When it comes to Retirement Planning, NPS has become one of the important products to consider along with PPF, EPF, Superannuation fund, Mutual funds, etc.

Also read: Why Retirement Planning should be your most important goal?

Read our detailed posts on:

This is due to various reasons like- low-cost structure, decent performance track-record, transparent mechanism, hassle-free operations, and of course, the additional tax-advantage.

Also read: NPS – National Pension Scheme

And nowadays you can also set up a SIP in NPS using the D-Remit facility.

Also read: How to set up SIP in NPS

But, one important question raised by many NPS investors is that- What happens to the corpus lying in the NPS account once the accumulation phase or the working life ends?

See, during the accumulation phase, the money in your NPS account is managed by the NPS trust. But, as soon as you reach superannuation or take voluntary exit, the NPS trust has no role to play post-that.

It only provides you with the lump-sum withdrawal and transfers the balance amount to the life insurance company (annuity service provider), as-opted by you for the regular pension or annuity.

Next query comes from investors is- How much will they receive as a pension?

And when you look at the various annuity options offered by the empanelled annuity service providers, confusion further increases as to which annuity plan would be suitable to choose.

In this article, we will discuss the NPS annuity plans and the pros and cons in detail. It will help you understand the suitability of each one of these.

But, to set the context of the article, let us first quickly understand the NPS withdrawal rules.

NPS Withdrawal Rules 2022- in brief:

At the time of retirement, you are allowed to withdraw upto 60% of the NPS corpus, lump-sum and the balance 40% or more needs to be transferred to a life insurance company to subscribe to an NPS annuity plan for the regular pension income.

If you are exiting NPS before retirement, at least 80% of the accumulated corpus needs to be mandatorily utilized for the purpose of subscribing to the NPS annuity plans and only the balance 20% is allowed as a lump-sum withdrawal.

However, if the balance in your NPS account does not exceed Rs.2.50 Lakhs (Before 60 years) or Rs.5 Lakhs (After 60), as the case may-be there is no need to buy any annuity plan, you can withdraw the entire amount lump-sum. You can go through the detailed article on NPS withdrawal rules here.

Now, let us understand the NPS annuity plans and try to answer questions like-

- Which annuity plan should you Choose?

- How much pension will you get?

What is annuity in NPS?

Annuity in NPS is nothing but the regular income you receive from the accumulated corpus in your NPS account.

You subscribe to an NPS annuity plan from a part of your accumulated NPS corpus (generally 40%) of an annuity service provider empanelled with the NPS trust (list shared in an upcoming section). This is for the regular income/pension for a fixed period, post-retirement.

It can be monthly, quarterly, or annually as desired by you. Although, the monthly-mode is the most preferred one. If you are a government employee, only a monthly annuity option is available.

However, if you have retired post 60 years or on superannuation, you may choose to defer the annuity payments upto 3-years.In case of pre-mature exit, this option is not available, you need to subscribe to the annuity plan immediately.

The amount of annuity (pension) varies depending upon the age of entry, purchase price, rate of annuity (depends on prevailing Interest rates) and the NPS annuity option chosen.

The amount of pension remains fixed for the lifetime and does not change with the changes in the interest rates of NPS annuity plans.

Empanelled Annuity Service Providers with NPS:

You can subscribe to NPS annuity plans only from the following 14 life insurance companies, empanelled under NPS as Annuity Service Providers (ASPs):

- Aditya Birla Sun Life Insurance Company

- SBI Life Insurance Company

- Life Insurance Corporation of India

- HDFC Standard Life Insurance Company

- ICICI Prudential Life Insurance Company

- Kotak Mahindra Life Insurance Company

- Bajaj Allianz Life Insurance Company

- Edelweiss Tokio Life Insurance Company

- Tata AIA Life Insurance Company

- Max Life Insurance Company

- Star Union Dai-ichi Life Insurance Company

- India First Life Insurance Company

- Canara HSBC Oriental Bank of Commerce Life Insurance Company

- PNB MetLife India Insurance Company

Options under NPS Annuity Plans:

Although there are various annuity plans available with the life insurance companies. But, for NPS subscribers, as per PFRDA guidelines the annuity service providers can offer mainly the following 5 types of NPS Annuity Plans:

- Annuity for Life: This is a plain-vanilla annuity plan. In this, a fixed amount is paid to the annuitant (NPS subscriber) every month/quarter/year as desired, throughout his life. Upon death, the annuity payment ceases and no further payments would be received.

