Debt investments for long term, no way. Long term means equity only. This is what the norm these days is, this is what is being told, and this is what is being preached as best, since only equity investments are expected to give best returns over longer period. Debt is meant for short term.

The above is the general view in the market. All novices and even expert investors are getting over board on equity investments, not because they understand equity very well, but they are seeing the stock markets performing quite well.

Why debt investments for long term – a Perspective

The reason of me having this view is that at the core, Investors are human being, and thus are Loss averse, which means that loss gives them more pain then the comfort coming from gains.

A sudden fall in the market can change the view point in minutes. And just like rise, fall is also a reality, and the major test of patience for all the so called aware and long term investors will be in the falling market.

In my practice and process, finding the risk tolerance level of the Investors is important to suggest them a suitable Asset allocation mix.

Further the past data as researched by the risk tolerance software “Finametrica”, makes people realize that to have a good and stable portfolio they have to have a good mix of Equity with debt even for long term, else the portfolio will become so volatile which may start making them uncomfortable.

I am going to share with you some of the data from the same reports to let you understand why debt investments are important for long term too.

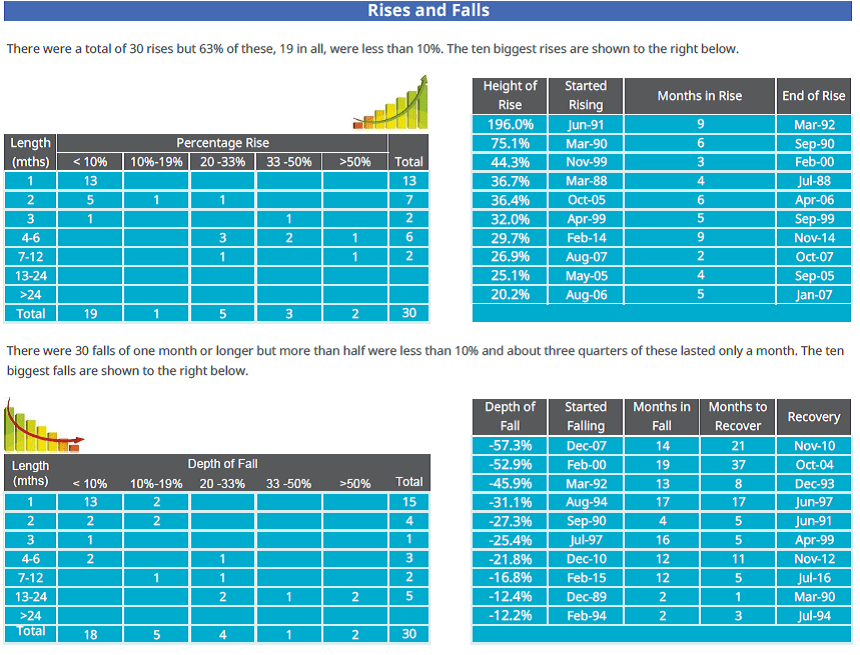

100% equity allocation has fallen by 57.3% in December 2007, the fall was spread in 14 months and 21 months to recover from there, thus it took almost 3 years to recover back to the same level.

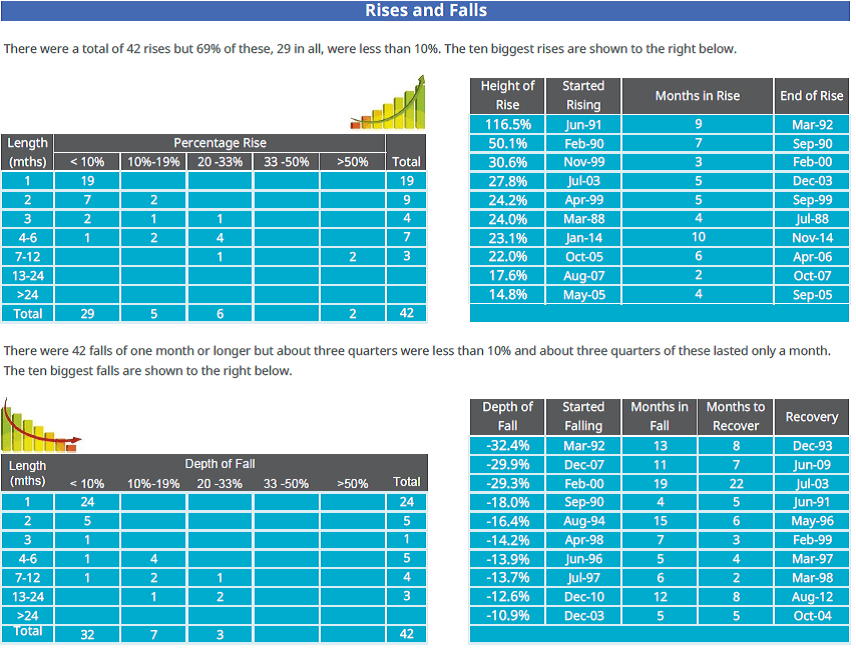

Just compare the depth of falls with 100% equity. By reducing 40% exposure from direct equity, you have compromised the returns of 0.82%, but also have considerably brought down the volatility of your portfolio.

Please understand that debt is not a no earner in the portfolio. Where debt brings balance in your portfolio’s volatility, it also brings potential of earning good returns too, especially in falling interest rate scenario.

Conclusion:

If you are a serious long term investor then look at the things from fundamental point of view and have a suitably allocated portfolio into Equity and debt both.

{kind=link}