When Ankur started his first job, on the advice of one of his colleagues he bought one LIC endowment plan. The basic purpose of buying that plan was to save tax and also some investment for long term.

Now after few years when he was reviewing his investments, he was not sure if he’s invested in the right product or not. His tax saving is being taken care of by his EPF contribution and Home loan premiums, thus, this policy does not contribute to any tax saving investments. Neither this policy suits him from Insurance perspective; since he feels that insurance cover is minuscule as compared to his requirement.

His confusion was from the Investment perspective angle. He was told at the time of investment that it would give him some guaranteed and safe returns and will make his money double on maturity. Now this statement is still in his mind, which is a reason for confusion that “Should he surrender LIC Policy or not?”

You also must have some Endowment policies with you, which actually are being serviced from Investment planning angle only. But are they worth continuing? Did you ever evaluate them, as to if they are actually serving the purpose and generating enough returns or expected to generate enough returns as per your expectations? Would surrendering the policy and investing the proceeds somewhere else be wiser or you should continue with the plan as it is, until maturity.

Let’s try and answer the question Should you surrender LIC Policy, by taking an example of LIC Jeevan Anand.

(Also Read: Is the claim settlement ratio really important while selecting life insurance policy?)

Mostly endowment plans work in a similar way. You invest a calculated premium which is based on your Age, sum assured and term opted for, and on maturity, you will get Sum Assured plus all vested simple reversionary bonus plus final additional bonus (If any). These bonuses depend on the performance of Corporation and distributed as per management’s discretion, and it’s not guaranteed.

While evaluating the policy, you need to have following details with you:

- Your policy Surrender value ( with all vested bonuses)

- Term left before maturity

- Expected maturity value of your product ( As per past bonuses)

- Alternate product where you’ll invest the surrender value

- Expected Returns from that product.

To Surrender LIC Policy or not – Let’s understand this with two real-life cases:

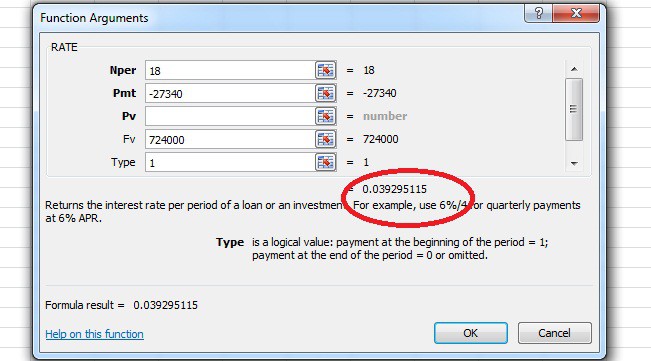

Gaurav (name changed) bought LIC Jeevan Anand for a Sum assured of Rs 400000, with an annual premium of Rs 27340. The policy was started in Sept 2013, till date he’s paid 3 premiums (Policy is in 3rd Year). Premium paying term is 18 years, and policy term is 61 years.

He wanted to review the Policy from an Investment perspective as he got a decent Life insurance cover from Term Plan. He wants to know if he surrender LIC policy or continues with it.

How to get LIC policy surrender value?

Lic policies (endowment) attains surrender value only after payment of at least 3 annual premiums. It comes in 2 forms – Guaranteed surrender value and Special Surrender value. Surrender value factors are mentioned in policy feature details which help in getting tentative Idea, but it’s better to have an exact calculation in place by asking for Surrender quote from the LIC Office.

As per LIC Jeevan Anand surrender value terms – “The policy may be surrendered after it has been in force for 3 years or more. The guaranteed surrender value is 30% of the basic premiums paid excluding the first year’s premium. Any extra premium(s) paid and premium(s) towards Accident Benefit are also excluded. In practice, the Corporation will pay a Special Surrender Value – which is either equal to or more than the Guaranteed Surrender Value.”

