Comparing mutual funds can be tricky, there are as many as 44 Fund Houses offering more than 2500 mutual fund schemes in India!

But still, most of the investors rely only on two factors to compare mutual funds which are the past returns and star Rating by some research houses, which actually is not the right approach.

Though Past performance should be considered, there are different ways to look at it. Besides returns, there are several other qualitative and quantitative parameters that are equally important.

So, in this post, I will discuss 5 tools to compare mutual funds in detail. But before using these tools, make sure that you are comparing funds falling in the same category and use the right benchmark so that the comparison exercise makes more sense.

Also read: What is SIP in mutual funds?

Since returns is the primary way of looking at the mutual fund performance, let’s talk about that first:

1.Compare Mutual Funds on the Basis of Returns:

As far as returns are concerned, there are three ways to evaluate and compare the returns of a mutual fund.

a. Absolute or Point to Point Returns:

It measures the increase or decrease in the NAV of the fund, without taking into account the time period of investment. It is just the difference of the final value and the initial value in percentage terms.

For example, you invested in 100 units of fund X at the NAV of Rs 10 and sold them after five years at NAV Rs 20. This means, in absolute terms, you have earned 100 percent returns [(20-10)/10]*100.

Why is it not a good tool to compare mutual funds?

Well, the reason is simple. It does not factor in the time of investment and the compounding effect. It might be possible that similar returns in absolute terms may be generated by two funds, but Fund A took 3 years and Fund B took 5 years for the same.

Absolute returns show that both the funds are equally good performers, but clearly, Fund B took a longer tenure to deliver similar returns. The better metric would be CAGR.

b. CAGR (Compounded Annual Growth Rate):

It shows past returns of a specific period, say 3 years, 5 years 10 years, etc. Simply put, it is point to point returns in annualized terms.

On the face of it, this tool looks fair enough, but it has limitations too:

It measures returns taking into account only the starting value and the end value of the fund, assuming that it has consistently compounded over the time period. It ignores the consistency and volatility of the fund across different market conditions.

Volatility is the basic nature of equity markets and recent bull or bear runs in the market may influence this metric and present a manipulative picture of the fund performance.

Also read: What is Equity?

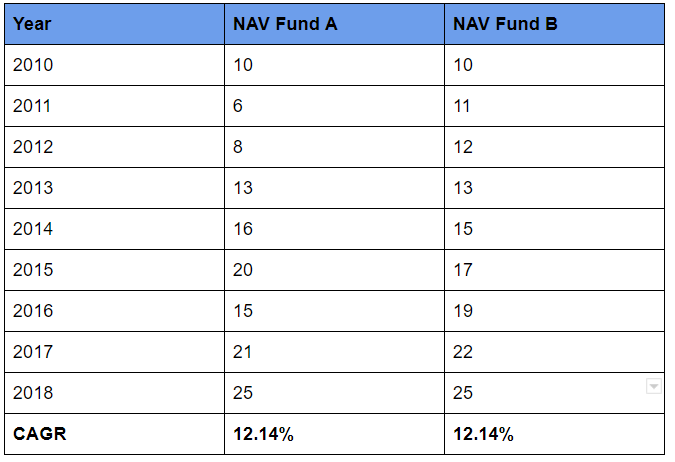

It may happen that a bullish phase in the market for 1 year may show good trailing returns over a three or five year period or vice versa. Let us take a hypothetical example:

In the above example, though both Fund A and Fund B have the same CAGR, it is clearly evident that Fund B has shown a more consistent performance than Fund A.

That way, though it is better than the absolute return metric, but will not show the consistency of the fund to help you compare mutual funds in an effective manner.

c. Rolling Returns:

Basically, these are trailing returns over different time periods. While calculating returns, not only one block but multiple blocks of 3,5 or 10 years, at different intervals, are taken into consideration, that way behaviour of the fund across different market ups and downs can be analyzed.

