Income tax deductions under section 80C, 80CCD, 80D, etc. not only reduce the tax liability but also encourages savings and investments amongst taxpayers.

Not only in a savings plan, but you are also eligible to claim deductions on certain specified expenses done on medical treatment, education, home buying, etc. as well.

If you are a salaried employee, your employer might be asking you to submit a proposed investment declaration along with the tax regime opted for, to calculate the estimated tax on your salary. This document with the investments or expenses eligible for section 80 deductions will help lower the TDS deduction, of course under the old tax regime. If you have opted for the new tax regime, you need not submit any such document/proofs.

Also read: Old or new income tax regime: which one to choose?

In this post, we would try to explain some of the important deductions in income tax that are available for salaried employees, HUF, senior citizens, etc., and how you can efficiently utilize those in doing tax planning.

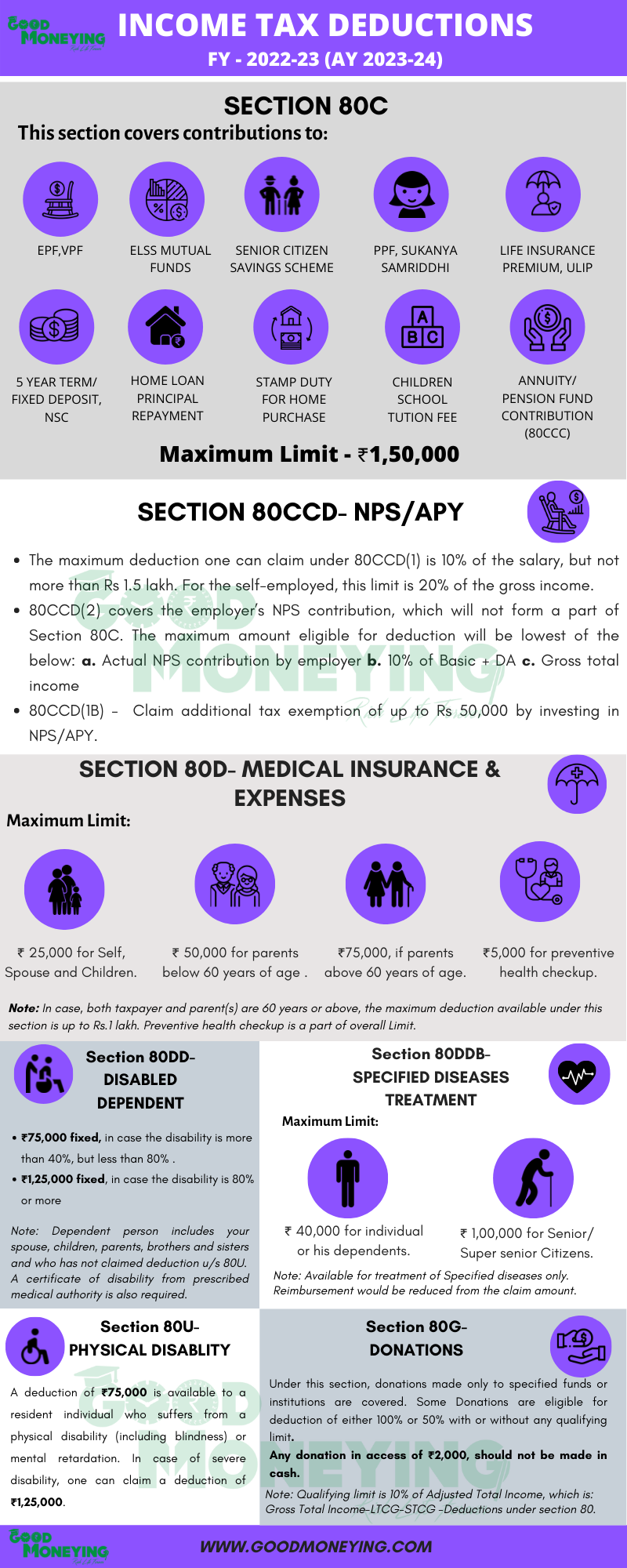

Do check the Income Tax Deductions Chart (infographics) at the end of this post.

