ICICI Prudential health saver is a unit linked health insurance plan, designed in such a way that draws attention towards it at the first sight.

There are those who still consider health insurance premium is an unnecessary expense as they assume they are young and healthy, drive the vehicle very carefully or have enough coverage from their employer, for them ICICI prudential health saver can be a head turner as like other ULIPs it also comes as a bundle of insurance and investments.

It makes people feel that “paisa to wapis mil jaega na”- (at least they will get their investment back). Let’s go deeper and understand whether ICICI Prudential health saver is really a worth purchase or not?

ICICI Prudential Health saver – in Brief

ICICI prudential Health saver is a unit linked health insurance plan having 2 portions in it. One is health insurance and other is an investment.

Health insurance portion takes care of medical expenses in case of hospitalisation of insured and on the other side investment portion builds a health fund which takes care of expenses not covered in the hospitalisation benefit.

Unlike other health insurance plans offered by life insurance providers which are more like cash benefit plans, in ICICI Prudential Health saver plan, hospitalisation insurance benefit is just like any other mediclaim.

The premium payment after deduction of allocation charges, administration charges, Insurance charges gets invested in a portfolio of your choice (out of 7 different portfolios) and termed as Health savings fund.

This health savings fund can be used after 3 completed policy years in the percentage specified for different years for the reimbursement of health care costs incurred like on medicines and drugs, diagnostic expenses, dental expenses, co-pays in medical insurance and other miscellaneous medical expenses not covered in medical insurance.

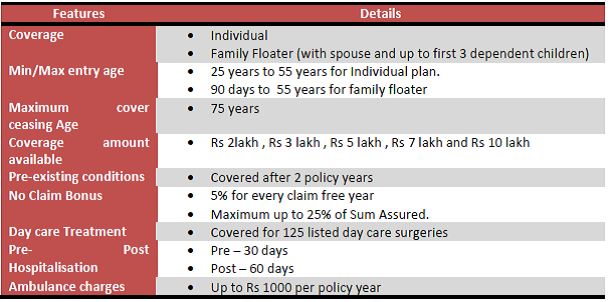

Key features of ICICI Prudential Health saver

Other Additional Features of ICICI Prudential Health saver

- Reimbursement of medical tests subject to a limit of Rs 5000 or 1% of annual sum assured limit whichever is lower, once every 2 years.

- In the case of a claim, the accumulated no claim bonus will be reduced by 10% of the base annual limit in the following year.

- A co-pay of 20% will be applicable on medical expenses in case –

- Stay in single AC room with a room rent of more than 1% of the annual coverage limit

- Get treatment in the non-listed hospital network.

Though in the case of emergency hospitalisation related to trauma or cardiac cases, co pays will not be levied.

4. In Health savings fund 4 switches are allowed every policy year. Subsequent switches will be charged Rs 100 per switch.

Annual Premium Rates

Premium Allocation Charges

Other Charges

Policy administration charges Rs 60-90 per month depending on the frequency of premium payment. Besides this, there are some fund management charges on different portfolios in health savings fund.

There are Insurance charges also which you can call as a health insurance premium, which varies with age and sum assured opted for.

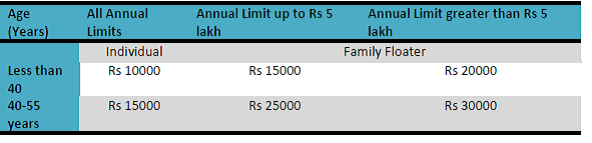

Health savings benefit claim chart

Should you opt for ICICI Prudential Health saver as your health insurance plan?

ICICI Prudential health saver has many good features in it. Like Offering alternate year health check-up, Tax saving u/s 80D along with no compromise on health insurance coverage, insurance Coverage available up to Rs 10 lakh.

(Read: How to select the best Health Insurance Policy in India?)