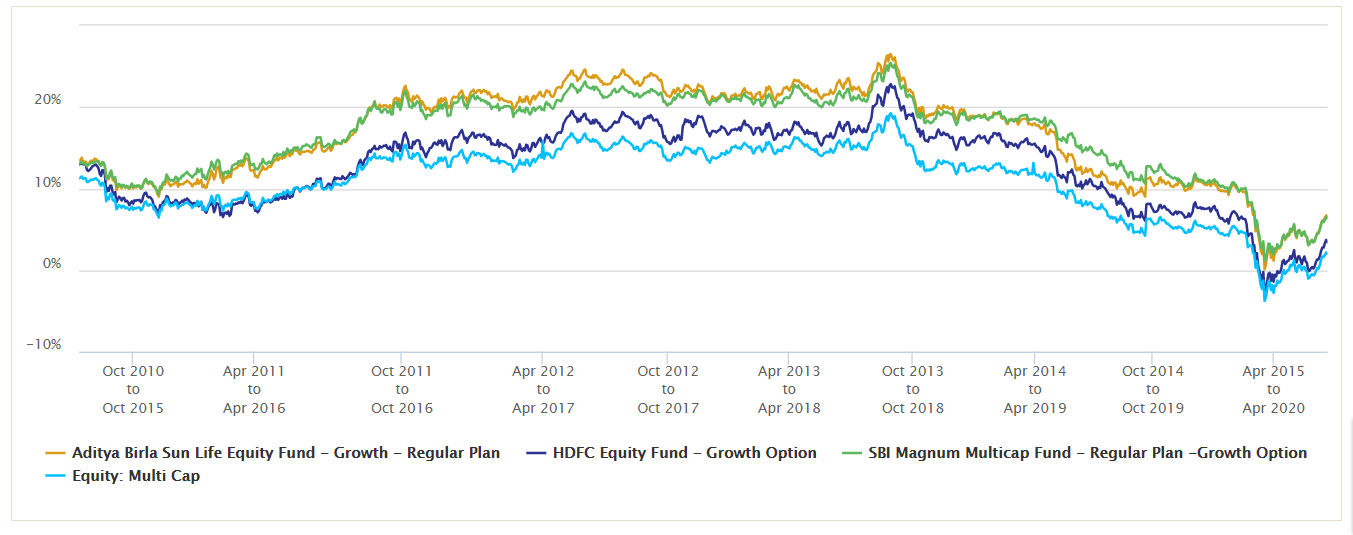

For instance, you want to compare the performance of two funds (belonging to the same category) over different five year periods, over the last 10 years (2010-2020).

You may check 5-year returns starting from each day falling in the period from 2010 to 2020 i.e. 5 yr returns starting from 1st Jan2010 till 1st Jan2015, 2nd Jan 2010 till 2nd Jan2015, 3rd Jan 2010 till 3rd Jan2015, and so on…., the average of these figures would give a better sense of the performance of both the funds.

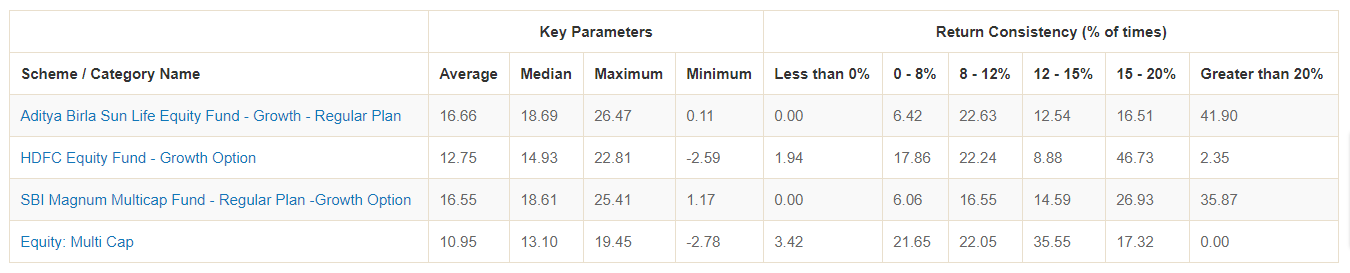

This exercise can also be repeated to compare the performance of the fund vis-a-vis its benchmark. See the image below:

2. Mutual funds comparison on the basis of risk involved (risk-adjusted return):

As stated above, comparing funds merely on the basis of returns is not enough, you should also look at the risk factor. It is equally important.

You might be aware that investments in mutual funds involve risk, and rationality says that you get compensated for the degree of risk you have taken, in terms of returns.

Also read: Types of Risks in investments and how to manage risk

Let’s say, you are comparing two funds and found that these funds have delivered similar returns over a particular period, how are you supposed to judge, which one is better?

Here comes the role of risk-adjusted returns. For ascertaining risk, the basic metric used is Standard Deviation, wherein we see how much the fund returns have deviated from the average returns. Higher standard deviation means higher volatility that way higher risk and vice versa. The beta of the funds will tell you the risk vis a vis the Benchmark.

Also read: How Mutual Fund Benchmarks helps you select the right funds?

So, if the standard deviation of Fund A is 10% and that of Fund B is 15%, it implies that the risk involved in Fund B is higher than Fund A, but the returns generated are almost the same, so Fund A has performed better than Fund B.

