This is no longer new information to the investors that since April 1 2023, the taxation of the debt mutual funds have been changed, and now there is no long term capital gain tax advantage available to the debt mutual funds.

This was a big change and has made all the retail investors start thinking on the possible alternatives. Since this change will not impact big corporate investments as in any case most of the big money used to come for less than 1 year time horizon only.

The impact of this change will be more on the Retail investors who buy Debt Mutual funds as an alternative to bank deposits to take advantage of Indexation and reduce the tax outgo. Also, the presence of debt in the overall Asset Allocation makes the portfolio less volatile and suits the risk profile of many investors.

Also read: New Debt Funds Tax Rules: Why to still Continue investing in Debt Mutual funds?

Though the structure of debt mutual funds, due to it being a capital asset, still is beneficial as compared to the traditional bank deposits. But many investors still ask for an alternative.

So this article is to share with you the possible tax efficient alternatives to the debt mutual funds, which may suit your time horizon.

So I have tried to find the products based on Different Investment horizons. Looking at the Rolling Returns , Volatility and Drawdowns

Tax Efficient Alternatives to Debt Mutual funds:

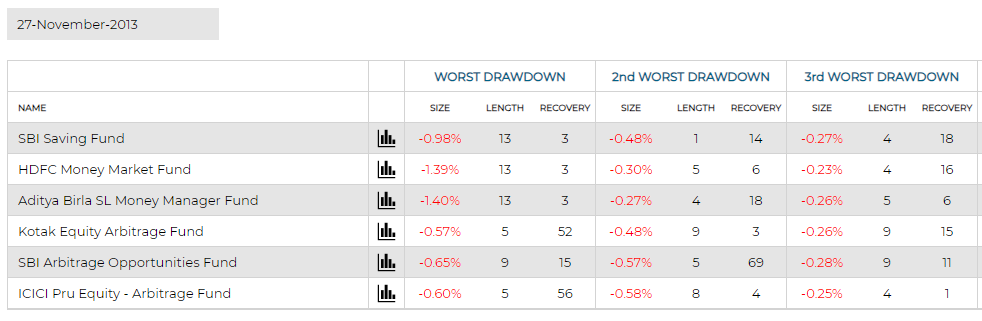

Arbitrage Funds

For very short to short term I have looked at Arbitrage funds

Volatile markets offer more Arbitrage opportunities. Since all the positions are hedged with the derivatives, virtually there is no risk on the Equity Exposure. These funds also take 35% exposure to the debt instruments.

The 65% of equity allocation ( direct and through derivatives), make these funds an equity oriented fund and the taxation thus reduce to that of equity mutual fund, which is 15% on Short Term Capital Gain (less than 1 year holding) and 10% on Long Term Capital Gain (More than 1 year holding)

Also read: All About Taxation of Mutual Funds In India

So taxwise these funds are no doubt attractive vis a vis Debt funds. But the question comes, even though the Risk and Volatility is considered to be low, is it the same or as low as debt funds? And what about the returns?

Check out the below tables showing 1 month, 6 month and 1 year rolling return of the Top Arbitrage funds (AUM Wise) along with the category average, vis a vis there debt counterpart of the specific tenures. For 1 month we have taken Liquid fund, for 6 month Low duration and for 1 year Money Market

