In the series of reviewing health insurance policies offered by nationalized banks, the next one is Canara bank Mediclaim. I have already reviewed PNB oriental Royal Mediclaim and AB Arogyadan which you can read from here.

The Canara policy is a private policy in a public package. Yes, the insurer in case of Canara bank Mediclaim is the private health insurer, Apollo Munich health insurance. Apollo is offering an almost similar policy to its retail customers, but the one offered through group insurance to Canara bank account holders is at very competitive rates.

Today, I will review Canara Apollo Munich health insurance policy in detail, and also do a comparative analysis to what is available otherwise to its retail clients.

Canara bank Mediclaim – In Brief

Canara bank in collaboration with private health insurer Apollo Munich health insurance is offering the Easy health group insurance plan to its customers (Account holders). The only precondition before buying this product is that you should be having a bank account at Canara bank.

The USP of this policy is that the premium is quite competitive as compared to its similar product as available in the market for Apollo’s customers, with almost same or better features.

Besides this, the premium is flat for all age groups, unlike the retail policy where the premium rate varies for different age group.

You may also buy this policy for your parents or Parents-in-laws too, and their account is not a prerequisite in this case if you are an account holder. (Also Read: Mediclaim policy for parents – other options)

I am always wary of the service quality of nationalized health insurers, and this was one of my big concerns when I reviewed PNB Oriental Royal Mediclaim, but since here in Canara bank Mediclaim the insurer is Apollo Munich which is a private health insurer, so this becomes another attraction in this policy.

(Also Read: Do you have financial plan to survive a serious illness?)

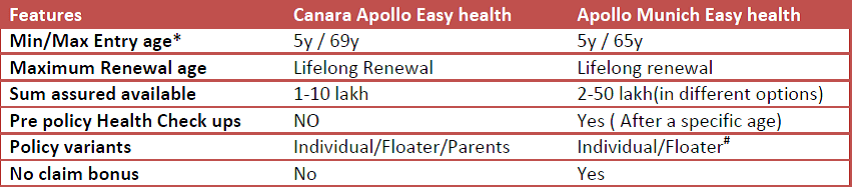

Canara bank Mediclaim – Basic features

(in comparison to Apollo Munich Easy health Insurance)

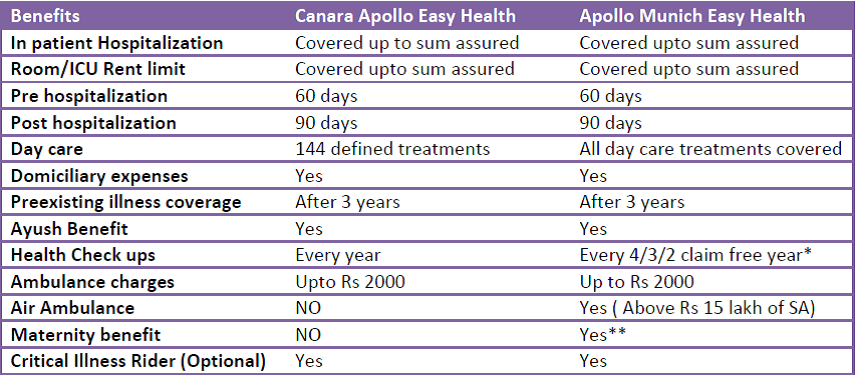

Canara bank Mediclaim – Key Policy benefits

(in comparison to Apollo Munich Easy Health Insurance)

