Samar, one of my school-time friends who works with a software firm in the UK, called me during the lockdown days to discuss his financials. Though we usually have general chit chat over Whatsapp, this was a focused discussion.

His queries were related to Indian taxation. He had some earnings from India in the form of rental, dividends, and fixed deposit Interest. Also, he keeps visiting India, for Personal and professional purposes, and in the last few years, the visits were quite frequent due to his father’s bad health.

He read somewhere that in Budget 2020, the Indian Government has changed the definition of Non-Resident Indians, and now if a person stays here for 120 days or more instead of 182 days earlier in a financial year would be called Resident.

He counted his period of stay and found that last year he was in India for 131 days, as his company allowed him to work from home due to Parents’ health.

So his question was if that situation repeats in future, would he be counted as Resident Indian, and if yes, what would be the tax implications? And What is RNOR? as he has never heard this term before.

This was a valid question and a genuine concern, as many NRIs were confused after this announcement, and plus RNOR status was something of an alien term for many.

Post Budget 2020, a lot many queries have been pouring in regarding the RNOR status of the NRIs. The Government announced some major changes in the definition of NRI, which led to the confusion in the minds of Visiting Indians and PIOs (Persons of Indian origins).

Generally, RNOR status is looked upon in the case of Returning NRIs, but with the addition of 2 more conditions in the definition of RNOR, it may get applied to some others too.

Also read: Taxation of NRE Fixed Deposits for Returning NRIs

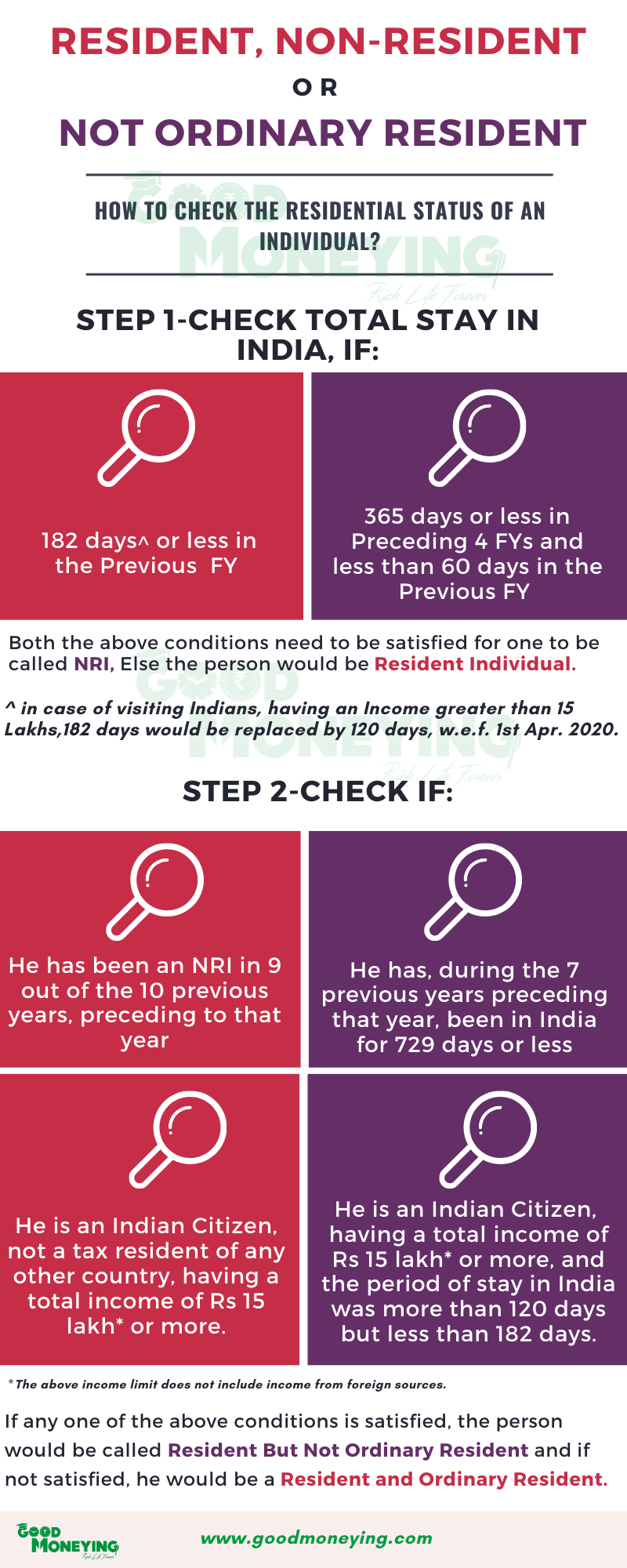

So, let’s first understand who actually an RNOR is?