Also read: Rolling Returns – A better tool to evaluate Mutual funds

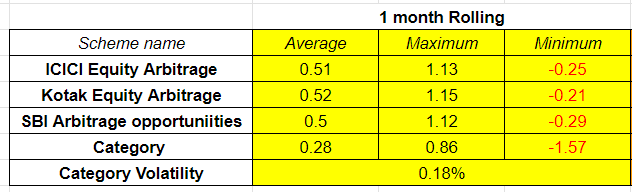

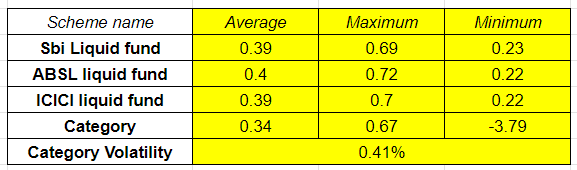

- 1 month Rolling returns of Top Liquid Mutual funds* Vs. Top Arbitrage funds*

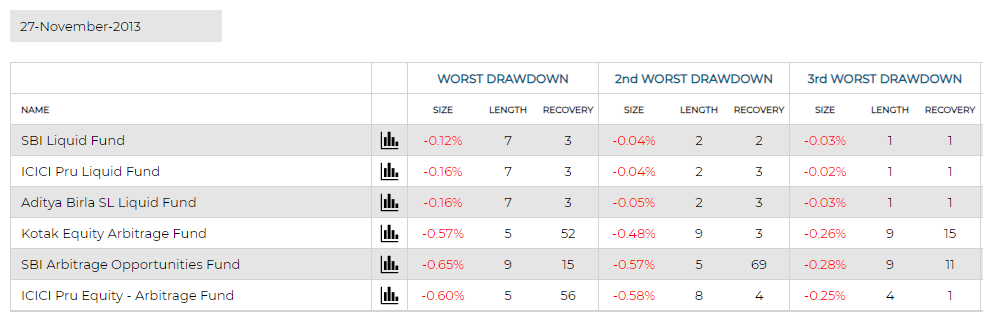

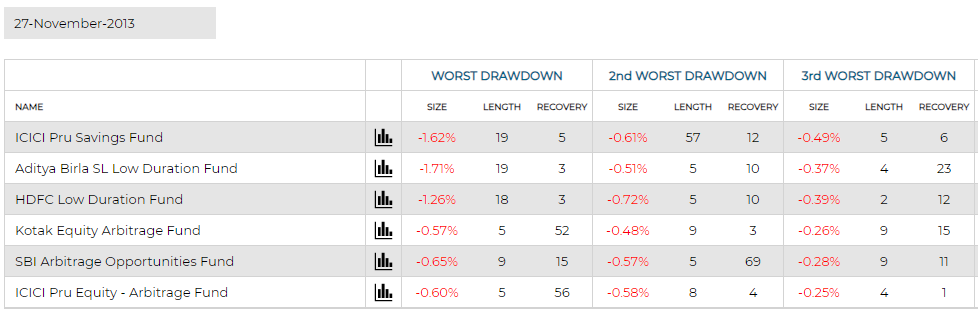

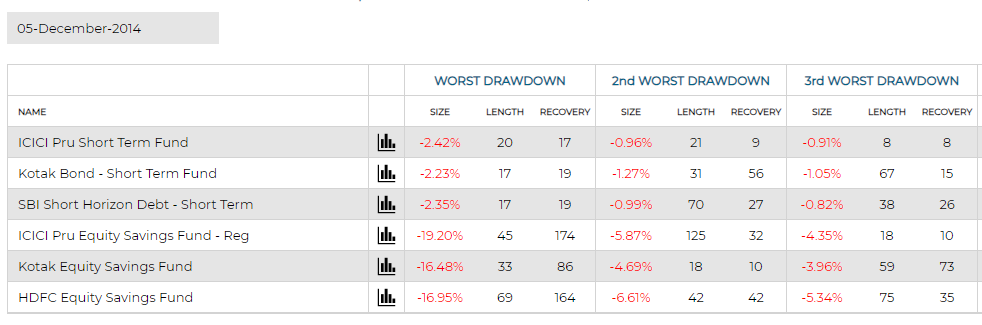

The below table shows the drawdowns in the last 10 year period in these specific funds