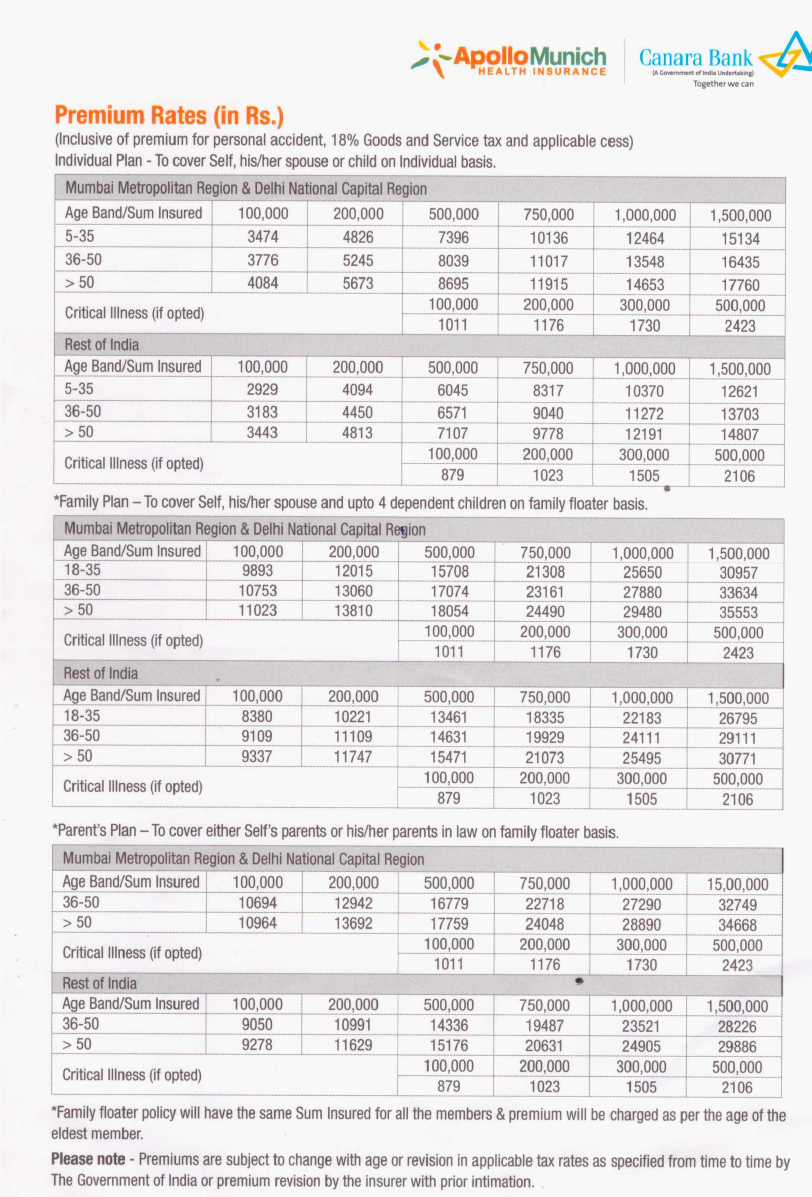

Canara bank Mediclaim – Premium rates

All the above-mentioned rates are flat rates and not linked to any age slabs. Whereas if you buy directly from Insurer than rates are quite high. For e.g. for a 50-year-old healthy individual, wanting to buy sum assured of Rs 10 lakh, have to shell Rs 8692/- to Canara Apollo Munich health insurance, and Rs 19039/- for standard variant to directly Apollo Munich health Insurance. (Click here to check out Apollo Munich Easy health’s rate card)

Canara bank Mediclaim – Should you buy?

Well, I have not found anything negative in Canara Apollo Munich Mediclaim policy. Though it doesn’t have high-end features of Air ambulance or additional feature of maternity benefit which the retail version offers, but as far as basic Mediclaim policy is concerned, which covers In house treatment, day care surgeries, Pre and Post hospitalization etc. and that too with no cappings, sub-limits or copayments, all are available here.

The Maximum Sum assured available is also quite decent, and one can buy Super top up policy separately to enhance the cover if required. (Read: Apollo Munich super top up review)

But as I wrote earlier in my last review, in group policies offered by nationalized banks, do not expect any services from bank people as they are just acting as an intermediary. If you buy this policy, then you have to equip yourself with knowledge of the necessary processes for smooth issuance of policy and claim settlement. Also, do not take flat rates as really flat ones, since it all depends on the claim experience of the insurer and also the relation between bank and Insurer. Even group policy rates can change in future.

Personal financial Planning always starts from having adequate emergency fund and required insurances. Health Insurance is one of the Major components in protection planning. Chose wisely to have a comfortable future.

How do you find Canara Apollo Munich health insurance policy? Do share your views

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Nice summary of the insurance policy.

Really have a very good one insurance policy from apollo munich general insurance company ltd. The policy covers maximum expenditure and the claims are easy to get due to fast service provided by the executives. Renewals are easy and updates are mailed regularly to my email address.

Can i convert my existing personal policy from apollo munich to this group policy with continuation benefit?? I m 60 years are premiums are rising exponentially with age. Also if i take this policy can i convert to individual policy of apollo??

