In Budget 2020 FM announced a proposal of a new Income tax rates regime where a salaried person not having income from Business or Profession, can opt for and calculate the income tax liability in a simpler way without going much into the technical calculations.

This was with a caveat that if opted, then the employee would have to forego all the exemptions and Deductions which he/she otherwise could opt in (now) old income tax regime.

Since salaried people are asked to declare their savings structure at the beginning of the financial year so the employer can start deducting the TDS from the same, and the employee is also asked which tax regime he/she wants to opt for.

But in Union Budget 2023, government has cleared its intention to popularize the new tax regime and introduced few changes in it. Also, have made this new slabs as a default slab rates for the calculation of tax for salaried employees with effect from 01.04.2023. This means if someone does not specifically tell employer to opt for the old regime, the tds will be deducted on the calculation based on the new tax regime with the new rates only.

Salaried taxpayers , have time till 30th April 24 to decide , if they want to opt out of the default new tax regime, and go with Old tax regime instead. If not done on time, the TDS will be deducted as per the new regime tax slabs.

This article is to apprise you with the changes and the difference between the new and old regime. plus a calculation based on assumed numbers to make you understand how the Maths actually work

Old Tax Regime – Income Tax Rates (FY 2024-25)

| Taxable Income (Rs.) | Slabs |

| Up to Rs 2.50 lakh | NIL |

| 2.50 lakh – 5.00 lakh | 5% |

| 5.00 lakh -10.00 lakh | 20% |

| Above 10 lakh | 30% |

*If Income is up to Rs 5 lakh only then section 87A Rebate can be claimed. **Basic tax exemption Slab for Senior Citizen (Above 60 years) is up to Rs 3 lakh; and for Super Senior citizens (Above 80 years) is up to Rs 5 lakh

New Tax Regime (FY 2024-25 )

In the Union Budget 2023, FM has Introduced The New Tax Regime

| New Tax Slabs (in Rs.) | Rate of Tax |

| 0-3 lakh | NIL |

| 3 lakh – 6 lakh | 5% |

| 6 lakh -9 lakh | 10% |

| 9 lakh -12 lakh | 15% |

| 12 lakh -15 lakh | 20% |

| 15 lakh and Above | 30% |

The surcharge rates for old regime is left untouched and thus Taxpayers with income between Rs 50 lakh and Rs 1 crore will continue to pay 10% surcharge on the tax. The surcharge is 15% for income between Rs 1 crore and Rs 2 crore, 25% for between Rs 2 crore and Rs 5 crore, and 37% for income over Rs 5 crore.

However, to make the new regime attractive for higher income brackets, government proposed to reduce the surcharge from 37% to 25% above 5 crore of income if assesee opt for new tax regime. Applicable w.e.f FY 23-24

Also, for Income bracket not exceeding Rs 7 lakh, Rebate of 100% of Income tax payable is proposed u/s 87A, if opted for new tax regime. Where as in the old Regime the limit is up to Rs 5 lakh of Income. (This makes a point, if your income is upto Rs 7.5 lakh, then new tax regime should be your only choice)

Please note that besides the difference in Tax Slabs and Income Tax rates, the Major point of selection between the Old income tax rates regime and the New Income Tax rates regime is that in the new Regime you won’t be able to enjoy the tax exemptions and deductions, which may be available to you or you generally claim earlier.

What are the Major Income Tax deductions which one can not claim in the New tax regime?

- House Rent Allowance

- Standard Deduction (This benefit will also be available in the new regime calculation)

- Benefits u/s 80C – 80U – Like ELSS, PPF, NPS, Insurance, etc.

- Housing Loan Interest payment benefit u/s 24B

- Interest Income u/s 80TTA and 80TTB (For Senior citizens) benefit.

- Education Loan Interest u/s 80E

Looks like a Big List of benefits to forego…Right?

But the point here to note is that tax payers generally never claim all the benefits.

Some are living in their own house with no home loan. Everyone does not have an Education loan liability. All may not like to save u/s 80CCD or may not want to save this year to keep the liquidity intact

Which option should you choose will depend on the composition of your salary, your loan profile, your savings potential, etc.? So, one has to do comparative analysis and if the old slab rates look more beneficial, then BETTER TO go with thAT.