Who is RNOR?

As per Income tax rules specially meant for Returning Indians, RNOR (Resident But Not Ordinarily Resident) is an Individual who:

- Has been an NRI in 9 out of the 10 previous years preceding to that year, OR

- Has, during the 7 previous years preceding that year, been in India for a period of, or periods amounting in all to 729 days or less.OR

- An Indian Citizen, who is not a tax resident of any other country, and having a total income of Rs 15 lakh and more (Excluding income from foreign sources) OR

- An Indian Citizen, or a PIO, having Income in India of Rs 15 lakh or more (Excluding Income from foreign sources), and the period of stay in India was 120 days and more but less than 182 days.

The conditions 3rd and 4th have been added in Finance Bill 2020, which was the cause of all this confusion. “Income from foreign sources” means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India).

The below infographics summarizes the conditions to check for Resident, Non-Resident, and RNOR residential status:

Since Samar does not have that much income from India, the change in the period of stay is not applicable to him.

One of the above 4 conditions needs to be satisfied to be eligible to be construed as RNOR.

You must have noted that the first condition is of your Residency tax status, the other is on your stay in India, the third one is about your total income and its source plus tax residency in another country, and the last one is the mix of Income and period of stay.

Why is RNOR status Important to check?

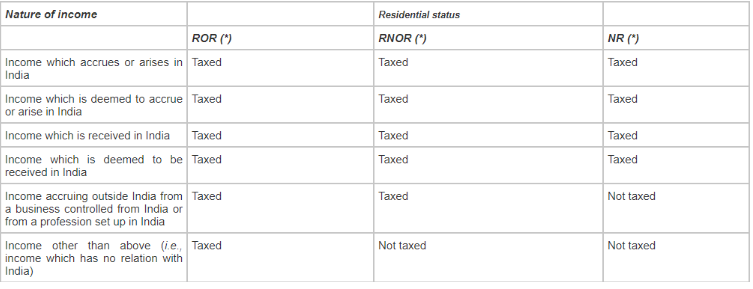

The Residential Status is an important factor to determine the taxability of the Income of the concerned person. The taxation of an individual depends on the A) Residential Status and B) The nature of the Income.

Also read: Mutual funds taxation – How is it different for NRIs?

Income tax rules say, if a Person is a Resident, then the Indian Income, as well as Foreign Income, be taxed in his/her hands; whereas if the Person is Non-Resident, then Only the Indian Income be taxed and not the foreign income.

RNOR status is treated the same as Non-Resident. Thus in the case of RNOR too only Indian income is taxable and not the foreign Income.

Though this time Government has added conditions on the visiting NRIs or PIOs, generally RNOR status is the point of contention among the Returning Indians.

The purpose of RNOR residential status is to provide a safe tax net to the returning NRIs so they can wind up their financial arrangement from the other country and bring back the assets along with less worry on the taxation part.

So, if someone is an RNOR and is still earning rental income on properties abroad, or earning some kind of interest on their deposits, or capital gain on their shares or mutual funds invested abroad, then that will not be taxable in India, till the time they are RNOR

Considering the First 2 conditions of RNOR status, and assuming someone are not having Total Income of Rs 15 lakh in India, then the undermentioned may apply:

- Those returning India after being NRIs for 5 continuous years or less, immediately become Residents as they won’t be able to satisfy the first 2 conditions.

- Those returning India after being NRIs for 6 continuous years may become RNOR for one year, provided he/she had not visited India in all those years

- Even those who after being NRI for a considerable time say 15-20 years, may become RNOR but for 2 years at the most. In rare cases, a person can become RNOR for 3 years.

How to determine the taxation status of an Individual?

Firstly you have to find if you are a Resident or a Non-Resident. Check the rules for the same here

If the calculation says that you are not a Non-Resident, then you have to find out if you are a Resident or a Resident but not ordinarily resident (RNOR), by checking the rules as stated above in the article.

You have to do these calculations every year to be on the right side of the law, so to file your tax returns accordingly.

What is the benefit of having RNOR Status?

As mentioned above the major benefit of having RNOR status is that till the time you become completely Resident, you will not be taxed on your Foreign income.

