With Retirement planning gaining importance, especially after the Push towards NPS by government, it has become important to understand immediate annuity products.

New pension scheme and even other Insurance pension scheme require investors to buy annuity from the maturity or surrender proceeds of the Policy. Though 40% from NPS maturity and 1/3rd from Insurance pension plan can be withdrawn in lumpsum and tax-free, but for the balance amount, one has to compulsorily buy annuity.

Also Read: NPS withdrawal rules

One can buy annuity from the same insurer or can invest the lump sum amount in an immediate annuity product of some other company to start with pension.

This article is to review one of the immediate pension plan, HDFC Life new immediate annuity plan.

HDFC Life new immediate annuity plan – In brief

HDFC life new immediate annuity plan is a non-linked traditional annuity plan that offers a guaranteed pension income stream depending on the option one has opted for.

- There are various annuity options (on Single and Joint life),

- There are various modes of annuity payments (Monthly/Quarterly/Half Yearly/Annually)

- Annuity rates may be different for different options and mode of annuity.

- Annuity rates also keeps on changing depending on the prevailing economic conditions.

You need to choose the option and mode of annuity, pay the purchase price (Investment/Premium amount) and you will start receiving the pension/annuity from next payment date as per the mode chosen. Please note that you cannot change annuity options later.

Annuity is an important part of financial plan and thus please do take time to understand what you are purchasing.

HDFC Life New Immediate annuity Plan – Basic Features

- Minimum age to buy annuity – 30 years

- Maximum age to buy annuity – 85 years

In case Investor is below 30 years of age, then the proposal would be accepted only in the cases where HDFC Life is bound by some contract.

Also, if this product is to be purchased as QROPS (Qualifying Recognized Overseas Pension Scheme), through transfer of UK tax relieved assets, it would be offered only to customers who are 55 years of age or above.

Minimum annuity Pay-out:

Monthly – Rs 1000 ; Quarterly – Rs 3000 ; Half Yearly – Rs 5000 ; Annually – Rs 10000

Maximum annuity Pay-out:

NO LIMIT in all modes

However if the Purchase price of Annuity is coming from NPS or a HDFC Life administered contract (Pension Plan), then it would accept cases with no minimum annuity condition.

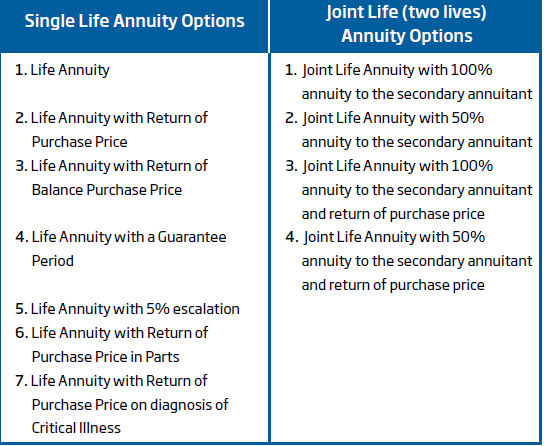

HDFC Life New Immediate annuity Plan – Annuity Options

Let me explain these options here for a better understanding.

Single Life Options:

- Life annuity – You will get a fixed amount as per the mode chosen, for life. Your Investment /Purchase Price will not be returned back to your nominees. This is the reason the annuity rates would be highest in this option.

- Life annuity with Return of Purchase price: You will get a fixed amount as per mode chosen, and on your death your nominee will get the investment amount back.

- Life annuity amount with Return of Balance Purchase Price: You will get a fixed amount as per mode chosen and on your death your nominee will get balance purchase price, which would be Purchase Price less total annuity paid till date of death.If the annuity paid is more than the purchase price then nothing will be paid to nominee.

- Life annuity with a Guarantee period: You will get a fixed amount as per mode chosen for life or till the end of guarantee period whichever is later. The annuitant has the option to choose guarantee period of 5 or 10 or 15 or 20 years.

- Life annuity with 5% escalation: Here a fixed annuity amount is paid to the Annuitant, which keeps on increasing @5% p.a. Nothing is paid back to nominee on annuitant’s death.

- Life annuity with Return of Purchase Price in Parts: You will get a fixed amount as annuity for Life. After 7th year of policy continuance 30% of purchase price is paid back to the annuitant on survival. Balance 70% of purchase price will be paid to nominee of the annuitant on his death. If annuitant dies within first 7 years, then nominee will be paid back complete Purchase price.

- Life annuity with Return of purchase price on diagnosis of Critical Illness: You will get a fixed annuity for life, but if you get diagnosed with 6 specified illness before 85 years of age or dies during the policy continuation, then you or nominees( as per the situation) will be paid back 100% of purchase price.

Joint Life Options:

- Joint Life annuity with 100% annuity to Secondary annuitant: You will get fixed annuity till you are alive, after you, your spouse will keep getting same annuity till death. No return of purchase price to nominee.

- Joint Life annuity with 50% annuity to second annuitant: You will get fixed annuity till you are alive, after you, your spouse will get 50% of same annuity till death. No return of purchase price to nominee.

