LIC has come up with a new conventional pension plan naming “LIC New Jeevan Nidhi”. This year LIC has wished “happy new year” by launching 2 products – LIC Flexi Plus and LIC New Jeevan Nidhi.

It has become a need of the hour for the life Insurance companies to reconstruct their pension plans which should conform to the new guidelines of IRDA. To have a basic understanding of those guidelines read – HDFC Super Pension Plus review.

There’s 360-degree change in the pension plan space and now onwards you will be pitched with pension plan when you are looking for an instrument purely from retirement planning point of view. It has become compulsory now for any pension plan to distribute the surrender/maturity proceeds only in the form of an annuity.

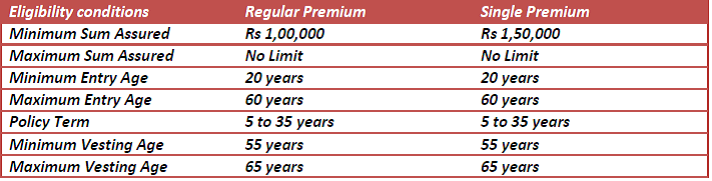

How LIC New Jeevan Nidhi pension plan works? In brief

LIC New Jeevan Nidhi is a Traditional/conventional with profit pension plan which provides death cover during deferment period and pension/annuity on vesting.

Annual premium will be decided as per the investor’s age, Investor health, sum assured and policy terms. The investor has to pay premiums for the full term or single premium and at the vesting age whatever be the fund value it has to be used to purchase the immediate annuity. And the annuity will be at the then annuity rates.

He may exercise the option to commute the fund value ( at the applicable Income tax rates which is 33% as of now) and rest has to be used to purchase annuity. Fund value will be Sum assured plus the

Fund value will be Sum assured plus the guaranteed additions *plus participating profits (non-guaranteed)** in the shape of simple reversionary bonus . One may also use the fund value to purchase another single premium deferred pension product if he satisfies the eligibility criteria of the same.

*Guaranteed additions : @ Rs 50 per thousand Sum assured for each completed year for first 5 years.

**Participation in profits : From 6th year onwards and will be as per corporations experience.

Benefits / Features of LIC New Jeevan Nidhi.

Vesting benefit: Use the maturity proceeds to either Purchase immediate annuity or a single premium deferred pension plan.

Death Benefit:

Death during the first 5 years of policy: Nominee will get Basic sum assured plus accrued guaranteed addition as the lump sum or annuity or partly as the lump sum and partly as an annuity.

Death after the first 5 years of policy: Nominee will get Basic sum assured plus accrued guaranteed additions plus simple reversionary and final additional bonus if any as the lump sum or annuity or partly as the lump sum and partly as an annuity.

Discontinuation of Premium:

You may discontinue paying the premiums or may even surrender the policy anytime after 3 years payment of premium. But in that case, also you will have to compulsorily purchase an immediate annuity or a single premium deferred pension plan with the paid up / surrender value. (Read: How Pension Plan works in India)

Other Features of LIC New Jeevan Nidhi pension plan.