Income Tax Deductions List FY 2022-23 (AY 2023-24):

Section 80C Deduction & Section 80CCD:

The following investments and expenses are eligible for deduction under sections 80C, 80CCC, and 80CCD of the income tax act:

| Section | Eligible Investments/expenses |

|---|---|

| 80C | Contributions made towards- EPF/VPF, PPF, ELSS mutual funds, Sukanya samriddhi, senior citizens savings scheme, NSC. 5-year term deposit, life insurance or ULIP premium, principal repayment of home loan, stamp duty paid towards house purchase, children’s school tuition fee (maximum 2 children). |

| 80CCC | Contributions made to any annuity or pension plan of a life insurance company. |

| 80CCD(1) | Both salaried employees and self-employed can claim this deduction on their contribution towards NPS, not more than- 10% of Basic Salary+DA (in case of an employee), 20% of gross total income (for self-employed). |

| 80CCD(1B) | Additional deduction of Rs. 50,000 for the investment done in NPS. Atal Pension Yojana is also eligible. |

| 80CCD(2) | It is available to employees for the employer’s contribution to NPS. The limit for the deduction is lower of- the amount of contribution or 14% of salary (for central government employees)/10% of salary (for other employees). It is available under both old and new income tax regimes. |

The aggregate income tax deduction limit under sections 80C, 80CCC and 80CCD(1) is Rs.1.50 Lakh and an additional deduction of Rs.50,000 is available under section 80CCD(1B).

Read our detailed articles on-

- Investments and expenses eligible for deduction under section 80C

- Employee Provident Fund (EPF)

- New Pension Scheme (NPS)

- Public Provident Fund (PPF)

- Sukanya Samriddhi Account

Section 80D: Income tax Deduction for medical insurance & expenses

Section 80D deduction is available if you have paid health insurance premiums or incurred any medical expenses. The limit of deduction is as below:

| Health Insurance Premium paid for | Maximum limit |

|---|---|

| Self, spouse & dependent children, none of them being senior citizens | Rs. 25,000 |

| Self, spouse, dependent children & parents, none of them being senior citizens | Rs. 50,000 |

| Self, spouse, dependent children & senior citizen parents | Rs.75,000 |

| Self, spouse, dependent children & parents, both being senior citizens | Rs. 1 Lakh |

Also read: Health insurance plans for Parents/Senior Citizens

Please note that tax deductions under section 80D can also be claimed for preventive health check-ups of upto Rs.5,000 within the overall limits mentioned above.

In the case of senior citizens, this deduction can also be claimed for medical treatment, if no health insurance is available.

If you have paid a lump-sum health insurance premium for more than one years’ cover, the deduction would be divided proportionately between the years for which the premium is paid.

Also read: Expenses on which you can save income tax

Section 80DD: Treatment & Maintenance of Disabled Dependent

This deduction can be claimed for the expenses incurred for treatment (including nursing), maintenance, or rehabilitation of a disabled dependent. Dependent means- spouse, children, parents, brothers, and sisters who have not claimed any income tax deductions under section 80U.

A fixed deduction of Rs. 75,000 is allowed if the disability is more than 40% but less than 80% (normal disability). In case the disability is more than 80%(severe disability), this fixed deduction increases to Rs. 1.25 Lakhs.

It is also allowed for the payment made towards an annuity scheme specifically meant for taking care of the disabled dependent. The plan would provide regular income or a lump-sum amount to the dependent upon the death of the taxpayer.

However, if the dependent with the disability predeceases the taxpayer, the amount received from any such plan would be added to his/her income and would be chargeable to tax accordingly.

Please note that a certificate issued by the medical authority is required to claim this deduction.

Section 80DDB: Treatment of Specified Diseases

Income tax deduction under this section is allowed for the expenses incurred over treatment of some specific diseases or ailments on self or dependents (spouse, children, parents, brothers, and sisters).

For individuals below the age of 60, the maximum amount of deduction under section 80DDB is Rs.40,000. For senior citizens (above 60), the maximum limit for this deduction is Rs.1 lakh.

Some of the diseases include- neurological disorders, malignant cancer, AIDS, thalassemia, hemophilia, etc.

Please note, this deduction is available only on the basis of the prescription provided by a specialist doctor and the amount of claim would be reduced in case any reimbursement of the expenses is received.

Section 80U: Income tax Deductions for Physical Disability

This deduction is for resident individuals suffering from physical disability. In the case of normal disability (more than 40% but less than 80%), a deduction of Rs.75,000 is available. If the person suffers from a severe disability (more than 80%) the deduction increases to Rs. 1.25 Lakhs.

