Inflation and taxes are two holes in the

Investments pocket. While making investment, the ultimate goal is to have a

positive return post inflation and taxes.

Your goals are getting impacted by inflation,

your expenses rise due to inflation, your purchasing power gets squeezed

because of rising inflation.

In fact, High inflation sometimes means Higher interest rates, as RBI wants to control the rising prices, High interest rate leads to higher cost of capital and thus impacts the profitability of the corporate.

Also read: Tools RBI use to control inflation

It’s just a small example, there are so many

interlinkages in different macro-economic indicators. So, Important is that you

should know how and where the particular indicator is going to impact you.

In Financial planning, Inflation is the very

important consideration. But its not a single general number which is taken

into account.

Retirement, education, medical, lifestyle all leads to different assumptions on inflation.

What is inflation?

It refers to rise in the general price of goods and services. Be it food, clothing, housing transport etc. all gets impacted by inflation. It measures the average price change in a basket of commodities and services over time, resulting in an increase in the cost of living.

I will not go into technical of how and why part of

Inflation. Its just for the general understanding, so you can make wiser

financial decisions.

High Inflation directly Impacts the Purchasing Power of

currency i.e. With the same amount of money you buy lesser goods at a later

stage.

So, it’s not just an economic term but impacts each and

every section of the personal finance in one way or the other. So, it becomes

important to account for the same, while planning for the long-term financial

goals.

In India, Broadly inflation is primarily measured by two indices, namely Wholesale Price Inflation (WPI) and Consumer Price Inflation (CPI).

WPI reflects the changes in the average prices of goods at the wholesale level, i.e. commodities sold in bulk and traded between businesses or entities.

On the other hand, CPI tracks the change in retail prices of goods and services, which households purchase for their daily consumption, making it more relevant in financial planning.

CPI is also used to calculate Cost Inflation Index, which factors in the impact of inflation on the cost price of capital assets.

How different types of Inflation impacts the financial plan?

FOOD INFLATION: It is the general increase in the

prices of food and associated items, which is the major component of any

household consumption and impacts each and every individual. So, it becomes

very important to be taken into account while planning anyone’s finances.

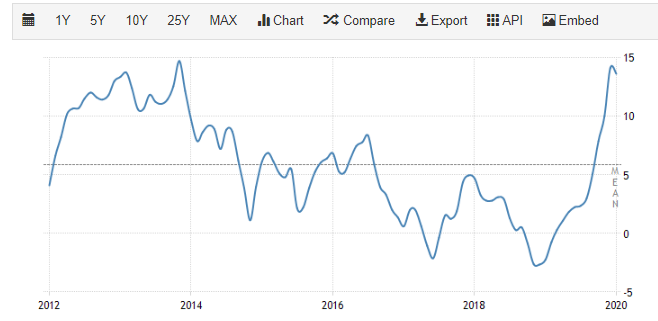

As per tradingeconomics.com Food Inflation rate in India averaged 5.84 percent from 2012 until 2020, reaching an all-time high of 14.72 percent in November of 2013 and a record low of -2.65 percent in December of 2018.

HOUSING INFLATION: Buying a house is one of the important financial goals for many. Housing property prices get impacted by many factors like demand, supply, tax benefits, economic stability, etc. It usually differs with the general price environment in the country, so needs to be looked upon and to be planned for differently.

Also read: Are You ready for your next house purchase?

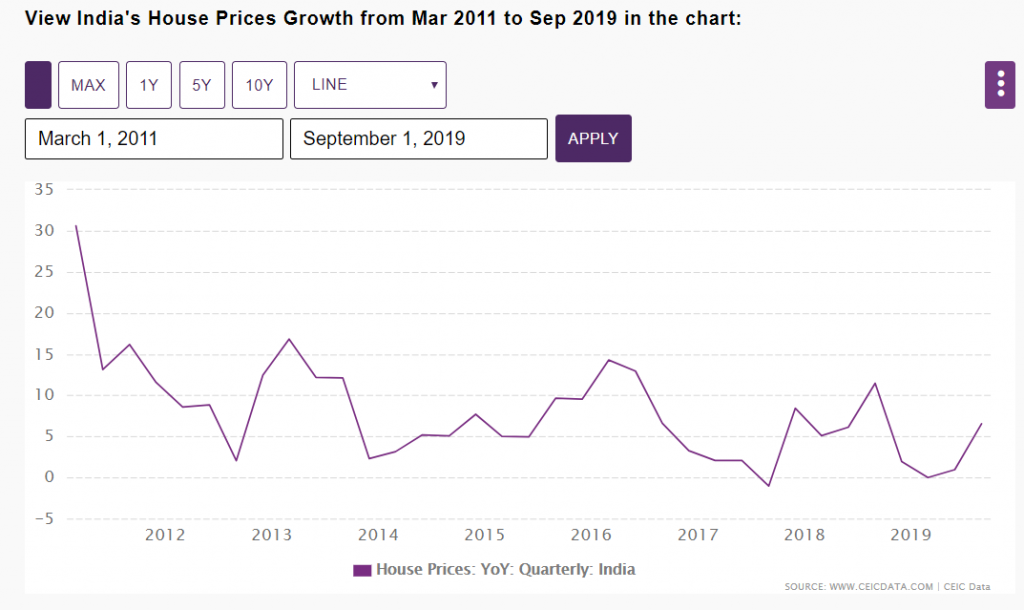

As per ceicdata.com, from March 2011 to September 2019, India House Prices have grown on an average rate of 6.6% p.a., reaching an all-time high of 30.6% in March 2011 and a record low of-1% in September 2017.

EDUCATION INFLATION: They say, Planning for Child Education is not a child’s play. Education cost is rising very fast and when you have a goal for international education, you have to take into account the currency fluctuations too. Considering the trends of the fee structure of private educational institutions in India, it is estimated to be increasing at 10%-12% per year. You can easily have a feel of it considering the Children school/college expenses

MEDICAL INFLATION: With the rapid rise in technology, and the advancement of medical facilities, medical inflation is also rising each day. It impacts each one of us and may hit badly during Post Retirement years. So, it is wise to be prepared for the same by taking adequate health insurance as well as maintaining a decent medical emergency fund.

Medical inflation does not only include the cost of hospitalization, but medicine costs too, doctor consultation fees, Surgical equipment etc.

A report by Mercer Marsh Benefits forecast medical trend rate to be around 10 percent in India.

LIFESTYLE INFLATION: This inflation implies those

expenses which are discretionary in nature and beyond the basic expenditure, these

are additional big-ticket expenditures incurred for improving the standard of

living, such as- bigger house, branded clothes, better car, latest gadgets,

lavish vacation etc. It becomes important to provide for the same especially

while planning for the long-term financial goals to keep up with the current

lifestyle.

Conclusion:

Inflation is a kind of slow poison. You have to understand its impacts and plan to tackle it, before it damages your financial situation. You cannot beat medical and education inflation with Fixed deposit kind of product, so It is important to target the right inflation with the right instrument, and strategy.

Also read: Investment strategies for Education and Retirement

{kind=link}