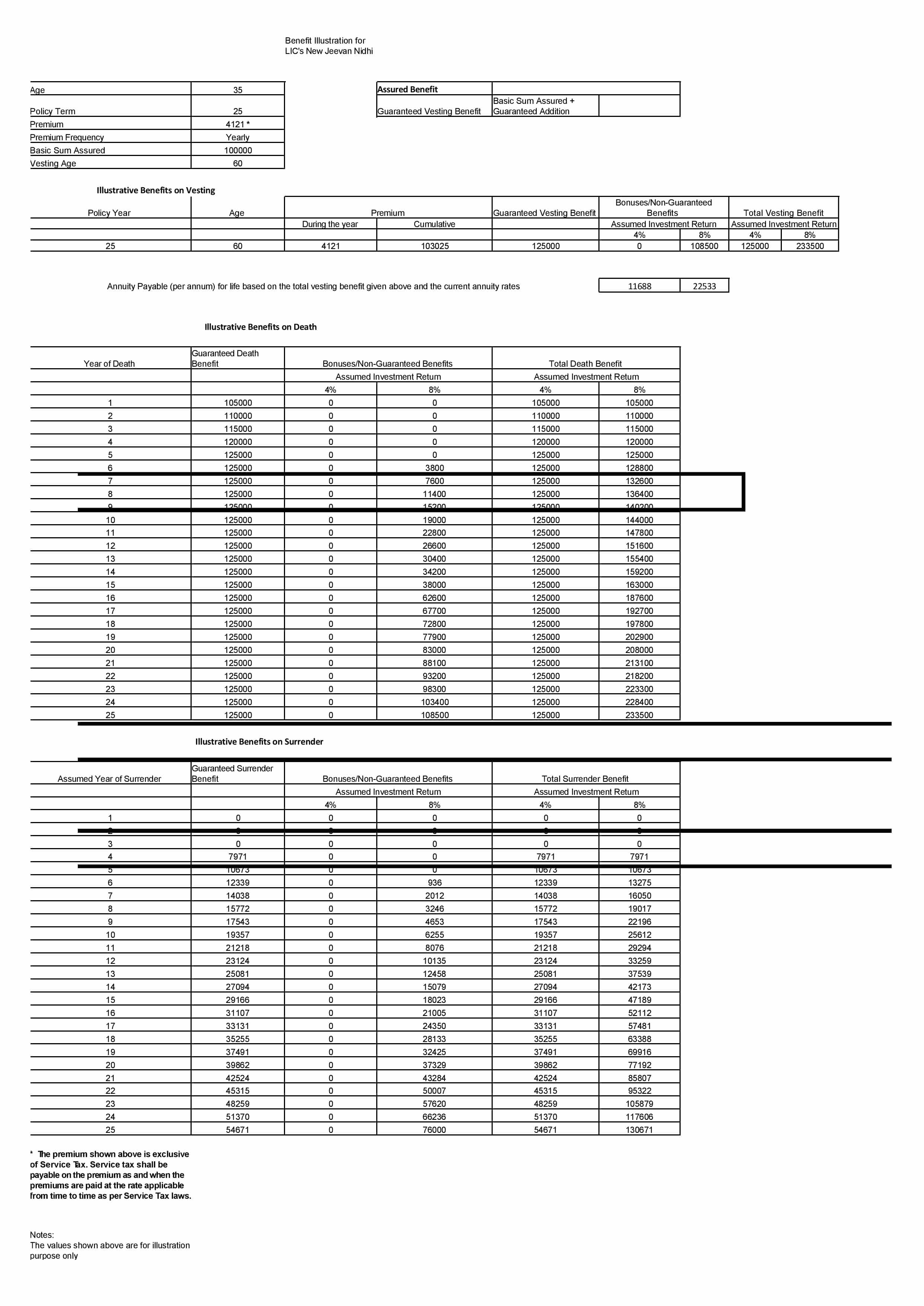

Let’s analyze the illustration of LIC New Jeevan Nidhi (from LIC website ) Click here to see the image

What this illustration of LIC new Jeevan Nidhi says is that if a healthy non-smoker person of 35 years of age buys this plan with the sum assured of Rs 1 lakh then his premium exclusive of service tax would be Rs 4121/- p.a.

Now if he continues paying the premium till vesting age of 60 years the product will be able to generate Rs 125000/- (@4% p.a ) or Rs 233500/- (@ 8% p.a). And if these maturity proceeds be used completely to buy an annuity for life, then it will be generating Rs 11688/- p.a or Rs 22533/- p.a. respectively as per current annuity rates.

Further LIC specifically says: in preparing this benefit illustration, it is assumed that the Projected Investment Rate of Return that LICI will be able to earn throughout the term of the policy will be 4% p.a. or 8% p.a., as the case may be. The Projected Investment Rate of Return is not guaranteed.

Now if I analyze the figures and calculate the net annualized return …it comes out to be 1.57% (@4%) and 6.22% (@8%). If I take into account the service tax also then returns are bound to come down.

As the returns are not guaranteed and being an endowment plan which is very expensive in terms of distribution cost so it would not be wise to assume the much of returns. It should be in the middle of both the extremes assumed.

Should you invest in LIC New Jeevan Nidhi?

Frankly, I am not in favor of any endowment plan in the accumulation stage of retirement planning (Read: Retirement vs pension plan). In fact, I am always of the view that investments should be flexible enough to be taken action on as and when required.

I may favor some immediate annuity plan at distribution stage but that too looking at the other financial requirement of the client. It would be very difficult to achieve one’s retirement goals if the money grows at 4-6% rate when inflation is hovering around 7-8%

Do share your own views on “LIC New Jeevan Nidhi” to have a healthy discussion on the same which will benefit other readers too.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Hi Manikaran!!

Thanks for the review. So in your opinion one should not go with endowment plans for investment. Then can us suggest any other investments for tax saving and for long term investment.

Sandeep..this is where the main problem lies. Investor has always one particular requirement in mind and look out for product that satisfies that requirement. Here you are particularly asking for tax saving and long term investment…but it should be other way around . You should be searching for product which can help you achieve one goal, which is far away and thus long term investment. and if that product can help in tax saving than that would be icing on the cake.

If i have to answer your particular query than i would advise you to go with PPF or NPS or mix of both. Otherwise you may contact me with your specific requirement.

Manikaran, I think this is reason there are very few financial planners are in the country. This is a common voice in india especially among practicing financial planners that investors should avoid endowment or ULIP plans. But in actual these are the instruments specially when launched by LIC to fund the government projects or to subscribe Govt companies ‘IPOs to help them in disinvestment. When you people write against government , you cannot succeed in India.

Ooops..Rashmi. U have actually made a very bold statement ” When you people write against government , you cannot succeed in India.”

But this is not true. Financial planning profession is growing with a fast pace. People in india are actually looking up to the professionals who can give fair ,unbiased and non product centric advise on the personal finance front. and with this view they are also ready to pay even for that advice. The Challenge is with the awareness front. When Financial planning word is being loosely used and anyone can call himself a financial planner there people gets confused.

Btw ..this article is just a review on the product and not anything against government.

RESPECTED SIR,

i’m yajnesh aged 26 yrs, i want to know about pension plans namely NEW JEEVAN NIDHI. my budget is 6LKH as a premium and i can pay 24k as yearly .MY QUERIES ARE * HOW MUCH AMOUNT WILL I GET AS A PENSION?

* FOR HOW MANY YEARS WILL I GET BONUS?

* PLZ EXPLAIN ME ABOUT SOME TECHNICAL WORDS U ARE USING HERE.

and also tell me about jeevan akshay v1 plan . please tell me about all these

I am invest in Jeevan Nidhi 818 single plan for 35 years .how much money I get for pension.

It depends upon the fund value accumulated and the prevailing annuity rate.