Gaurav enquired about surrender quotes from LIC office, but he could not get any since the policy is yet to complete 3 years. Before 3 years, endowment plans don’t generate any surrender value. So we considered the value as ZERO for our analysis.

(Also Read: Tax implications when you discontinue life insurance policy)

How to calculate the maturity value of LIC Jeevan Anand?

As per the policy features, Survival benefit would be Sum assured together with an accrued bonus.

To get the expected maturity value of the plan, we used the bonus data as available on the insurer’s website. http://www.licindia.in/Customer-Services/Bonus-Information . As per these details, the bonus declared in LIC Jeevan Anand (for 18 years term policy) in past 3 years was in the range of 44-45 per thousand. Thus, what the policy has been earning in the form of the bonus was Rs 18000 per year, and it’s assumed that same will continue in future too.

This means on maturity what he can expect to get was Rs 400000 (Sum assured) + Rs 18000*18 (Simple Reversionary bonus for 18 years term). Total comes out to be Rs 724000.

By calculating the maturity amount with Premium payments, annual returns come out to be 3.92%.

Of course looking at annual returns, continuing the plan does not make sense, but still to decide on to surrender LIC policy, one needs to look at the alternative available and expected returns from the same.

In this case, there’s no surrender value available, so whatever has paid is a total loss at this moment. But forgetting that if Gaurav starts investing the annual premium in some Hybrid fund with the expectation of 10% per annum return, then after 15 years he’d be having Rs 9.55 lakh. Even @8% he will have Rs 8 lakh with him.

So it makes more sense for Gaurav to forget Rs 82020 paid as premiums till date and divert the annual savings to a better product.

Case 2 – LIC Jeevan Anand

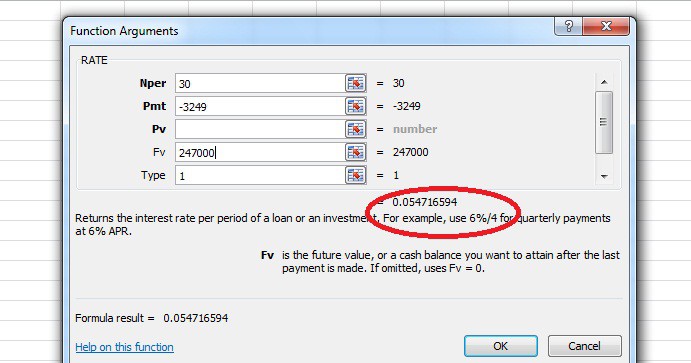

Annual Premium – Rs 3249

Sum Assured – Rs 100000

Premium Paid – 16

Premium paying term – 30 years

Policy Term – 80 years

Surrender value as per Surrender quote is Rs 36713/-. Total Premium paid till now is Rs 51984/-.

Expected maturity value at 48-49 per thousand bonus as per http://www.licindia.in/Customer-Services/Bonus-Information, comes out to be Rs 247000 ( Rs 1 lakh SA plus Rs 1.47 lakh Bonus). This brings the annual return to 5.47%

Now again, if you look just at percentage return then you may feel that one should be out of such product. But we need to look at the other side too, as what if we surrender and invest the surrender value and future premiums in a product which is expected to generate 8-10% of the annual return.

In this case, if we invest Rs 36713 and future annual premiums of Rs 3249, somewhere for 14 years term then @10% maturity value would be Rs 239397/-, lesser than what is expected from the policy itself.

So in this case mathematically, surrendering the plan may not make much of difference.

Should you surrender LIC Policy?

They say buying life insurance contract is a long-term commitment and should not be looked at from short-term viewpoint. I totally agree with the statement and this is why buying the same and continuing the same needs to be supported by long-term requirements and inflation rate.

(Read: Were you sold what was told?)

“WHY” is very important to answer before getting into any policy. If it is for Insurance then it should be having decent insurance coverage, enough for your financial dependents in case any eventuality strikes. If the purpose is an investment, then the expected return should beat inflation and generate some positive real returns.