You cannot Port in your existing policy into this canara apollo plan. You have to buy it afresh, which means that all the waiting periods will start from scratch. So better to avoid this.

Hello Mr Singal

Thanks for such a good review on Canara Apollo Munich group Policy…. Can I port this group policy from Canara Bank to an individual family floater one in the future.

Also can you please share your viewpoints regarding Bank of India National Swasthya Bima policy.

Yes you can port this group policy to individual at the time of yearly renewal and within the time specified for portability…i guess it is 45 days before renewal. And i have already done a review of BOI policy. Pls find the link http://www.goodmoneying.com/insurance-planning/boi-national-swasthya-bima-policy-review

Canara bank also offers a similar policy in tie up with united india, if am not mistaken ? I was thinking of taking that. Could any one please tell me which is better?

I need to check on this. Not sure.

which is better among canara+apollo mediclaim or canara +united india mediclaim for entire family including patents ( uper age is 68 years) .what shoud be policy rules for patient with chronic higher

tension (blood pressure ) ?

I have not gone through Canara United yet. But, i believe one should have a decent cover first. We tend to waste the crucial time while searching for better. There should not be much of difference in the policy basic features. So whichever policy you are comfortable with…get yourself a cover first.

Do spend a good time in research. Because taking health insurance is like marriage.

Better take ur time before getting trapped in a wrong one.

Good Luck.

Can I port my pnb oriental group policy to Canara Apollo policy and get all benefits of carry forward of waiting periods for all diseases. I now have diabetes.

No. Group policy cannot be ported to other group policy

I would like to avail this insurance. Kindly get back to me at the earliest.

If you want to know how to get the insurance he is the process:

1. Go to any canara bank branch and get an account opened.

2. Ask branch manager / manager-in-operations for the “Apollo Munich GUY” who does the health insurance

3. Get your insurance done after following his instructions.

Dont forget to thank me if it have helped you 😉

Thanks Arnav 🙂

Dose the individual plan cover for spouse of the account holder?

Yes. But then only the spouse will be covered. If you want a floater and joint policy, then you have to go with Family Plan

My dad is 58 years old and got himself covered under Apollo Munich Easy Health policy for Canara Bank customers. He has also paid the renewal premium this year. My Question is Upto which age he can be holder of the insurance policy. At the starting of the article it was written maximum entry age 65y and Renewal will be lifelong ! Is that so ? Can you go through the terms and conditions of the policy and let me know

1. if my dad will be covered life long by this policy ??

2. the premium will not increase on the basis of age at any point of time ? ( it may increase due to inflation or other factor I am asking abt age as its a huge bonus ) . Please confirm this too

Yes, the Insured will be covered lifelong, and Premiums will not increase with age.

This is as per my understanding, to get more details and confirmation its better you should write to Apollo Munich Customer care or visit any nearest Branch.

Hi Sir,

Very nice details about the policy. I have one question. What if tomorrow this tie will break between the Bank & health care company? How it will affect the existing customers? How our policy will go forward?

Thanks,

sanjay

Then you will be offered with similar kind of policy out of available policies with the insurer and next year you can port your policy to the insurer of your choice.

Hello,

Thank you for the reply. If I am getting it right, this means if we take example of Canara Bank & Apollo Munich; and in case their tie up gets over then we will be offered with similar kind of policy from Apollo Munich and the next year if want we can port it to other than Apollo Munich. I hope my understanding is right. Then in that case the Pre-Existing Diseases period will not get extended right?

Second question is about the premium, as we see premium is quite competitive as compared to its open market rates. So in above case the premium will get modified to open market rates?

Yes, to both the questions.

Sir i like this policy, i have an existing policy family floater policy from Oriental Health insurance which covers me age of 34,parents age 56,57. What is your opinion on swithching the policy?, i seen in this tieup there is no policy which can cover all 3 of us so i will take 2 policies. 1) for my parents Floater policy 2)for me standalone.

My questions:-

1)it better to transfer from PSU to private ?

2) I don’t have an account with canara bank right now but if i open tomorrow can i buy this policy?

3)Can i transfer my policy from Oriental to This one with continue benefits specially for that years waiting period?

4)My policy renewal un current co is 27 th Jan can i transfer with in one month?.

Waiting for your reply

More or less, all policies are similar in nature now-a-days. So, switching is beneficial only when there are significant differences in features.

Yes, you have to open an account with Canara Bank to buy this policy. However, these are group policies and are valid only till the tie up exists.