Disabilities include- autism, blindness, hearing impairment, cerebral palsy, mental illness/retardation, etc. These are also applicable to section 80DD.

Section 80G & Section 80GGA: Donations

Under section 80G, you can claim tax deductions by giving donations to certain specified charitable institutions, trusts, or charitable funds.

The amount of deduction depends upon the category in which the fund or institution to which the donation is made falls into.

Some donations are eligible for a 100% tax deduction. While for some donations deduction is allowed only upto 50%.

For some other donations, the amount of deduction- 100% or 50% as the case may be is subject to a qualifying limit of 10% of Adjusted Total Income.

Adjusted Total Income is calculated as:

| Gross Total Income | XXX |

| less: Short-term capital gains | (xxx) |

| less: Long-term capital gains | (xxx) |

| less: Income tax Deductions claimed under sections 80C to 80U | (xxx) |

| Adjusted Total Income | XXX |

For the list of specified funds and charitable institutions and the amount of eligible deduction, click here

Section 80GGA deduction can be claimed by individuals not having any income from business or profession for donations to those associations or institutions engaged in scientific research or rural development.

Please note, that income tax deductions under sections 80G and 80GGA are not allowed if the amount of donation exceeds Rs. 2,000 and the amount is paid in cash.

Section 80GG: Deduction for house rent paid

Income tax deductions for salaried employees, self-employed, businesspersons, etc. under this section are available for the house rent paid and no House Rent Allowance (HRA) is received. The following conditions need to be satisfied to claim this deduction, you should:

- be residing in the same house for which you are paying the rent.

- not own any residential accommodation in the name of self, spouse, or minor child at the place of ordinary residence or employment.

- not own any self-occupied house property at any other place.

The quantum of the tax deduction would be the least of the following:

- Rent paid – 10% of Adjusted Total Income

- 25% of Adjusted Total Income

- Rs. 5,000 per month

Please note, that the computation of Adjusted total income would be the same as section 80G.

Also read: Section 80GG: deductions in income tax for house rent paid

Income Tax Deductions Under Section 80E, 80EEA & 80EEB:

| Section | Details |

|---|---|

| 80E | Deduction for interest on education loan for the higher education of self, spouse, children, or student for whom you are a legal guardian. It is available for a maximum up to 8 years starting from the year in which the interest is paid. |

| 80EEA | Additional deduction of 1.50 lakhs over and above the deduction under section 24b for interest payable on home loan to first-time homeowners for buying a new home, sanctioned between 01-04-2019 to 31-03-2022. The value of the property should not exceed Rs.45 lakhs. |

| 80EEB | A tax deduction of up to Rs.1.50 Lakhs on the interest paid on loan taken to purchase electric vehicles, between 01-04-2019 to 31-03-2023. |

Please note that the above deductions are available only when the loan is taken from a financial institution i.e., Bank or NBFC.

Check our detailed articles on-

Income Tax Deductions Under Section 80TTA & 80TTB:

| Section | Details |

|---|---|

| 80TTA | A deduction of up to Rs.10,000 on the Interest received on your savings account in a bank, co-operative society, or post office. It is not available for senior citizens. |

| 80TTB | A deduction of up to Rs.50,000 on the Interest received by senior citizens on the savings account in a bank, co-operative society, or post office and fixed deposits. |

Also read: 5 Tax Benefits for senior citizens

Standard Deduction:

Apart from these section 80 deductions, if you are a salaried employee or a retired pensioner you are also entitled to a standard deduction. It is a fixed deduction of Rs. 50,000 from your salary income.

Also read: Standard deduction in income tax

Income Tax Deductions Chart FY 2022-23 (Infographics):

The below infographic summarizes income tax deductions under section 80C, 80CCD, 80D, 80DD, 80DDB, 80U and 80G:

Conclusion:

It is wise to do your tax planning at the beginning of the financial year to do away with the last-minute hassles. It also helps in selecting the suitable investments which support your financial goals too.

Waiting until the last minute for your tax planning may lead you to unsuitable financial products which may ruin your financial health and hamper your financial goals.

Income Tax Deductions list 2022-23 would help you take advantage of some of the provisions of tax laws in planning your taxes wisely. For comprehensive tax planning, you should consult a qualified tax expert.

You may download the Income-tax deductions pdf, the ready tax-reckoner for salaried employees being released by the income tax department.

This Article is written by Mr. Varun Baid, CFP Professional

{kind=link}