Plus this is to ease out the procedures so you can bring your money back to your country smoothly with not much tax hassles. (Check your Residency status from this RNOR calculator – Click here)

So when you are RNOR and come back to your home country for good, you are allowed to open the RFC account (Resident Foreign currency) account where you may transfer your NRE bank balance and even FCNR account balances, in case you want to keep the tax free interest status, and also the easy repatriability of the funds. (Read: Everything about NRI bank accounts)

You may receive foreign remittance easily in your RFC account, like your Rentals, Capital gain proceeds, Employer benefits, Retirals, etc. and you will not be charged any tax on the same in India.

Also read: Tax Planning Tips for NRI Returning to India

The below table summarizes the taxation on different Residential status:

Conclusion:

Samar’s case was different, but still, his concern was genuine. If you have Income in India above the threshold limit, and you are a regular visitor then soon you will lose your NRI tag and may be asked to pay tax on your foreign income. Even if your visits are genuine and you are a law-abiding citizen you may fall into tax complexity due to all this.

However, for returning NRIs coming for good in their home country, RNOR status would help them manage their foreign transactions in a tax-efficient manner and will have ample time to wind up.

{kind=link}

As Indian passport holder, on 18 March 2019 I stayed for good in India. When can I become Indian Resident?

There is not a one-word solution to your query. A lot many things are there to look at, for instance, if you were an NRI in 9 out of the 10 previous years preceding to that year or not, you were in India for a period of 729 days in the past 7 years preceding that year or not, etc.

So, please use the calculator of Income Tax website and fill in the details to know your residency status:

https://www.incometaxindia.gov.in/Pages/tools/residential-status-calculator.aspx

As per calculations, I will be a Indian Resident exactly a year later as I am a RNOR. Can I invest in post office products though I am RNOR or wait till I become Resident?

Although you are an RNOR in the eyes of income tax. But, since you have returned to India for good in FEMA’s eyes you have already become a resident as the intention is clear.

Investments are governed by FEMA and not Income tax. So, just like you may be having a savings bank account in India, you may also go for the post office saving schemes before becoming tax resident in India.

I am an NRI both by IT & FEMA from FY 2009-10 till 2016-17. During FY 2017-18 RNOR by IT and NRI by FEMA.

During 2018-19 exactly stayed 182 days in India so i presume R by IT nd NRI by FEMA.

But during 2019-20 Resident by both IT and FEMA. I have NRE FDs which will start maturing from 2022 till 2026.

What is the best way forward.

Hi Chandra

What I don’t understand is how do you consider yourself as NRI by FEMA in 2017-18 and 18-19? If you have come back in India with an intention to stay here for good or for long then the moment you entered India you have become NRI as per FEMA. And once you are NRI by FEMA your NRE deposits become taxable unless you have converted that account to RFC.

In my view, all your NRE FDs have become taxable at this stage.

If I am NRI as per FEMA; however, RONR as per IT law (due to exceeding number of days stay). Would the interest on NRE remain tax free.

If i am in RNOR status during 2020 (India) 7+ yrs stay in foreign country and have some retirement income in other country for the sake of simplicity let us take USA then in 2020 i pay flat non resident tax -30% in USA on that retirement benefit claimed (401K) there and don’t pay any tax on that in India due to RNOR rules but my questions is i dont think there are option to claim for those foreign tax paid credits in RNOR status correct ?

Hi Manikaran,

I find your articles really helpful so thank you for that! I was wondering though do you have any more clarity on the number of years you can be RNOR consecutively or if you become RNOR the go back to ROR can you become RNOR again?

I was an NRI for more than 19 years, and since returned to India for good. I qualify as an RNOR. I have let out few properties on rent. What is the threshold rental amount and the % of TDS to be deducted. Is it 10% of 31.2%?

Since you have become a Resident / RNOR , the TDS threshold and rate applicable will be of Resident Indian. This article will explain you the details https://www.charteredclub.com/tds-rent/

Dear Mr. Singal,

I’m an OCI & planning to stay in India for about three years (has no intention to undertake employment or do any business) after everything settles with Covid. I have some investments through NRE FDs. Let’s say I’ll become a resident & after certain time I have to convert these NRE FDs into Savings accounts. My query is, whether I’m allowed to transfer these savings accounts FDs back into NRE Accounts once I become an NRI after leaving India, fulfilling the norms of an NRI. If so, can you please explain the procedure involved in doing these transfers from Savings account to NRE account. Thanks.

Dear Mr. Siraj,

When you return back to the country of residence, you need to again convert your Resident Savings account into an NRO account. From this account, you may transfer the money to the NRE account after submitting form 15CA/ CB, whatever is applicable.

Need advise on RNOR status FY 2020-21 and FY 2021-22

I returned back to India in Feb 2020 and below is my day count of stay in India during past 16/17 years.