Also read: Read a detailed post on Income Tax Deductions

Let me share an example here for better understanding

Mr. X and Mr. Y both have the same salary structure, Mr. X claims various exemptions and deductions like- HRA, 80C, 80D, etc. so files tax under old regime

But Mr. Y, do not claim any deduction or exemption, and decide to file return under new regime

Let us first look at the Net Taxable Income in both the regimes for both Mr.X and Mr.Y: (please note , this calculation is referring to the new changes applicable from FY 2024-25)

Now let us see the tax liability in both the cases.

| Particulars | Mr. X | Mr. Y |

| Basic Salary | 18,00,000 | 18,00,000 |

| HRA | 3,00,000 | 3,00,000 |

| Medical Allowance | 50,000 | 50,000 |

| Conveyance Allowance | 50,000 | 50,000 |

| Gross Salary Income | 22,00,000 | 22,00,000 |

| Less : Exemptions | ||

| HRA ( assumed) | 2,00,000 | – |

| Gross Taxable Salary | 20,00,000 | 22,00,000 |

| Less : Deductions | ||

| Standard Deduction | 50,000 | 50,000 |

| 80 C | 1,50,000 | – |

| 80 D | 40,000 | – |

| Net Taxable Salary | 17,60,000 | 21,50,000 |

Let us calculate the Tax of Mr. X as per the Old Tax Regime and Tax of Mr. Y as per the New Tax Regime.

| Old Tax Regime Slab (in Rs.) | New Tax Regime Slab (in Rs.) |

Old Tax Rates | New Tax Rates | Tax calculation of Mr. X | Tax Calculation of Mr. Y |

| 0 – 2.5 lakh | 0- 3 lakh | NIL | NIL | NIL | NIL |

| 2.5 lakh – 5 lakh | 3 lakh- 6 lakh | 5% | 5% | 12500 | 15000 |

| 5 lakh-10 lakh | 6 lakh-9 lakh | 20% | 10% | 100000 | 30000 |

| 10 lakh and Above | 9 lakh-12 lakh | 30% | 15% | 228000 | 45000 |

| 12 lakh- 15 lakh | 20% | 60000 | |||

| 15 lakh and Above | 30% | 195000 | |||

| Gross Tax | 340500 | 345000 | |||

| Add: Cess 4% | 13620 | 13800 | |||

| Net Tax | 354120 | 358800 | |||

It is very much clear from the above calculation that in this specific case where one person has done some tax savings investments, will pay less tax if opts for Old regime. But, if you look closely then there is not much of a difference and to save Rs 4 thousand of additional tax , Mr. X has done 2 lakh of savings (God knows where :))

What Should you do?

In the New income tax Regime, it is easy, as you just have to have an Idea on total Income, without any deductions and benefits, and you can easily calculate the tax.

However, in the Old regime, you need to apply all the available and applicable provisions and see what would be your total taxable income.(You may learn about the major deductions and exemptions available to an individual in this article). Here I have added one Income tax deductions list infographic too for an easy read.

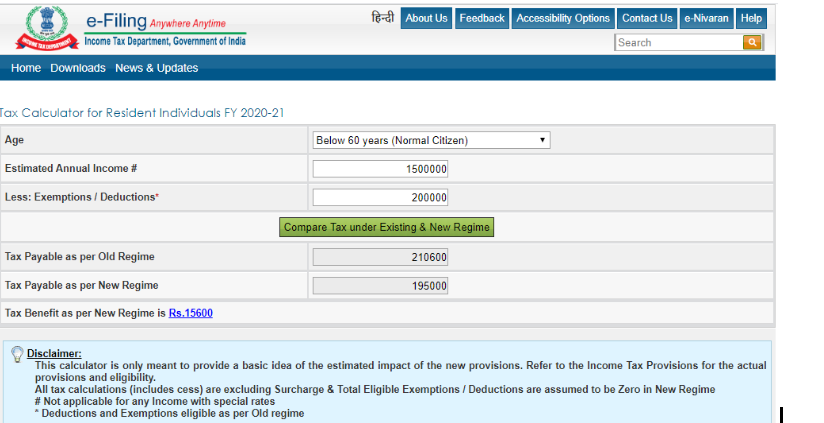

There’s a calculator available on the Income Tax website where you can make the comparison between Old and New tax regimes and decide which option may suit you best.