These policies are non transferable, if you buy this policy, you have to start everything from scratch and may not continue the benefits under the previous policy.

Is there life long renewal in this policy?

Renewal is always lifelong as per court ruling. Provided the policy should be in existence always.

Sir but dependent children are covered only till 5 years. After that what should we do go with individual policy for kid ? Age of my kid is 18 months

I think you can cover your child in floater policy till he becomes Major. Please get in touch with Apollo/Canara Executives for clarification.

Hi Sir,

I am planning to purchase health plan for my parents whose age is 49(mom) and 59(Dad).

Pls suggest me whichpolicy is good for my parents(1. BOB(Baroda Health -National ), 2. BOI(National Swastya) 3.Canara (Apollo Munich Easy Health)).

Pre existing diseases –

Dad – BP and for Mom – Thyroid and Mental disorder(Not admitted in hospital only tablets and she is well and fit).

Could you please suggest me which policy is good of you choice.

And, I noticed the policy wordings in Apollo munich wordings were as below(http://www.canarabank.com/media/2553/brochure-10l-web-draft1.pdf)

MAJOR EXCLUSIONS • Any treatment within first 30 days of cover except any accidental injury.

• Any Pre-existing diseases/conditions will be covered after a waiting period of 3 years if the

risk is accepted.

• 1 year exclusion for specific diseases like cataract, hernia, hysterectomy, joint replacement etc.

• Expenses arising from HIV or AIDS and related diseases.

• Congenital diseases, MENTAL DISORDER, cosmetic surgery or weight control treatments.

(For complete exclusions please refer to the policy document)

Here, stating last point wether the insurance company will reject the claim that your mom has mental disorder. Please please clarify and sugget me.

Thanks in advance.

See, all policies are good. You just have to see, which company accepts your case and gives cover to your parents. You have to disclose the health conditions of your parents while filling the proposal form. Just be true to them and let them decide.

The exclusions and waiting periods you mention is a kind of standard across the industry.

contact me 9878854555 for health insurance at very low rate …

Hello

Can you please provide feedback for apollo Munich policy being sold by Dena bank at a very low premium rate.

I am basically looking for health policy for my parents. Both 62+. Father with hypertension and diabetes. Mother with hypertension and keen pain.

Also, how are the star health policies although copays are very high.

HI. I have not seen the Dena-Apollo policy. Will review it someday. Thanks

I’ve got two questions –

1. Should i not select a public (nationalized) insurance provider over a private insurance provider? I think private companies are profit driven and this could impact the claim settlement. While in public sector insurance company, they’ve got a sum allocated by government that needs to be spent for claim settlement and profit making won’t be the primary goal.

2. Can a partially paralytic person (enjoying sound health otherwise) get an insurance cover under these bank mediclaim policies?

Kindly suggest. Thanks.

1. I don’t think so. Not sure but even if they are profit driven, IRDA rules are same for them too.

2. This might be considered as Pre-existing illness and covering the person totally is Insurers’ prerogative and depend on their underwriting process.

thank you for the detailed article. i surprised to find nothing about this insurance on its site canarabank.in . kindly guide me if it is available anywhere, if i err.

sorry. it is available on bank’s site.http://www.canarabank.com/english/bank-services/personal-banking/insurance-business/health-insurance/

Hello Sir, My mother has taken this Canara bank Apollo Munich insurance policy a year back (sum insured 5 Lakhs). My mother was 67 and Father was above 70 yrs of age at that time. Do this policy cover my father’s insurance requirements ? Kindly reply.

How is this policy compared to apollo munich Optima restore? I am planning to take this for my parents aged 60 and 57

Optima restore has majorly 2 different feature, Restore option and High NCB. Rest it is same as easy health

hai for any clarification make a call to me 99999999

Hi, i recently purchased Apollo Munich health Insurance policy from Canara Bank for my husband, I would like to understand iwhether it will cover my husband preexisting heart disease..

My questions are

policy is valid or not?

Whether it will cover other disease?

heart will be covered after 3 years of policy purchase r not

You have to disclose the Existing health ailments in the proposal form and let the insurance company take the call to cover it and when.

