2020 has been an eventful year in all areas. When most parts of the world are working from home and getting accustomed to the new normal, the Financial Market Regulators are also on their job and doing their level best to make products, advisory, and structures easy, safe, and manageable for the investors.

The market events like Defaults and Downgrades of Debt Securities, Shutting down of 6 Franklin Debt Schemes on the grounds of liquidity concerns, and some internal issues in the product structures have made the regulator think again and propose some structural changes and measures trying to improve transparency and making investors more informed.

SEBI has issued a number of circulars announcing these changes, coming into effect in the year 2021. This Post is about,

5 important Changes related to Mutual funds applicable from Jan / Apr 2021:

1. Dividend Plans of Mutual Funds would be renamed as- Income Distribution cum capital withdrawal Plan:

From 1st April 2021, all existing and to be launched Dividend plans of Mutual Fund schemes would be called- Income Distribution cum capital withdrawal plans.

The dividend payout option would be renamed as- Payout of Income Distribution cum capital withdrawal plan.

Similarly, Dividend Reinvestment & Dividend Transfer plans would be called- Reinvestment of Income Distribution cum capital withdrawal plan & Transfer of Income Distribution cum capital withdrawal plan, respectively.

SEBI came out with this labeling norm to communicate to the investor that the dividend distributed by mutual funds is not only a distribution of profits but some portion of capital too, i.e. you get your own money back as a dividend and it is taxable in your hands as well.

Also read: Taxation of Mutual Funds 2020

Let us take an example to understand it better:

Let’s assume XYZ Dividend Plan launched at a NAV of Rs.10 on 1st Jan 2019. On 1st July 2020, you decide to invest in the scheme, the NAV on that date was Rs.13 and on 1st October, the NAV appreciates to Rs.15.

On this date, the fund books the profits and declares a dividend of Rs.5 per unit and the NAV again settles at Rs. 10.

For you, out of the Dividend of Rs.5 is only Rs. 2 (since the investment is made at the NAV of Rs. 13) is profit and the rest Rs. 3 is nothing but your own capital. But you have to pay tax on the entire dividend of Rs. 5 as per the slab rates applicable.

Also read: New or Old Tax Slabs- What to choose?

Now, the circular clearly states that Mutual Fund Houses should disclose this segregation between the capital part and the profit part of the dividends distributed in the Consolidated Account Statement provided to the investors. You may go through the circular here.

This amendment would help reduce the mis-selling of dividend plans. But, it is also important for the existing investors to review the option and see whether they want to continue with the same or switch the growth scheme and go for a Systematic withdrawal Plan (SWP) for regular income requirements.

Also read: How SWP in mutual fund works?

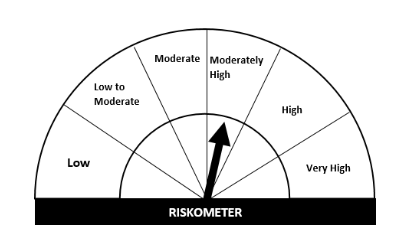

2. Revamping Mutual Fund Risk-o-Meter:

You must have come across the Risk-o-meter on the fund prospectus/factsheet, which depicts the risk level of the fund and consists of 5 parameters mentioned below:

- Low Risk

- Low to Moderate Risk

- Moderate Risk

- Moderately High Risk

- High Risk

One new category would be added to this existing arrangement- “Very High Risk”, from 1st Jan 2021. However, fund houses can adopt it earlier if ready.

So, now we would have 6 categories of Risk Levels. The new Risk-o-meter would look like this:

The Risk-o-Meter we see today actually shows the risk level of the category in which the Fund falls into and not that of the fund and is static for every fund.

The new risk-o-meter would be based on the portfolio of the fund and would have to be updated every month on the basis of the changes in the portfolio composition in the previous month and would have to be disclosed on the AMC as well as AMFI website within 10 days, making it a dynamic tool.

Any change in the Risk Levels of the fund would also be communicated to you (the investor) through e-mail or SMS. In addition, the year-end risk reading and how many times it changed during the year should also be disclosed.

SEBI has provided detailed guidelines to evaluate the risk levels of the fund in this circular.

Debt schemes would be evaluated on the parameters of Credit Risk, Interest Rate Risk, and Liquidity Risk. Debt Funds with higher exposure to illiquid, lower-rated and high maturity papers would be labelled as ‘riskier’, which means that debt funds could also fall in High and Very High-risk categories.

Also read: Types of Risks in Investments and how to manage them

Equity schemes would also be evaluated on the basis of liquidity measures, market capitalization (large-cap, mid-cap, and small-cap), and fund volatility. Equity Funds with higher exposure to the mid and small-cap sectors would be treated as riskier.