- Joint Annuity for Life: In this annuity plan, the annuity payment continues even after the death of the NPS subscriber. The same amount of pension is payable to his spouse as long as she is alive, after the death of the annuitant.

- NPS- Family Income Plan with Return of Purchase Price: This is the default annuity option for NPS subscribers. In this NPS annuity plan, a fixed pension is payable to the NPS subscriber every month/quarter/year, as desired. Upon death, the same amount would be paid to his spouse throughout her lifetime. After her death, the pension would be paid to the subscriber’s dependent mother and thereafter, his father. On death of the last dependent, the purchase price would be refunded to the nominee or the legal heirs (children) of the subscriber.

- Annuity for Life with Return of Purchase Price on death: In this annuity option, a fixed amount is payable as pension and upon the death of the subscriber, the purchase price (investment amount) would be refunded to the nominee.

- Joint Annuity for Life with Return of Purchase Price on death: In this option, annuity payment will continue throughout the life of the spouse of the annuitant and after that, the purchase price would be refunded to the nominee.

Also read: Bajaj Allianz Life Guaranteed Pension Goal Review

How much pension do you get? NPS Annuity Calculator

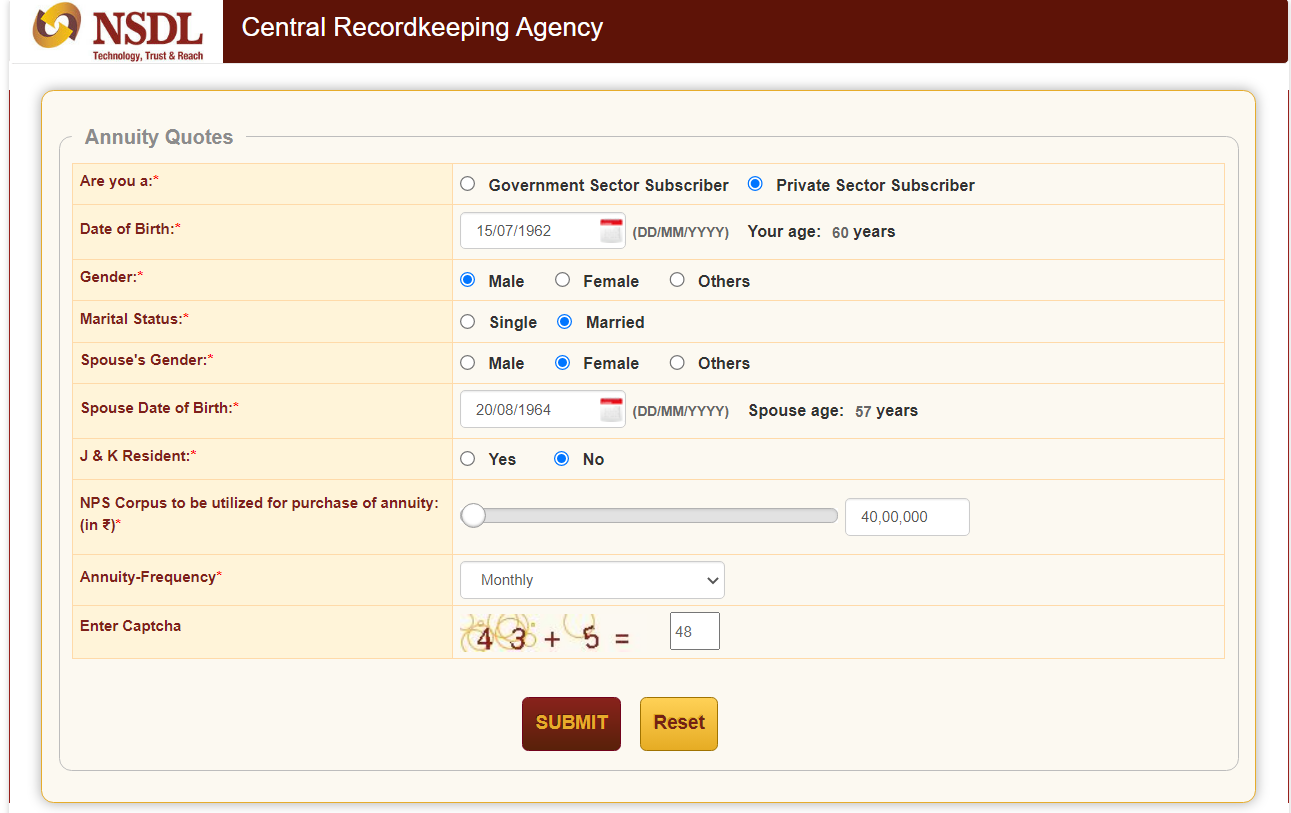