But on the other side, this is an old policy and thus having age-old features like having a maximum cover ceasing age, maximum entry age, no claim bonus only up to 25%, day care coverages only up to 125 surgeries etc. These days there are many other innovative policies are available in the market with full of features. Standalone health insurers like Apollo, Max bupa, Religare has very attractive features as far as health insurance is concerned (Read : max bupa Family First).

As far as a feature of health savings fund is concerned this is just a portion of your premium which is getting invested in a fund which you can claim later on for your medical reimbursement. Proper planning can take care of this aspect too. So, as we always say, that keep your insurance and investment separate, this advice applies in ICICI prudential health saver also.

Also Read : Religare health insurance Care

My View is to buy a standalone comprehensive health insurance coverage and create a health emergency fund by saving somewhere in liquid/safe instruments as per your risk profile. It’s Better to avoid products like ICICI prudential health saver.

What are your views? did you like the features of ICICI Prudential health saver?

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Dear Manikaran,

I have few queries regarding Health Savings Fund which is part of this policy for which I am not able to get correct answers. Please let me know your thoughts:

1. In case of death of insured person, will this fund be given to nominee or not?

2. In case of policy maturity that is 75 years of age for insured person, will this accumulated fund be given to the person or not?

3. In case I surrender this policy (I took this policy in Oct 2009, 15K premium, 5 Lacs cover, Age 30, Male) after minimum premium paying period, will I get accumulated fund value or not?

4. There is one option for Cover Continuance option after 5 years of regular premium payment. Should I opt for that option after 5 premium payments or not?

I am asking this question because there is a clause in this policy which states that we can claim this money only for health care cost.

Regards.

Vijay

Please find my answers below, in the same sequence of questions:

1. On death of Insured Person(s) during the Hospitalisation or Day Care Procedure, the Company shall pay the Hospitalisation Insurance Benefit towards Pre-Hospitalisation, Hospitalisation or Day Care Procedure, as thecase may be also the Company shall also pay the Fund Value under the Policy to the nominee.

2. Its a very valid question raised but policy wordings are silent on this clause. Where it specifically says that no surrender (full or partial) is allowed in this policy, it doesn’t speak about the money on maturity. I will try to find out its answer and update you later .

3. Surrenders- either total or partial is not allowed in this policy.

4. After payment of five full years’ premiums, if any subsequent premium payment is not made, the Policy will continue for all benefits including insurance cover with charges being deducted by cancellation of Units. Thereafter if the Fund Value reaches or falls below 110% of one full year’s premium the Policy will be foreclosed. The foreclosure Fund Value (Fund Value as on the foreclosure date based on that day’s NAV) can be claimed within the next five years as Health Savings Benefit subject to a maximum limit of 50% of the foreclosed Fund Value. The maximum aggregate benefit that can be claimed over the five years is limited to the foreclosed Fund Value. On death of the Primary Insured during this period, foreclosed Fund Value minus any Health Savings Benefit paid during this period will be payable to the nominee.

In 2009 i have started icici health saver policy with Rs.15k for 2 lac annual limit for my family of 2+2.

Now i want to increase my annual limit to 5 lacks which is costing 25,000/- premium.

So what shall i do – stop this policy and go another fresh one of continue.

As on Sep 23 my saver fund value just 25k ( paid 60k towards premiums sinces 4 years)

October 20 is next premium date – so give me advice.

Dear Srinivas,

A few things that you should consider before taking a decision:

1. In the new policy the waiting periods and exclusions will start all over gain

2. Health Insurance premium increases with age

3. ICICI Pru Health Saver has a unique feature which helps you build funds which can be used for OPD expenses, other expenses not covered under hospitalization plan. The other plans may not help you accumulate a kitty for health related expenses, which is required as you grow older.

ICICI Pru Health Saver features can be accessed via this link http://www.iciciprulife.com/public/pdf/Health_Saver_brochure_6may.pdf. Do let us know if you wish to meet or speak to our advisor for any other clarification.