Also read: What is Equity, it is more than just stock market investment

The Risk Levels of ETF, overseas securities, derivatives, REITs, gold and cash is also determined. Read more on REITs here.

Also read: How good is Gold as an Investment?

This new arrangement would make more informed on the risk perspective of especially debt funds which are considered comparatively safer and would also help understand that risk and returns go hand in hand. Higher returns come with higher risk as well.

Also read: How to manage debt fund risks in an Investment Portfolio?

3. Inter-scheme transfer rules are now tightened:

Inter-scheme transfer (IST) refers to the shifting of debt securities from one scheme to another of the same fund house. As per present rules, such transfers are allowed if done at market price and is in conformity with the investment objective of the transferee scheme.

In order to prevent misuse of these provisions by the fund managers, SEBI in this circular has issued some additional guidelines for inter-scheme transfers. It would come into effect on 1st Jan 2021.

These new guidelines say that inter-scheme transfers in close-ended funds would be allowed only within 3 working days post the launch of the scheme and thereafter it is not permitted.

In the case of open-ended schemes, such transfers can be done to manage the liquidity requirement and meet unexpected redemptions. But this measure should be the last resort to the fund managers after all sorts of other Liquidity Risk Management have been exhausted.

The circular clarifies that the fund manager should first use the cash and cash equivalents of the scheme, thereafter market borrowing and selling of securities would be the option. If all these avenues fall short then the transfer of securities can be used to meet liquidity requirements.

However, the decision to use market borrowing before ISTs would be at the discretion of the fund manager.

In addition, the new rules also say that the fund manager would have to provide the rationale to the trustees behind the IST, if the rating of the paper gets downgraded within 4 months of the transfer.

If the security becomes default grade within 1 year of such transfer (in Credit Risk Schemes) then the trustees of the fund should ensure that the negative impact on the performance of the fund would reflect in the performance incentives of the fund management team involved in the process.

Also read: Types of debt funds

Also, no IST of security would be allowed if there is a rumor or negative news in the mainstream media or any alert is generated about it in the internal credit risk assessment, during the previous 4 months.

It would help curb the malpractices done by the fund houses to show good performances of some schemes by transferring some illiquid and lower-rated papers to the schemes which are not that mainstream.

4. Changes in Asset Allocation of Multi-cap Funds:

But, recently SEBI observed that portfolios of a lot of multi-cap funds are skewed towards large-cap stocks with almost 70 to 80% allocation and negligible allocation towards small-cap companies.

So, in order to make multi-cap funds ‘true to their label’ SEBI issued this circular and said that multi-cap funds should have at least 75% allocation towards equity and related instruments with 25% allocation to each large, mid, and small-cap stocks.

Also read: What is the difference between multi-cap and Flexi-cap funds

In further clarification, SEBI in this press release said that apart from rebalancing the multi-cap schemes, fund houses have other options as well. For instance, merge their multi-cap scheme with their large-cap scheme or convert them to Large and Mid-cap schemes, etc. Fund Houses have to ensure these compliances before 1st Jan 2021.

Also read: 5 ways to compare mutual funds

The press release also mentions that multi-cap funds should be benchmarked appropriately but does not clarify which benchmark to be used. Presently, no benchmark has a 50% allocation towards mid and small-cap schemes.

Also read: How Mutual Fund Benchmarks can help you select the Right Funds?

5. NAV allotment of the Day of Realization of Funds:

SEBI in this circular said that the closing day NAV of the day on which the fund would be available for utilization shall be applicable irrespective of the amount of purchase and time of receipt of the application, in case of all funds except liquid and overnight funds.

Previously, this realization day NAV provision is applicable only on the purchase amount of Rs. 2 lakhs or more.

So this new change which is also applicable w.e.f. Jan 1’2021 may impact your SIP Purchases and platform transactions, where there are chances of delay in the debit of your account and Credit to AMC.

Also read: Everything you wanted to know about SIP

Conclusion:

All these are interesting moves, and the whole idea for these changes is to make Mutual funds more investor-friendly. More comprehensible product to the Investors. Especially to the direct Investors.

For those people who have engaged Advisors or Distributors with them, SEBI is tightening the way the professionals are being operated in the market.

As I wrote at the beginning of this article that 2020 has been an eventful year. Not only for Financial products but even Financial Intermediaries are asked to change their way of working.

This article is written By Mr. Varun Baid

{kind=link}

Excellent and useful article, thanks for circulating.

Glad to know, Mr. Seetharama. Please share it with your family and friends.

Is dividend income upto 1 lakh p a per individual/ HUF is exempted

No, Mr. Swamy Dividend received is fully taxable.