You can find out the amount of pension you are going to receive under each of these options of NPS annuity plans for all the Annuity Service Providers. You need to follow the three simple steps listed below:

- Visit this link on the NSDL CRA website- https://cra-nsdl.com/CRAOnline/aspQuote.html

- Enter all the relevant details

Enter the details as asked in the screen so displayed. Select the type of subscriber (Government/Private), Enter your Date of Birth, Gender, and Marital Status. Also, enter the amount you are going to purchase the annuity for and the frequency (monthly/quarterly/half-yearly/annually) of the annuity payment and the captcha.

- Click SUBMIT

Click on the SUBMIT Button. A table with the pension amount under each of the options of NPS annuity plans from all the Annuity Service Providers (ASPs) will be displayed on the following screen.

Let us take an example to understand it better.

Ravi, a private sector employee, will retire in a month, at 60. He had accumulated Rs.1 crore in his NPS account. According to NPS withdrawal rules, he can withdraw 60% of the accumulated amount (₹60,00,000) lump-sum and the balance amount i.e., ₹40,00,000 would be invested with any one of the annuity service providers for the purpose of regular pension.

His wife Rekha is 57 years of age.

Let us fill in the details of Ravi in the table on the NSDL CRA website and find out the amount of pension he would start receiving after retirement, under each of the options under the NPS annuity plans. He wants a monthly pension.