Regards,

ICICI Prudential Life Insurance Help

Srinivas, as now you want to increase the cover which will cost you Rs 25k in icici. so it becomes your first point of comparison with other products. Find out if you can get the same features and benefits somewhere else. This icici policy demands more premium outflow as it has a saving feature attached to it , so if you ignore this feature then you can get a better cost effective deal and better product somewhere else.

Dear sir, l have started same policy in 18 feb 2010 for my family 2+1with regular premium 15k for 5lakh.now I want to add my kid having birth date 15 July 2012.all policy year are claimfree.today my fund value appr.30k.so please tell me about my new premium and is it good to continue with new .or go to other plan for small kid.

Kiran, for the new premium quotes you better contact ICICI Pru people or some of there agent.

As far as policy is concerned i have clearly mentioned in the article above that there are much better policies available as of now in the market like of Religare health or Apollo Munich, so you can go through the features of the these policies for a better decision making.

Dear Mr. Kiran,

Thank you for choosing ICICI Prudential Life Insurance. In response to your query we would like to inform you that ICICI Pru Health Saver allows you to add a family member to your existing policy. This is allowed only in event of a marriage or birth of a child. The change shall be effective for the purpose of this policy from the next premium due date. For more details you can write to us on [email protected]

To help you make the most out of your policy we would like to inform you about the free health check-up feature. In this policy you avail of a free health check-up subject to a limit of Rs. 5000 or 1% of the annual limit, whichever is lower, once every two years after the first year. Benefit is valid for only one member of the family at given point in time.

Do let us know if we can help you I any other way.

Regards,

ICICI Prudential Life Insurance

sir,

i wants to surrender ICICI HEALTH SAVER POLICY

, as i can not pay further premiums due to some reasons.How i get my fund value from icici pru life I have paid four premiums of Rs.25000. per year Pl.advise me ,i requires my money back as it was told by icici agent that i will get some money as partial withdrawal.

OR partial withdrawal is possible in this policy

Dear Mr. Khairnar,

We request you to help us with your contact details to assist you.

Alternatively, you may also post your request along with your policy details on https://onlinelifeinsurance.iciciprulife.com/digital/ipru/GrievanceRedressal.htm?execution=e1s1

Request you to quote the reference number 041385_aaal whilst sharing the details. Post receipt of the requirement, our representative will get in touch with you within 48 hours.

Regards,

iciciprulife.com

Dear Sir,

I have taken ICICI Prudential Health Saver (Medic lamp) Policy.

My Policy No Is :- 17759310

I have one confusion in this policy.

My agent tell me in this policy you will get your money back while maturity on market value 6 to 10%.

But I went to your office(maninagar branch, ahmedabad) & your office adviser told me you can’t get money back while maturity.

Can I stop premium after 5 year & my policy will continue while 72 year.

If no its ok but yes what is condition for continue for policy

I also read policy but I can’t understand.

So please give total detail of this policy.

So I am very confuse will I get money while maturity or not.

So please conform me.

should I stop my premium or continue.

Please tell me good detail from your side.

Name :- Dharmendra Sahu

My contact no :- 09429019064

My policy due date is 16-05-2014 So I can decide should I continue or not.

Waiting For Your best Reply,

Warm Regard,

Dharmendra Sahu

Dear Mr. Sahu,

We are sorry to hear your concern. Our representative will get in touch with you in the next 4 hours to assist you with your concern.

We appreciate your patience.

Regards,

http://www.iciciprulife.com

Dear Sir,

i mean in this policy i will get my money back while maturity.

my agent tell me you will get & i go to your company (icici maninagar branch) thay tell me you can’t get your money on maturity.

& Also If I stop my periume after 5 year what i have to do continue to policy

Dharmendra

Dear Mr. Sahu,

We understand our representative has contacted you and acknowledged your concern. Please be assured that the concern highlighted by you is currently being reviewed and we shall keep you posted on the further development of the case.