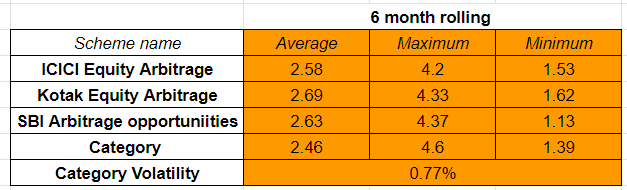

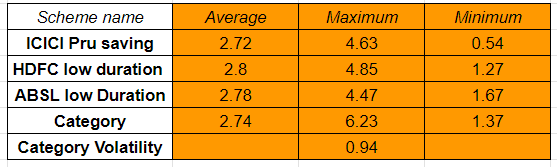

- 6 month Rolling returns of Top Low Duration funds* Vs. Top Arbitrage funds*

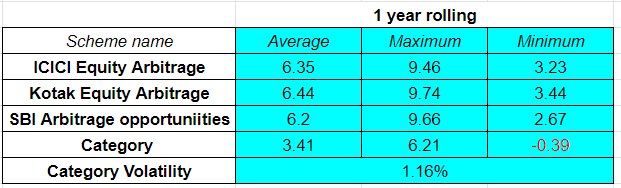

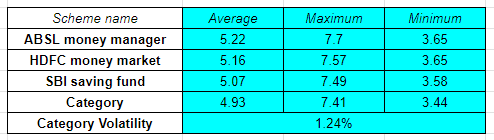

- 1 year Rolling returns of Top Money Market funds* vs Top Arbitrage funds*

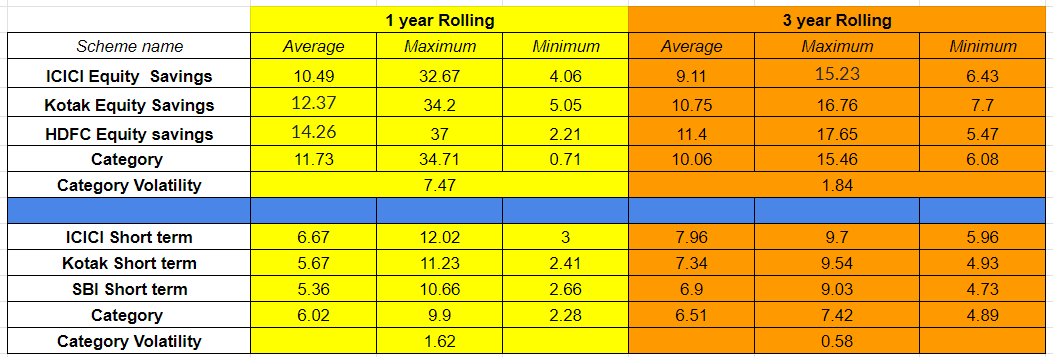

Equity Savings fund

Now let’s look at the Short term to Medium term horizon

One thing is clear that if the concern is to Increase Return then we will have to increase the equity exposure in the portfolio which will further increase the risk, and if the purpose is to reduce the risk then the equity should be cut down.

When we are looking for a tax efficient alternative to debt funds, of course the idea is to have funds with least possible risk, but with tax efficiency and for tax efficiency we have to look out for equity category funds. Still, we may manage some risk through the hybrid category.

For Short to medium term horizon , I have only one option, i.e. Equity savings Fund

What is an Equity Savings fund?

Equity savings funds are a mix of Equity, debt and Arbitrage. Due to the presence of Arbitrage Strategies, this fund looks to exploit the pricing inefficiencies in the cash and derivatives segments of the equity market. Also, this will result in some hedging in the portfolio.

ESFs also keep around 30-35% of pure equity exposure, and the same exposure is of Debt and Arbitrage. Thus, the fund’s overall equity exposure is partially hedged, partially into debt, and this mix makes it a tax efficient alternative to pure debt funds, for short to medium tenure

Below table shows how Top Equity savings Fund and the comparable debt schemes (tenure wise), have performed lately

In the above table, you may find better returns in Equity savings fund, but do also look at the category volatility, which is quite high in ESFs vs. Short term debt funds. Of course, you may say that you are a long term investor, but to have a better understanding on the risk look at the Drawdown table below.

Fall in the debt funds will not bother you much as this will not impact the portfolio in a big way, but 15-20% fall in equity savings funds will surely hit the investments hard.

So, you have to be clear on this front as to what you are going to earn and with what risk. I would like to share one article on risk