Hello Sir,

Can you please elaborate me what is the savings I can get if I go to Canara Apollo Munich through Canara Bank and directly go to Apolo Munich. I am looking for 03 people for 3 lack sum assured. I am 39 year old and wife 31 year old and daughter 07 year old. Kindly let me know how much I can save on premium and other benifits

Thanks

Dinkar

Please contact Canara or Apollo Employees for all these comparisons

With in next 10 days renewal premium has to be debited from my account for certificate numbers EA 00281275, 76,77 & 78, but till date your customer care is not in a position to tell the exact amount that will be debited. Please give a call back.

dear sir,

i am glad to inform you to in that i have already check up and amt. is debited my bank account but i don’t know any status for my policy so please give me status for my policy thanking you

Does this policy cover :

1. Depression

2. Parkinsons

Awaiting response.

Thank you.

Not sure. You should better read out the policy exclusion list, if these were not mentioned there then you may have to leave the decision with Underwriters after applying for the policy

Sir , my parents are above 75 , can we take parents plan from canera bank …is there any age limit for parents

I have a joint saving account in Canada bank,am I eligible to canara bank mediclaim,SB acc. With my daughter,if I can what is the procedure?

Hello Mr. Singal,

I have read the policy document, it say that you need to sign on a declaration that you dont have the following illness. The declaration is not clear and waiting period for specific illness is not mentioned like you see in all other policy where its clearly mentioned that the below mentioned illness will be covered after so many years.

I also saw the policy document and it seems this polict has lot of exclusions like in point 10. it says in CABG open heart surgery exclusions will be Angioplasty etc.

Kindly help me clear my doubts.

Please share the policy document by highlighting your concerned areas on [email protected]

My Apollo Munich Mediclaim lapsed on August 8th. Is there any chance of renewing? I did this policy through Canara bank.

I don’t think so. Generally health policies have 1 month of Grace period, but you have passed that time frame also. Still, you may check with Apollo people.

I am 69 years complete and running 70 years …my wife is 66 complete..whether I can purchase policy for 5 lacs…covering my spouse or alternatively,whether my spouse can purchase the policy and include me in the sum assured

Since the maximum entry age is 69 years, so I believe getting the policy should not be a problem. please contact the bankers

My brother wants to purchase this policy from Canara bank as he is the account holder in the bank. He has got diabetes (Type 1). My questions are –

1. Will this policy cover complication occurred due to diabetes after 3 years of waiting period?

2. Policy mentions Hospital Daily Cash. Can you explain that?

3. Where can I see the Critical Illness which are covered under this (if opted)?

Rahul, to be more confident on your intended purchase i would advise you to consult directly with Apollo Munich people. They will answer all your queries.

My brother (26 years) wants to purchase this policy from Canara bank as he is the account holder in the bank. He has got diabetes (Type 1). My questions are –

1. Will this policy cover complication occurred due to diabetes after 3 years of waiting period?

2. Policy mentions Hospital Daily Cash. Can you explain that?

3. Where can I see the Critical Illness which are covered under this (if opted)?

If the tieup of Apollo and Canara bank breaks what will the options available with us. Is the bank provide any other company tie up option for us? Because going for direct Apollo premium will be too costly as I am looking for my parent.

If the tie-up breaks then Apollo will give you the option to get into any of there existing plans by offering you continuity of the benefits. But in that case, since you will be going directly with Apollo so the cost would definitely be a factor to consider

I am 60 and my wife is 55 . could you sugguest a medical/health insuarence plan for us

All private companies will cover you in their open Plan. or may consider these group plans which may have some maximum age limit restrictions.

My parents were with New India policy enrolled when it was getting offered from Bank of Baroda as a tieup. Now after 8 years, BoB has broken the tieup. Earlier the premium for 5 lac was 7000 which now New India is asking 24000. Should we continue with New India or should we get this Canara bank policy? I think I am more concerned about continuity of benefits. With canara bank, we will have to start all the way from ground zero but if we stay with New India, they are offering continuity of benefits.

Please suggest

Yes. You get it right. To enjoy the continuity benefits you have to continue with new India. However, once you move to the individual policy then after 1 year you may again port the policy to the company of your choice and this will not impact the continuity benefits.

SIR,I purchased a canara apollohealth insurance policy for 5 lacs on 18.10.2016 and have continued the yearly reneals in last three byears and payment of fourth isntalment is due in early october 2019-have completed 36 months.Myself and wife have diabetic .But it appears I have not understood things correctly and not mentioned having diabetes for self and spouse in 2016.May I request you,what are the steps I have to take now so that deiabets and hypertension are covered.Very sorry for the inconvinience.PRASAD V S V

If you would disclose now that you are diabetic, to the insurer it would be treated as a misrepresentation of facts and the insurer has the full right to cancel the policy. What you may do is, you may apply for a new policy from another company, disclosing all the facts. If the diabetes is not much older, company may agree to issue the policy.