2004-05 17 days

2005-06 22 days

2006-07 18 days

2007-08 35 days

2008-09 35 days

2009-10 78 days

2010-11 28 days

2011-12 143 days

2012-13 30 days

2013-14 67 days

2014-15 41 days

2015-16 110 days

2016-17 364 days (RNOR)

2017-18 186 days (RNOR)

2018-19 23 days

2019-20 50 days

2020-21 365 days ——————————- NEED TO KNOW RES. STATUS – RNOR?

2021-22 179 days (as on 26 09 21) ———– NEED TO KNOW RES. STATUS – RNOR?

Thanks in advance.

A. Singh

Hello Mr. Singh,

I am sharing the link for the residential status calculator on the Income Tax Website, I believe this would be the most authentic source for knowing your exact residential status. Just fill in the above details here.

https://www.incometaxindia.gov.in/Pages/tools/residential-status-calculator.aspx

Hope it helps.

Thanks.

Hello Mr.Singh,

I am working in Gulf Countries from last 9.4 Years Exactly. Here no Tax is applicable on me.

During 2020 I could not be able to Visit India due to Covid Pandamic.

This Year I was came in India on 13August’21 and Stayed in India up to 14 December’21 more than 120days. Last 10Yrs my stay in india not exceeding 700days.

So kindly guide me I have to Pay any Tax on my NRE FD or what?

If NRE FD interest not counting then my total earning in India is not going more than 2.5Lacs even.

So does I pay any Advance Tax or not?

Thanking you,

Hi Ravi,

It depends upon your residential status, if it is NRI, then there would be no tax applicable. Else it may be taxable. Since your income in India is below the minimum taxable limit, you need not pay any Advance Tax.

Regarding your article of RNOR status that he should be NRI for nine financial years out of ten etc etc

Whether this is taken from any IT LAW

if yes

Pls send me pdf of same law showing what you have written

Is RNOR salary from foreign sources is taxable or not? Please advise if I can file ITR-1 if my status is RNOR?

Thanks you.

Hello Mr. Rao,

As far as we know, as long as you hold the RNOR status your salary from the employment in foreign country would not be taxable in India. And RNORs have to file income tax returns using ITR Form-2. Please consult a good Chartered Accountant to confirm the same.

Hi

I have recently returned to India and my residential status for FY-22-23 would be RNOR

Can I keep my NRE account while I am RNOR?

or do I need to close my NRE account and associated FDs and convert them to resident saving/FD accounts?

Hi Mayank,

Since your residential status has become RNOR, the NRE deposits will not remain tax-free anymore. Now you have two options, either you need to convert them to RFC deposits and continue to earn tax-free interest until you remain RNOR. However, it might be possible that the bank might tell you to close the account rather than converting into RFC. Since the premature closure of the FDs might result in an interest loss. So, the better option is that to continue the NRE FDs until maturity and pay taxes on the interest received on the same by reporting it in the income tax return in the next FY. You may close the NRE savings account.

My dad is an NRI for more than 50 years. Wants to return slowly to India. Is there an article explaining when is the best time to move to India for tax year purposes and making the most out of the RNOR status for 2 years plus?If he stays less than 729 or 120 days in a year can he spread it over 3 years? Is bank interest in NRE FD counted as income?

For tax purposes, it is better to consult a tax expert. However, you said your father wants to return to India, there is no way to escape from taxability on NRE FD interest income. As once he becomes Resident (Even RNOR) The NRE Interest becomes taxable from the same day as per the FEMA rules .

What I understand from RNOR rules is that even if your foreign income is not taxable in India, it is still taxable in the other country where you might still be a tax resident. So, keeping things simple, I don’t think there is any advantage in working out 2 y or 3 years of RNOR. Better to plan how his savings saved abroad can be used for his wellness in future.

For the tax purposes, it is better to consult a tax expert. However, you said your father wants to return to India, there is no way to escape from taxability on NRE FD interest income. As once he becomes Resident (Even RNOR) The NRE Interest becomes taxable from the same day as per the FEMA rules .

What I understand from RNOR rules is that even if your foreign income is not taxable in India, it is still taxable in the other country where you might still be a tax resident. So, keeping things simple, I don’t think there is any advantage in working out 2 y or 3 years of RNOR. Better to plan how his savings saved abroad can be used for his wellness in future.

I was NRI for past 30 years and returned for good to India in Jaunary 2022. I still have NRE and FCNR deposits . I qualify for being RNOR. Please advise if I will have to pay income tax on the interest earned on NRE and FCNR deposits. Awaiting your reply.

Once you are Resident (even RNOR) the NRE deposits and even FCNR becomes taxable