- Joint life annuity with 100% annuity to secondary annuitant and return of purchase price: You will get fixed annuity till you are alive, after you, your spouse will keep getting same annuity till death. On the death of last survivor, 100% of purchase price will be returned to nominee.

- Joint Life annuity with 50% annuity to second annuitant and return of Purchase Price: You will get fixed annuity till you are alive, after you, your spouse will get 50% of same annuity till death. On the death of last survivor, 100% of purchase price will be returned to nominee.

HDFC Life new immediate annuity Plan – Annuity rates

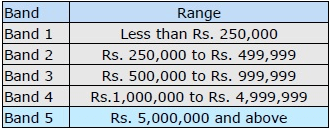

Annuity rates vary with age, with the option that has been chosen and the mode of the annuity. It also depends on the Purchase price, which further has been divided into different bands.

This means that if you want to buy annuity for Rs 10 lakh, then you will get rates of Band 4.

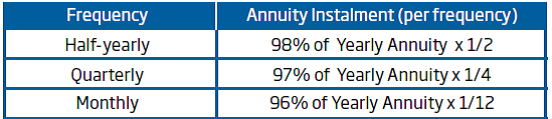

Conversion of annual payouts:

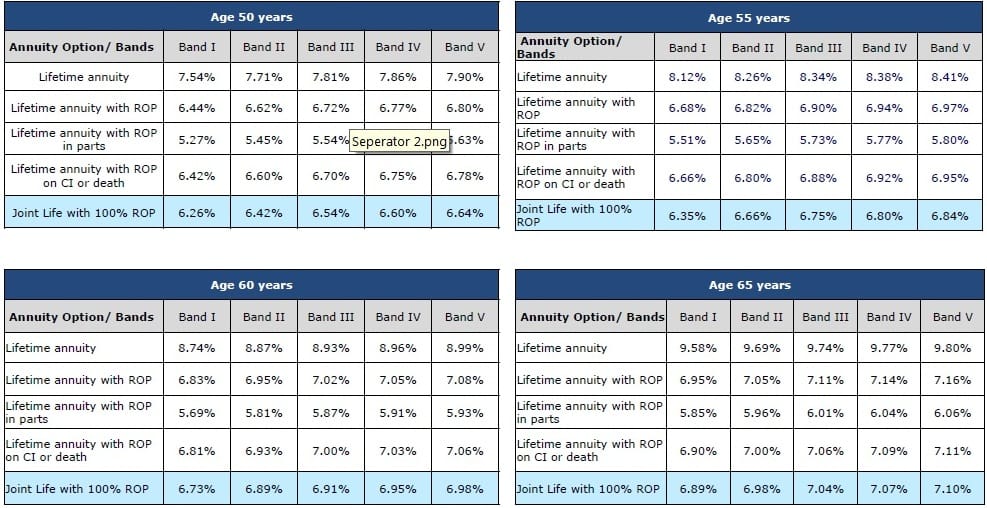

HDFC Life new immediate annuity plan – Annuity rates

These rates are as on 23rd July 15, and are subject to change.

As per the above rates, if you are 60 years of age, and would like to buy annuity with Rs 10 lakh purchase price, with option Lifetime annuity, then you will start getting Rs 89600 per annum as fixed pension amount.

In case you want to opt for monthly pension, the amount would be 96% of 89600 divided by 12, means Rs 7168/- per month.

The Purpose behind showing you these rates is to give you an idea on what to expect from annuity payments and what is the current interest rate scenario going on.

The above data clearly shows that Payouts are higher for higher age people, and more in Life time annuity option. If you want to get your purchase price back, then your payouts will reduce.

Do remember that your purchase price is subject to Service tax @1.4%, unless it is coming from New pension scheme (as per budget 2016)

HDFC Life New Immediate annuity Plan – Should you invest?

Ultimate aim behind retirement planning is to ensure the regular flow of income through arrangement of savings corpus. Along with regular inflow, growth of the corpus is also very much required, so the savings should not get beaten down by inflation during post-retirement years.

Immediate annuity plan is one of the products to create a regular income stream. You may also compare and invest in other products for this requirement, but when your money is coming from New pension scheme or any other Insurance pension Plan, then immediate annuity plans are something which you cannot avoid, as it is one of the conditional feature in pension products.

Though HDFC is not the only Insurance Company offering such Plan, there are few others but the annuity rates would more or less be the same, still a comparative exercise of different companies would help.

Since annuity is taxable, so what investors need to keep in mind is that not to invest so much in NPS or pension policies ( at accumulation stage), which leads you to shifting of major of your retirement corpus into immediate annuity products and make your Post-retirement income 100% taxable.

Have a proper Retirement plan at place and save in those instruments which are expected to generate tax-free instruments or are flexible enough to use the way your profile requires.

How do you find the review of HDFC life immediate annuity plan? Share your queries and comments in the section below

{kind=link}

What is recent structure of HDFC life new immediate annuity plan ? What about service tax ?

In Hdfc immediate annuity plan with return of purchase price in critical illness- if the illness does not occur before the age of 85 and the person is alive by that time and the death occurs at the age of 89, then the 100% purchase price is returned to the nominee or not ? Please reply