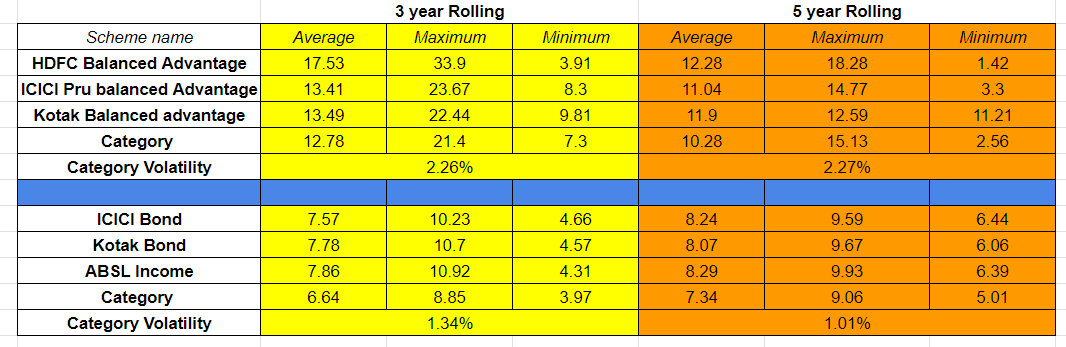

Balanced Advantage Fund

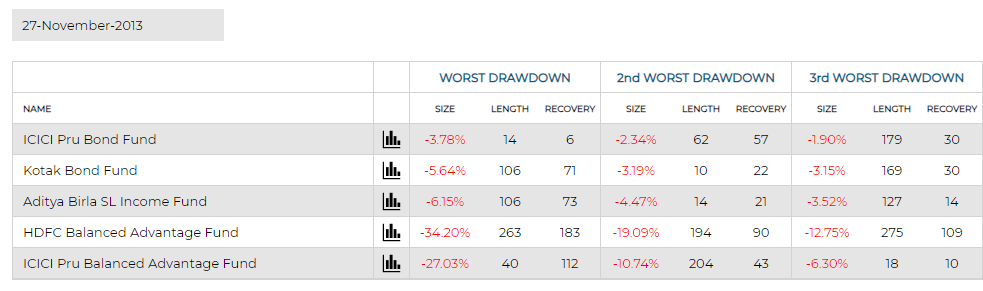

Let’s look at the 3 year plus kind of horizon, with Balanced Advantage fund category

You must be thinking why am I comparing BAF and not an aggressive Hybrid fund. The only reason for this is that we are not looking for aggression and just tax efficiency, and are happy with debt kind of return with least possible risk in different tenures.

But practically it is not possible, as tax efficiency only comes in equity oriented portfolios and when you add more equity, the returns will get pushed and so does the risk and volatility.

Also read: Balanced Advantage Funds vs. Multi-Asset Funds: Which one is better?

Also read: Balanced Advantage Funds vs. Balanced Funds

Here also we will check the Rolling Returns, Volatility and Drawdowns of Top Balanced advantage funds with Medium to long term bond funds

Drawdown Chart

Here again, you need to be aware of the volatility this may bring to your portfolio. Though longer the horizon and more averaging of purchase through SIPs may reduce the impact of drawdowns. But still I am more concerned about the reason you give to yourself for accepting the same.

Tax efficient Alternative to Debt Mutual funds for a very long term horizon

You may also say that your horizon is not 1 or 5 years. You have a very long term view and are saving for your Retirement which could be 15-20 years away. Is there any tax efficient alternative to debt mutual funds? Since the longer the time frame higher would be the corpus of the investments and with this new taxation of debt funds, the complete capital gain will be added to your income and increase the taxation at the time of withdrawal.

To answer this, you may add the very long term products in your portfolio like PPF, VPF ( for salaried ) and even NPS with debt allocation only can be good tax efficient alternatives to debt mutual funds.

PPF and VPF (Voluntary Provident Fund) are well known products offering tax free returns to the investors (up to a specific limit of Investment). NPS also offers 60% tax free return, and with the introduction of the SWP feature, this has become very attractive from the Retirement savings angle.

Conclusion

One thing you need to ask yourself is WHY are you seeking a Tax Efficient alternative to Debt Mutual fund? And also why do you call yourself a long term investor? Is it because of goals, or low returns in comparison to equity funds or change in taxation of debt funds?

What I mean is that in many discussions with investors I have found that their reason behind this search is not tax efficiency which definitely would be a by-product, but high returns in these bullish times. In the recent past the returns in equity products are looking mouth watering and every short to medium term investor just to increase equity exposure have started calling themselves long term investor, and are ready to accept risk.

But such investors run first in the falling times, as was seen in 2008 as well as in covid fall.

So don’t give justification to your greed. Ask yourself , speak to your advisors, will you be able to handle the volatility and take the pain of market fall, in search of this tax efficiency. If yes, you have the alternatives available but if not (which you may not even understand today), better to stay away and continue with the debt funds which are not that bad if you understand its structure properly.

– Infographics")

{kind=link}

Sir Ji, why did you leave out moderate hybrid funds (>30, <65 % equity) – that can be redeemed after 3 years with indexation benefit?

You are right. There are some balanced hybrid funds (though not much in numbers) which satisfies the new indexation tax rules. But these funds are not much in numbers and mostly are “Solution Oriented” kind of schemes…so ignored for this article.