in India – In Brief

The structure of any pension plan has 2 parts – Accumulation and distribution. You pay premium every year (for the required term selected) which gets invested in the fund/asset of your choice after deduction of charges and at the time of vesting* you have two choices. One you can ask the insurance company to start your pension/annuity (as per the available annuity options) or alternatively you can withdraw the money and purchase immediate annuity plan from the same insurer. If you don’t want to start the pension/annuity immediately, you may buy a single premium deferred pension product or you may delay the vesting age.

*Vesting is granting the right for receiving pension benefits.

You may also commute 1/3rd of the fund value on vesting date and receive it Tax free. The remaining amount must be used to purchase annuity**.

**Annuity is specified income payable at stated intervals.

Compulsory features in Pension Plans in India

Guaranteed Maturity Benefit: All pension plans in India should be having a feature of guaranteed maturity benefit which would be Fund value or 101% of Premium paid, whichever is higher. This feature is to provide safety to the invested hard earned money of policy holder.

Guaranteed Death Benefit: If the policy is not in discontinued status, it carries a guaranteed death benefit which is equal to 105% of the total premiums paid plus all top ups if any. This amount will be paid to the nominee of the policy holder in case of unfortunate death of policy holder. If the policy is in discontinued status then the nominee will get the funds lying in the Policy Discontinued fund.

Nominee will also have 3 options to utilise the funds: withdraw the entire death benefit or utilise the entire proceeds to buy immediate annuity plan or withdraw part of the proceeds and use the other part in buying annuity plan.

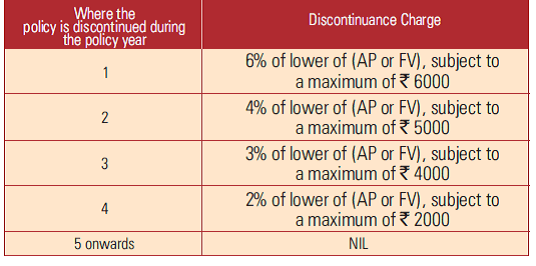

Surrender/Discontinuation: Unlike earlier where the premium paid gets forfeited if policyholders don’t the pay continuous premium for at least 3/5 years, now insurers won’t be able to do that. Infact this condition applies to all ULIP plans and is not limited to pension plans only. Now you may discontinue paying premiums or even surrender the plan whenever you want to. The condition is if you discontinue or surrender the plan within first 5 years of start of policy then your fund value on date of surrender will be shifted to Policy discontinuation plan after deduction of specified charges. This Discontinued fund will also earn you 4% p.a on the funds lying. You may withdraw the fund after completion of 5 years. But as per the new features of pension plans in India, the surrender proceeds has to be utilised either to purchase an immediate annuity plan or single premium deferred pension product. Standard discontinuation charges are as below.

But if you surrender the policy after continuing it for first 5 years, then fund value will not be transferred to any discontinued fund account but the proceeds has to be utilised to buy annuity (immediate or deferred). Thus we can say that after buying pension plans in India you cannot escape from pension.

Besides the above there are some product level features which may vary from company to company like Minimum/maximum premium, Allocation charges, Fund management fees, mortality charges etc. Some pension plans in India has features of giving some additional units to the regular disciplined investors. This would be the USP of those products.

Should you invest in Pension Plans in India?

One thing is very clear that we cannot ignore Retirement planning in India. Though Indian youth especially those working in private sector are not yet paying heed on this, but sooner or later they have to agree on this front and Plan judiciously for those years when they will not be receiving regular paychecks. Keeping this in mind regulator has changed the complete pension space in India. To reduce the future burden on self, government has also started with New pension scheme and moved from Defined benefit to Defined contribution.

This New Avatar of Pension Plans in India calls for only Serious Investor. But one who’s actually serious on retirement planning front has to figure out “Is pension plan the only solution to secure retirement?” Pension plans are one of the mediums which will help you accumulate the corpus for retirement, but for accumulation there are many other products also which if used judiciously and with planning can prove to be flexible, cost effective and tax efficient ways to invest.

I believe Pension plans in India are designed to make you more disciplined and organised, and you are required to pay some charges for that.

Do you think Pension plans in India are suitable products for your retirement planning? Share your views.

{kind=link}

Private Schemes are specifically devised by the employer. Whereas, government policies adhere to the plans under the National Pension Scheme which are extremely famous. Initially, government schemes were open to only Government employees, however, later were made available for all citizens of India. pension plans are devised in a way in which you invest regularly during the span of your career. You receive the labor of your investment in a lump sum at your retirement There are two types of pension schemes, i.e. Private and Government.

I want to know about pension policies of 2010 tp 2017