Capital gain bonds are used to save long-term capital gain tax on the sale of property (Residential or non-residential). But at the time of rising stock market scenario, one question always crops up in the mind of Investors, as to if they should Invest in Capital gain bonds or Pay tax and Invest the balance in shares or Mutual funds by following an Asset Allocation. This is with expectations that money will remain liquid and also will generate more as compared to capital gain bonds which has an interest rate of 5% p.a. (w.e.f. 1st Aug 2020) and that too taxable.

These kinds of queries have been increased post demonetization especially from those who were lucky enough to sell their properties before 8th November 2016. Though they have another option too to save long-term capital gain tax on the sale of property by buying another residential house within the next 2 years or constructing a residential house in the next 3 years of the sale of property, they do not want to buy another Real estate …at least for now.

Now, to decide if they should buy capital gain bonds or not, let’s first understand what these capital gain bonds are and how they work, in brief.

What are capital gain bonds and how they work?

When you sell a property, be it commercial, residential, or even Plot, then whatever gain comes out of that transaction is termed as Capital gains since the property is a capital asset.

Now depending on the holding period of that capital asset i.e. the time you have held that asset, before selling it, gain from the same, is termed as the Long term or short-term capital gain. (Also Read: All about capital gain taxation on Mutual Funds)

As per Income tax laws, the minimum holding period to qualify real asset as long term is 2 years (w.e.f April 1. 2018, as proposed in Budget 2017), means if you sell the property after April 1, 2018, then the minimum holding period would be 2 years, but if you have sold the property in 2017 then the required holding period to qualify the transaction as long-term was 3 years.

Short term capital gain will be added to your total income and will be taxed as per your Income-tax slabs, whereas Long term capital gain on a property will be taxed as 20% after providing for indexation benefit. Read more on Indexation benefit here.

Capital gain bonds are the eligible financial instruments under section 54EC, in which investors can invest the capital gain amount and save oneself from paying any long-term capital gain tax on the sale of the property. Investment has to be made within 6 months from the date of sale.

These bonds are issued by NHAI (National Highway Authority of India) and REC (Rural Electrification Corporation). In Budget 2017, Finance Minister has proposed to come up with more bonds or financial Instruments to save long-term capital gain tax on the sale of the property.

There is a lock-in period of 5 years(W.e.f 1 April 2018) and the current rate of Interest is 5.75% per annum payable annually (Taxable). The maximum you can invest is Rs 50 lakh. W.e.f. 1 Aug 2020, the interest rate on these bonds is reduced to 5% p.a.

Seeing the low-interest rates and that too taxable, one generally gets reluctant to invest the money generated from the growing real estate, and look out for other options available. Another alternative is to pay tax and invest money in another growing asset like equity. But, would that be feasible, let’s do some maths to find out.

Capital gain bonds Vs. Investment elsewhere

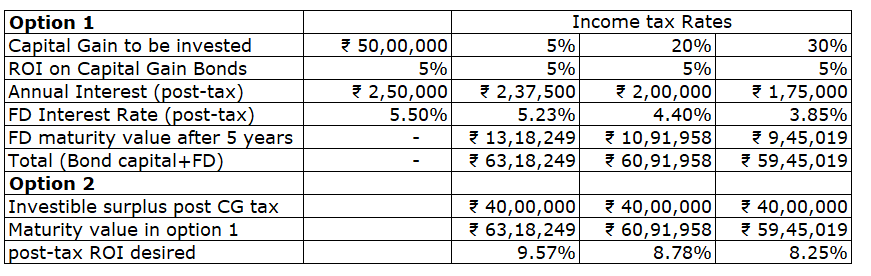

Just to make the calculation simpler, I have taken Capital gain after Indexation amount to be Rs 50 lakh only so the full amount can be invested and should be under the maximum limit of capital gain bonds. I have assumed that the annual interest from Bonds is being reinvested in bank Fixed deposits which have ROI as 5.50% (pre-tax). FD interests are compounded quarterly, but I have taken annual compounding. Also, the cess on Income tax is ignored.

What the above table shows is that If someone invests the complete capital gain/sale proceeds in capital gain bonds and also keep reinvesting the Annual interest in bank FD then the post-tax maturity value would be 63.18 lakh, 60.92 lakh, and 59.45 lakh for someone in 5%, 20% or 30% tax bracket respectively. But the calculation can slightly differ if the investor opts for the new tax slab rates.

Option 2 shows that if you pay capital gain tax and invest the money somewhere else, then how much return your investment should generate to beat the returns from capital gain bonds investments.

Conclusion – Should you invest In capital gain Bonds?

It is quite evident from the above calculations that how much the investor needs to generate from other investments, to compare it with the bond investments.