But since, Apollo Munich has a separate policy for diabetics, it may be reluctant to issue the regular one. You may consult a trusted Health Insurance Adviser for further guidance on the issue.

Sir, my age is 53 running and looking for a health insurance for 5 Lacs, I have visited SBI for the SBI arogya plus having 3 Lacs limit but premium remains unchanged for life long.. and to meet 5 Lacs remaining 2 Lacs can I take Canara bank health insurance of which premiums are also competitive.. are this both cash less and how are they…kindly guide

Yes, both are cashless if the company has tie-up with the hospital. But Combining a group policy with individual policy does not make any sense to me. You cannot depend on a group policy for long (especially when the concern is Premium). My advise would be to get yourself insured from a single company.

Sir, is there any provision for domicilery coverage in this polycy?

apolo munich mediclaim policy

room rent quary

We understand that you are inquiring about room rent sub-limits, it doesn’t have any room rent sub-limit.

मेरा पालिसी 6महीने से जयादा दिन हो गया है पॉलिसी नही मिला

In Apollo mediclaim tie with Canera Bank what is benefit

My age 66 year, but what is the benefit to take Insurance with canera bank in Apollo mediclaim

Read the policy features and decide whether the policy is beneficial or not.

I Renewed of Group health insurance policy for 2019-20 for that I required Hard copy of policy

I Renewed of Group health insurance policy for 2019-20 for that I required Hard copy of policy but i have not received policy copy

how latest is this post? dont see date in it? is rates still as of today ?

This post is a bit old. Please check the latest policy features from the company website.

are you from Apollo Munich health insurance

whether family floater Synd Arogya health insuranc

No, we are not associated with any insurer. We are independent financial planners/ Bloggers. Please contact the insurer directly with your queries.

Canara Bank health insurance

Premium for my mother age 70

We are not associated with the Insurer/Banker by any means, please visit the website of the insurer/banker or visit the nearest bank branch with your queries.

Iam the existing customer of canara bank i want to take health insurance which bank maintained companies

Additional Query: Please i need concerned person to talk about this

We are not associated with any insurer/banker. We are independent financial planners/ Bloggers.

Please contact the insurer/Banker directly with your queries.

I AM CANARA BANK A/C HOLDER, WANT TO TAKE MEDICLAIM POLICY FOR MY PARENTS

We are not associated with any insurer/banker. We are independent financial planners/ Bloggers.

Please contact the insurer/Banker directly with your queries.

Is the insurance applicable to someone aged 71yrs ?

As far as the information we have, the maximum age to enter the policy is 69 years. Still please check with the banker/ insurer directly with your queries.

I have a medical health policy in syndicate bank with the name syndaroghya. Since syndicate bank is merged with canara bank, I have renew this policy at the end of this month.

Kindly help me in this regard

Some nationalised banks cheating the customer regarding health insurance policy, After some time banks breaking the tie up with health insurance company and closing policies. Customers suffering bank and insurance companies benefitting.So this issue should be highlighted and and approach consumer court or concerned higher authority .

I have a syndarogya policy which is due for renewal. Now that syndicate bank has merged with canara bank I would like to know the procedure for renewing the policy in canara bank Mediclaim.

Some of nationalised banks cheating the customer regarding health insurance policy, After some time banks breaking the tie up with health insurance company and closing policies. Customers suffering bank and insurance companies benefitting.So this issue should be highlighted and and approach consumer court or concerned higher authority

Can canara bank Apolo Munich Health insurance scheme available for family cover of parents. Whether it covers all the ailements like heart’, cancer etc or only some excluded

As far as the information we have, you may add parents in a single cover and all critical ailments are covered. But do confirm from the Banker or Insurer before taking any action.

How can I renew my health insurance

As far as the information we have the policy has been discontinued and it should be ported to some other insurance policy. Do check with the Bank for details.

i have canara bank apollo munich policy.Can you pls advice whether it is having restore benefit

No, it does not have a restore benefit. But, do check with the bank. As far as the information we have this policy has been discontinued.