However, the standard deviation is a very basic approach to measuring risk. The more concrete way to arrive at risk-adjusted returns would be to use various ratios such as – Sharpe Ratio, Treynor’s Ratio, Sortino Ratio.

sounds alien, don’t worry, you may get these ratios already calculated on the Fund Factsheets or Research websites. The higher these ratios, the better is the fund.

Also read: How to interpret an equity mutual fund fact sheet?

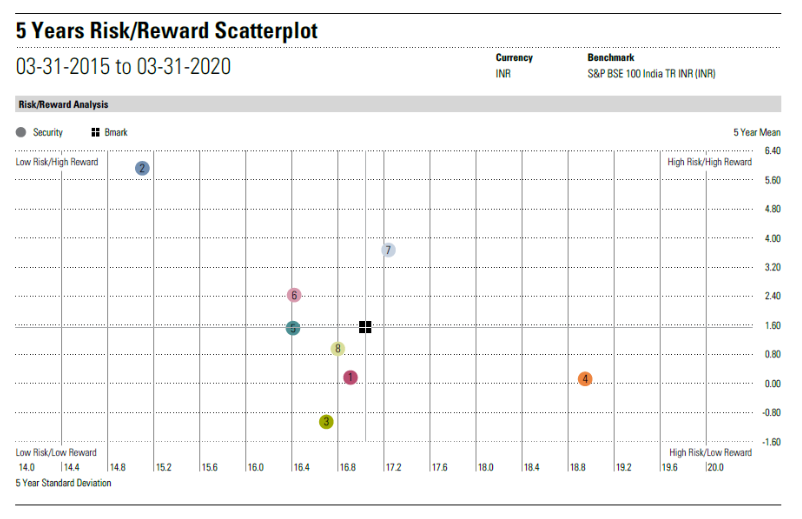

The above Scatter Chart shows the Largecap funds, mapped in different risk and Return Quadrants. Which do you think would be a better one?

3. Compare mutual funds on the basis of Expense Ratio :

Once you are satisfied with the performance of the fund, you may use the expense ratio of the funds as a tool of comparison. (Read more about expense ratio here). Select the fund with a lower expense ratio to fetch good returns.

But while comparing the funds on the basis of expense ratios, apart from category and type of fund, keep in mind the points mentioned below as well:

- Make sure you are comparing the expense ratio of Direct Plan of one fund, with that of the other. And Regular to Regular.

- Expense Ratios are different for index funds and actively managed funds. Index Funds have a lower expense ratio than actively managed funds, due to the difference in structure. Compare TER of Index fund with another Index Fund and actively managed fund with another actively managed fund.

4. Mutual Fund Comparison on the basis of Fund Manager track record and pedigree of Fund House:

While comparing mutual funds, it is also important to see the fund manager has a decent track record and holds good experience in the fund management space, to make sure that your hard-earned money is in safe hands. Other funds which the fund manager is managing can also be looked upon.

Fund investment asset size also matters. I will not say the bigger the better, but it should be decent.

Also when comparing funds it is always wise to go with the fund house which is a reputed one and has a decent existence history.

5. Selection on the basis of Portfolio of the funds:

Now when you have compared the funds and have shortlisted some, the time has come to select among them and build up a portfolio.

Also read: 5 ways to review investment portfolio

You should better not select the 2 funds of the same asset class with the same fund house. Fund manager diversification is very important. Most of the time you will see many funds of the same fund house in the performing list. Having all in your portfolio may not make sense, as the same style and strategy do not last for long.

Also read: Always add some debt mutual funds too, to have a well-allocated portfolio.

Invest in sector/thematic funds only when you are confident in the same and do not add more than 5% of the total investments in the same.

Also read: All you wanted to know about ESG investing theme

Also read: Have International allocation to diversify the currency Risk.

Conclusion:

Comparing mutual funds and selecting decent funds is the right thing to do but first, you should know the reason for your investment. It is not earning high returns, but the achievement of goals. Right?

Do remember, Returns are mere numbers they keep on changing!

So, it is important to know your financial goals and prepare a financial plan first and then select the funds according to the same which would help you in deciding the suitable exit strategy too.

Also, you may not be an expert in all fields, like you have a Chartered Accountant to take care of your accounting and taxation aspects, there is no harm in asking for the help of a Financial Planner to guide you with your investments.

Hope you find this post useful. Should you have any questions, feel free to put it in the comments section, we would try to answer your query as soon as we can. If you like the article, do share it with your family and friends.

This post is written by Mr. Varun Baid.

{kind=link}