Regards,

http://www.iciciprulife.com

Dear Mr. Sahu,

We wish to inform you that the concern highlighted by you has been reviewed. Accordingly, a communication has been sent to your registered email address with the details of the resolution offered.

In case of any further clarification, please contact us on our Customer Care number 1860 266 7766 or write to us at [email protected].

Regards,

http://www.iciciprulife.com

Dear Sir,

I am 35 yrs old and looking for long term health plan . I am very much confused for the following reasons.

I did some research on the Health Insurance packages available in the MKt right now.

I observed that maxbupa, Apollo munich and Star health are offering some good plans.

But Medical insurance plan are of max for 2 yrs term afterwards renewal is required + they have premium based on age band like

(1yrs – 35) ( 35-45)…. But i observed that at the age of 55-60 there premiums are floating anywhere between ~60k to 1lakh.

I was in thought what if a person take such health plan and continue to 15-20 yrs with no claim bonus then on attaining the age of 60

he would be unable to pay such high premium ( 60k to 1 l) becoz of some reason or other reason.

then he will be no longer get any benefit from such medical insurance even though he paid a premium for good long length.

My question :-

Is there any Plan in mkt (just like general insurance)that offer flat premium let’s say 15k/annum for a term of 20-30 yrs.

Don’t mind if the medical coverage will be less. At least a person can secure himself by such insurance with less benefits

Or what will your suggestion in above scenario

Regards

Mandy

Mandy, I understand your concern. buy may i pls know what kind of coverage you are looking for? I mean , i an unable to get as to which company asks for such high premium in the age group of 60-65 years.

I have one policy of Religare health for my mother who is 65 years of age and i am paying Rs 18000 p.a for the same for Sum assured of Rs 5 lakh.

See in all health insurance plans, premiums are bound to rise with age.

Sir ,

family floater (2A +2c) are costing this much as of today i.e apollo ( optima restore).

second thing that i also have medical coverage with my company provided. I was thinking of to take a small plan of SA 3 L. As per your best knowledge which among these starhealth, TATA AIg and apollo will be best .as a backup plan for family policy. Do you really think the company with direct settlement will be more beneficial instead of company with TPA

I also had discussion with one of the financial person , he suggested to make some kind of deposit and fund for old age. from that’s interest medical policy can be continued.

Mandy, by the time you reach 60, the children you want to cover in the plan will be come adults and will be having separate policies.

I have both good and bad experiences from both TPA and direct settlement but still i feel that when you directly deal with company the process work faster. Company is concerned about its own reputation.

You got a right advice of maintaining deposit and medical fund for old age. This will also help you in managing those medical costs which are not covered in any health policy.

All the best

Hi,

I have a ICICI Prudential Health Saver Plan with coverage of 5Lakhs (Covering wife & one kid).

I would like to add other kids name in this policy & keep the annual limit same I have visited the branch but they have given me new proposal with increased premium (from 15 K Per year to 23K Per year).

I do not understand, why there is increase in premium since I have a family floater plan & do not want to increase annual coverage.

Thanks

Shri

I have taken policy of icici prudential ….insurance..i have paid 4 premiums of rs 15000 each..now i dont want to continue with the policy …as i cant pay the premium….cn u tell what will be my surrender value………i ws told on taking the policy if i wish to discontiue i wil get partial amount…….plz help..my policy expiring on september7th

Mauli you need to contact icici pru people to get the surrender value.

sir i want a family health plan for me 32 wife 34 and son 6 . i search many plans in detail on internet but i am so confused about (1) which company solved claim faster with high claim settlement ratio (2) pre excisting disease the word which make more confused ……the medical problem and history and symptoms which i know i disclose to the insurance company ……but if a problem which i dont know how can i disclose and in future company reject claim on that basis….(3) i talk to many broker and company advisor for a health checkup of all family members ….. that in future there is no confusion about pre excisting and picture is clear….cost of checkup i will paid…..but all advisor says health checkup for 45+ age only…….(4) sir pls solve my problem about pre excisting and how can i have a health checkup of my family that i have a proof about preexcisting dicesease that healp me in future at time of claim

You buy health policy by disclosing whatever is known to you. If you want to be sure of your health, then get checkup done at your level and keep the reports with you. Companies won’t ask for any medical check up before 45 years of age unless the sum assured asked in more.