The desired ROI may not look that difficult to achieve if the asset allocation approach is followed. Read more on Asset Allocation here.

However, as you know shares and mutual funds are not fixed return instruments and are market-linked products, so there is considerable risk involved in the complete transaction. (Also Read: What is Equity?)

If one is comfortable with the volatility and agrees to accept the inherent risk, then one may go with the paying tax and invest options, else capital gain bonds will be suitable. (Also Read: 5 Best Things to do in Volatile Markets)

Moreover, investing always should commensurate with your goal requirements and tax planning should be part of your holistic financial plan. (Also Read: Financial Plan or Financial Planning- What is more important?)

Sometimes it is desirable to take the risk if the money is to be invested for a very long-term horizon, and sometimes it is not advisable to take such risks as the goal is nearby and you have enough money for that goal. So, one has to decide accordingly.

Hope this article would help in making the decision to buy capital gain bonds or pay long-term capital gain tax and invest money elsewhere. Share your views and queries in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Simply it means that as long as you are sure that you would be able to generate an ROI of 12.88 to 10.63 (depending upon your tax bracket), it makes sense to pay CG upfront and invest money in such high yield avenues.

Very simple, nice and easy to understand analysis.

Yes, but it all depends on case to case basis. If all the data falls as per the example, then the rates of 12.88 – 10.63 applies. This article is to show what needs to look at before taking any decision.

Hello Sir,

I own a land in Hyderabad purchased in 2003, planning to sell within few months. I am keen to save entire CGT by investing in 54EC bonds. Your article provides useful information on this matter. My specific question is to further clarify “can invest the capital gain amount or the entire sale proceeds”. Do I need to invest the entire sale proceed in 54EC bonds to save entire CG? Or Can I invest only the capital gain amount?

Since you will sell a piece of land, so the entire sale proceeds need to be invested to save LTCG

Very good analysis… One question – After selling property – can we invest part of long term capital gain in NHAI/REC bonds and on remaining amount – pay LTCG tax proportionately ?

Yes

My mother sold a land and there is LTCG incurred:

Is it possible that me or my wife become the first applicant & my mother second while buying Capital Gain Bond (NHAI/REC) and still my mother can claim capital gain exemption?

Very Good advise given I too had sold my property in 2014 after purchasing it in 2005 . I invested in NHAI 54 EC bonds and I had an very good experience with NHAI. I had selected demat form of deposit . Received all interests on time and final interest and principle on the 28 February 2018 .A very pleasant experience with Government of India and National Highways Authority of India NHAI.

THANK YOU NHAI we had good relationship. My citizens of India should be encouraged and feel positive to invest in Government Sponsored schemes . I have had an positive experience with NHAI. Thank You NHAI once More .

VERY NICE explanation , QUESTION IS WHETHER TO INVEST IN CAPITAL BOND @ 5.25% FOR 5 YEARS OR INVEST SAME AMOUNT 25l IN THIS CASE IN fd @ 8.5% (SENIOR CITIZEN) WILL IT NOT GIVE MORE RETURN 20 % tax bracket?

Firstly capital gain bonds are at 5.75% for years. Secondly, you need to understand that if you buy CG bonds then you will invest the Pre-tax amount, and if you go for any other product be it SCSS, then the amount will be Post-tax. Another thing is that SCSS has only 15 lakh of deposit limit.

The example that I shared in my article says that if you fall in 20% tax bracket then your desired ROI from other investments should be higher than 9.46% Post Tax, else you would be better off with CG Bonds

I am getting the house rent n interest from FD

N alsjo I have invested in NHAI BOND FOR FIVE YEARS

WHAT TAX SHOULD I HAVE TO PAY

The bond I have taken towards the selling of land after ten years

What we have understood is, your total income consists of two components- house rent and interest. To know how to calculate the income from house property, you may click on the link below:

https://www.goodmoneying.com/income-house-property-tax-rental-income/

Add interest from bonds and FD to this income and this would be the total income, on which you have to pay your tax.

For a detailed calculation of your taxes, please consult a local chartered accountant.

I wish to know more about saving capital gains through investing in bonds

Capital gain bonds are the eligible financial instruments under section 54EC, in which you can invest the capital gain amount and save yourself from paying any long-term capital gain tax on the sale of the property (whether Residential or Commercial).

Investment has to be made within 6 months from the date of sale. These bonds are issued by NHAI (National Highway Authority of India) and REC (Rural Electrification Corporation) and the maximum amount you can invest is Rs. 50 Lakhs per financial year. There is a lock-in period of 5 years and W.e.f. 1 Aug 2020, the interest rate on these bonds is reduced to 5% p.a., which was previously 5.75% p.a.