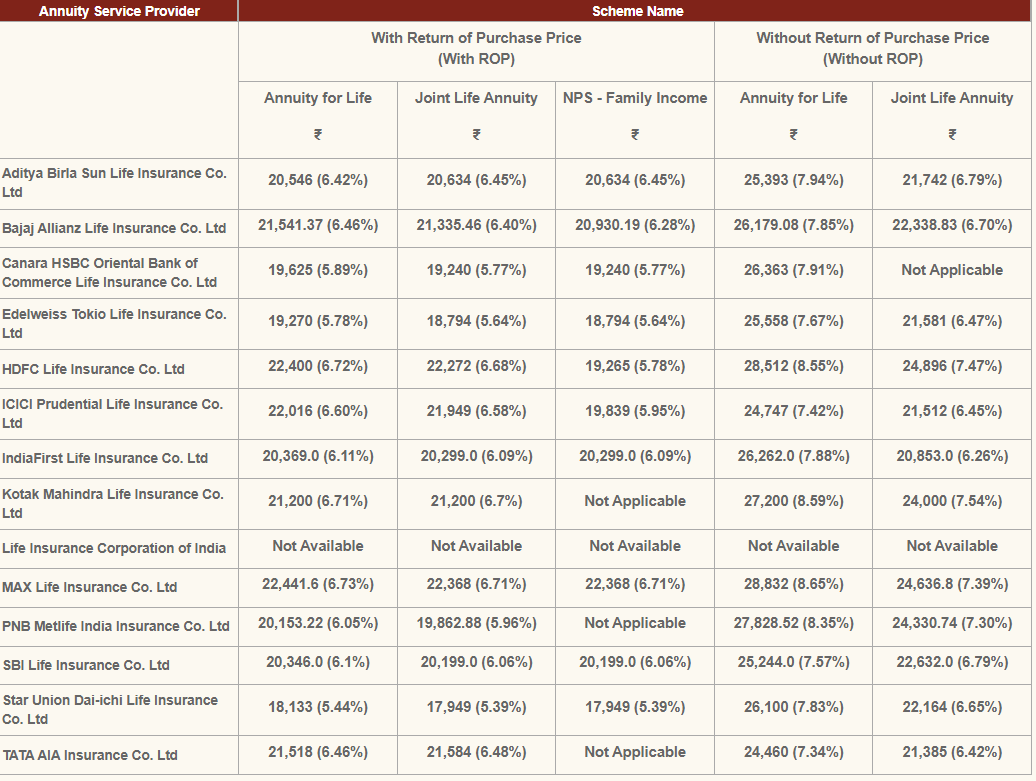

The following table would appear on screen, displaying the monthly pension amount under each annuity plan, based on the present annuity rates (July 2022). Please note that these may change in future with the changes in the annuity rates of the insurance companies.

Which NPS Annuity Plan should you choose?

It is clearly evident from the above table that if you have opted for the return of premium option, you would receive a lesser amount of pension as compared to the without return of premium option.

Also, the pension amount in the Joint Life option is less than the Single Life annuity option because of the fact that the annuity provider has to pay the pension for a longer period of time (until the spouse of the annuitant is alive).

So, the choice of NPS annuity plan would depend upon your requirements and situation. For example, if you are single and have no financial dependents, you can choose the annuity for life option.

If your requirements are getting fulfilled with a lower pension amount or have some other arrangements too for regular income like- government pension, etc. and you want to leave a lump-sum amount for your dependents ,or family members you can choose the return of purchase price option.

If you have no children or grand-children to take care of your spouse post-demise then a joint life annuity plan might suit you.

If you want to leave a lump-sum amount as well as want a regular income for your spouse, you may choose the NPS family income option.

Conclusion:

Buying an NPS annuity plan is compulsory after retirement with at least 40% of the accumulated NPS corpus. This not only inculcates a financial discipline but also protects the corpus from getting misused or mishandled by sellers or agents.

The purpose of an annuity plan post-retirement is to provide the safety of the principal and the certainty of regular income for the entire life, in other words, to safeguard against the longevity risk, not to earn returns.

But yes, it is also true that the post-retirement phase can be a long period, around 25-30 years or even more and might have different requirements. Since the annuity plan would provide a fixed pension, it cannot beat inflation in the long-run. You cannot rely upon the pension income from the NPS annuity plans to take care of the post-retirement needs.

Also read: What is inflation and how it impacts your financial plan?

So, it is important to design a robust post-retirement income distribution strategy to manage inflation and the taxation by dividing the investable corpus in different buckets meant for different needs.

Also read: Bucketing strategy to manage post-retirement income flow

On the other hand, if due to any reason you do not require a monthly income even three years after the exit from NPS, the buying of an annuity plan might be an unnecessary compulsion for you.

To answer such situations and to manage inflation, PFRDA might come up with an alternative option like that of a Systematic Withdrawal Plan (SWP) rather than the mandatory annuity purchase.

{kind=link}

please use gender-neutral pronouns. Using “he” for the reader and ‘she’ for their spouse is not making me feel inclusive or welcome to the financial schemes you are writing about. And, I as a human being and as a citizen, have the right to feel welcome.