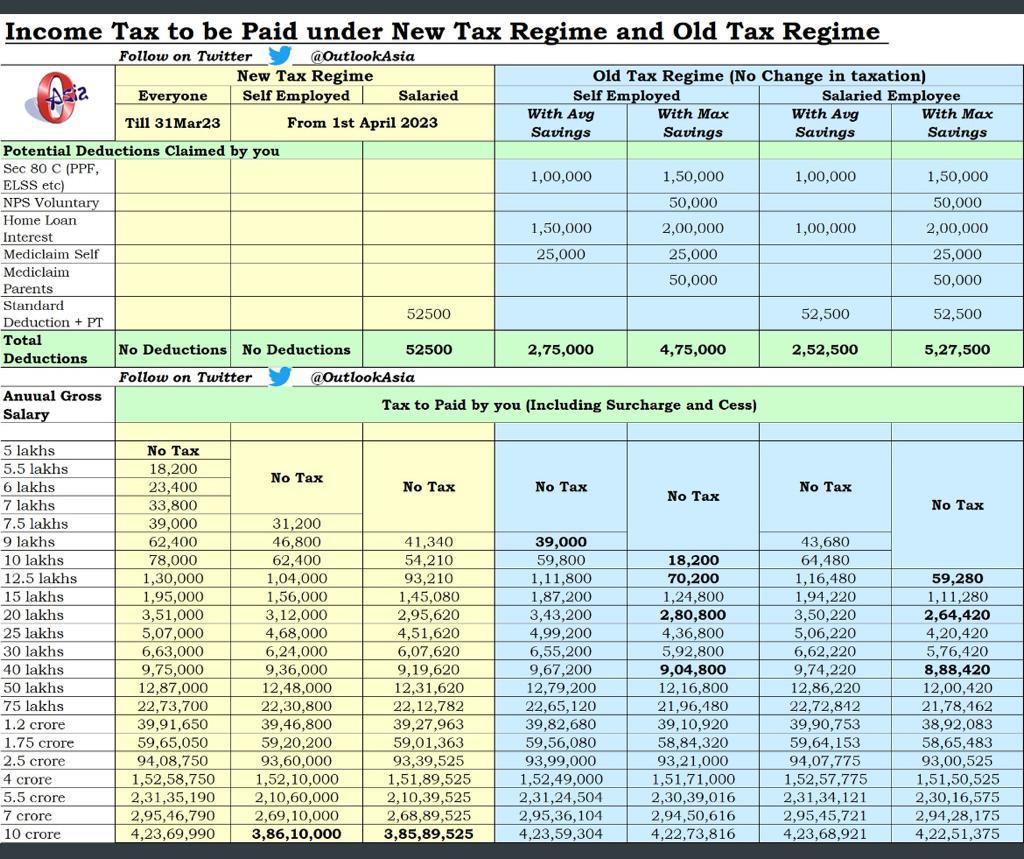

Also, a useful chart prepared by Outlook Asia, which shows the tax calculations under different income brackets in different tax regimes. Please find below

One Important thing. Even if at a later stage i.e after declaring to your employer about your choice of tax regime, you feel that the other one could have been better, then do not worry. When you file your Income-tax return next year i.e. in Assessment Year, you may do the self-assessment again with the other regime of your choice. In case of Salaried tax payers, one can opt for different regime from the one they chose at the start of the financial year. Salaried employees have the option of switching between the two tax regimes each year, giving them the flexibility to avoid aggressive tax saving investments while being able to opt for the old regime if they take out a home loan or see increased rent costs in the future.

However , those with business income can move between two tax regimes only once in their liftime.

Also read: Benefits of Filing Income Tax Return on time?

Conclusion:

The thought behind coming up with this new Income tax rates regime is to make things simple for the taxpayers so they need not to take any professional help. But I think that now in many cases professional help has become more important to do the exact tax calculation (especially till the time government keep the old regime as optional), so one should be able to take the benefit of all available and possible tax benefits, and chose what’s better.

But if someone wants to keep things simple, then, of course, the new one is suitable.

How do you find the old and new income tax rates in comparison? Do share your views and queries if any in the comments section.

Also check: Which ITR form you should use to file your Income-tax return?

{kind=link}

Dear Sir,

Very nicely explained all the tax implications under the old and new tax regime.

I want to understand whether deductions u/s 80-G (towards donations to qualified trusts) which is available under the old tax regime, would it be available for deductions under the new tax regime.

Thanks, Kamal Ji. I hope you are doing well and staying safe. In the new tax regime, 80G deduction will also not be counted. However, if someone donates to PM Cares before June 30’2020, then one can claim benefit in FY 19-20 Income Tax Return. This is explained well in this Business Line Article, https://www.thehindubusinessline.com/news/section-80g-deduction-an-added-incentive-to-donate-to-the-pm-cares-fund/article31233321.ece

Hai Mani, I am Suresh from Bangalore. My total Salary is 8.5L (Sal+Pension). I have HBL, Edn loan, NPS, additional PF, medical exp for dependents and lastly for PM care fund also. Which one will be a better option either old or new scheme

Hello Suresh Ji. Let’s connect on email or Phone.

if my gross salary is 505000/- and net will be 450000 around which scheme is beneficial … new or old ?

There is no one-word answer to this. A comparative analysis of both the tax regimes is required to be done based on your salary composition, savings potential, loan profile, etc. Then we need to decide which tax regime would be beneficial.

If one has no salary also can one opt for new regime?

Hi RP,

Yes, non-salaried individuals can also opt for the new income tax regime. However, unlike salaried individuals, they do not have the freedom to switch between old and new tax regimes every financial year. Once they have opted for the new regime, they would have to continue paying taxes as per the new regime in all the subsequent financial years as well.

Read this: https://economictimes.indiatimes.com/wealth/tax/these-individuals-cant-switch-between-old-and-new-income-tax-regimes-every-year/articleshow/74110899.cms?from=mdr