Don’t be afraid of anything which is not in your knowledge, to be on safer side you are getting your health check up done and this is what you can do. and keeping the records with you will justify if in future, insurer raise objection on hiding of facts (if any).

and as far as claim settlement record is concerned, no such data is available in public domain, so go with any company having more than 5 years of presence in this sector.

I am having Health saver policy no 12671728 since OCT 2009 and has paid all the premium on time.

1)In this policy key features there is point regarding no claim bonus of 5% of the annual limit accrued for every claim free year up to max of 25% but till date i have not received any such benefit so make sure that i will get those benefit.

2)Also my regular premium amount was Rs 22000/- per year, but while visiting my portfolio on your website the premium amount showing is Rs 88000/- so pl clarify.

3) Now as my policy is 7 years old if i opt for cover continuance option without payment of further premium what are the advantages and disadvantages in future.

Mr Rajendra, it seems you wanted to send mail to ipru people, not me.

According to the Health Insurance Portability IRDA is the insurance scheme or not.

I have a family floater with ICICI Pru for 7 lakhs covering me and my family of wife and two children.Till date I have not claimed a single penny from the Company.But has been regularly paying the Annual Premium…..I live in Hazaribagh , Jharkhand which hardly has any proper big hospital like Apollo,Medanta….but how can I at least avail my free medical check up for family which I should get….. Please Advise.

You should better check this up with the ICICI People. Call them at their call center number or write a mail to them.

Non of your answers are transparent and straight , you are bypassing all the answer if you have the answer of the relevant questions being a knowledges person then only carry on answering otherwise we don’t need your diplomatic answer = no solution. Be straight while answering and understandable to the policy holder .. I am having a same issue as your representative told me that I would get the fund back in maturity but now I see all they lied to us …! My number is +91 6294-823689 if you can help me please ..

Hy don’t buy this policy when you close the policy no return of money , my policy no is 18110324 and my email : joisar_nv @rediff.com, i pay 25000 primium and after ia close the policy , there is no return money for me and agent also not up to the standard.

sir,

i wants to surrender ICICI HEALTH SAVER POLICY

, as i can not pay further premiums due to some reasons.How i get my fund value from icici pru life I have paid four premiums of Rs.25000. per year Pl.advise me ,i requires my money back as it was told by icici agent that i will get some money as partial withdrawal.

OR partial withdrawal is possible in this policy

Policy due dt. 25/03/17

My policy no 17529490

Mob. no. 9975414230

Dhiraj, you need to contact icici pru people for this. You may call up there call center or visit any nearest Branch.

Dear Sir,

i have a health saver insurance policy from ICICI Prudential

i have been paying for last seven years 25000 pm , and have not claimed any thing,

i was informed that you will be covered under mediclaim up to 75 years .

please suggest should i continue with further premium up to 10 years

25000 p.m. in health saver does not look sense to me. Buy Health insurance cover separately and invest money elsewhere wisely.

I have the ICICI Pru Health Saver insurance for last 8 years. I would like to know the advantages of renewing it. How do I claim annual health check up charges?

Since you are continuing the policy for the last 8 years, the sum assured would have been Rs. 5 lakhs, which is not adequate in the current times. Firstly, you need to increase the cover.

Frankly, we do not see any advantage in renewing the policy. It would be better to go with a comprehensive health plan for your health insurance needs and separate investment planning suitable to your risk profile and goals. It would not be wise to mix both.

For the annual health check-up claim, you need to contact the Insurance company or read the details as mentioned in the policy document.