This needs to be considered every time you review your investments. Sometimes, you have every reason to buy that product in the beginning, but over a period of time, it may not fit into your overall requirement and financial plan. So rather than clinging to it with a point of view of losing money if surrendered, it needs to be reviewed in detail – feature-wise and requirement-wise.

Every product you have should fit into the Big picture and help you achieve your financial goals comfortably. LIC policies are something which one feels comfortable to continue with, but when in the review it looks like a complete waste of money, then it’s wise to surrender the same and move ahead with better suitable products.

How to Surrender LIC Policy?

- Visit the LIC Branch Office with the Policy bond. I have experienced that only the branch from where the policy was bought is to be visited for this purpose s no other branch will entertain this request.

- Ask for the surrender form or you may Download-LIC-Policy-Surrender-Form-No.5074 form from here. The formats keep on changing, so it is better to ask the form from the branch itself.

- To surrender LIC Policy you also have to submit the Photo ID proof like aadhar card or Pan card, along with a canceled cheque copy having your name printed on it.

- On completion of formalities, the money will be credited to your account in 7-10 days time.

Hope you find the article on surrender LIC policy useful. Do share your comments and questions in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

My Life insurance was about to mature in dec 2019 of 51,000. My agent made me take a new insurance policy of 67,000 annual premium and said you don’t have to pay in first year as you are getting the maturity amount. But I got 83000 in total and the policy is showing discounted claim .How much I lost he claimed the amount in June instead of Dec.

You may not have not lost anything. It seems that the amount has been transferred to some new policy. Better to check it with the LIC office or your agent to get all the details.

If i will not pay my lic premium three time in a row so what will happen to my policy?

It all depends upon how many premium installments you have actually paid. Generally, after paying three premiums policy attains a paid up value. Rest, you may read the policy conditions or confirm it from LIC directly.

hi,

I have taken 1 Cr insurance policy for me and my wife and payming approx. 350000 x 2=700000 premium for the last 3 years. Now I want to stop how much will I get from LIC?

You have to check from the insurance company directly and get the surrender quote.

If I go to LIC office to surrender my policy,will they complete all the formalities in 3 hours or they will ask me to come some other day? Please help me.

It would be wise to call them first and ask them what all documents are required before visiting LIC office, so that they can complete the work in your limited time schedule

I have LIC policy, I want to Silander my LIC policy how much get the money

Please check with LIC directly.

I have taken lic policy in 3/7/2014 . Policy plan 815. Term 25

Total Premium rs 9038 hly

I want to know how much money will be given to me after 25 yrs.

Is it profitable or not.?

Please check with LIC directly.

Regarding surrender value

My lic premium is 108000 yearly completed 3 year’s so why i am not get my whole amount back after all that is my amount na

Sir, you need to check with your local LIC office or your LIC agent.

I have a jeevan saathi policy which i have been paying since December 2010. Annual payment is around 29k. I would like to surrender it now…

What would be the amount I receive?

Will I receive the bonus whicj has incurred on my policy

It depends upon the policy terms and conditions. Read the policy document, contact local LIC office and ask for the surrender quote.

You have mentioned the IRR of the policy as 7.83%. Not sure, how you calculated it, but actually if it is so,then it is a good rate of return and there is no harm in continuing it provided, you do not have any goals coming up in near future and funds are locked in in this product.

From product point of view, it is good, but from financial planning point of view consult a financial planner.

It’s about Jeevan Anand policy, which I took 10 years back, I confused to continue or surrender? IRR is 7.83 percent. Maturity value is also E E E CATAGORY.

What Ii will do , to continue or surrender

I have lic policy.is it good to stop lic policies

It depends upon your Financial Plan and the Goals you are targeting. A holistic look at your finances is required to assess whether the product fits somewhere in the financial Structure or not.

I have jeevan sarala policy,it have 6 years pass but I want to surrender now what I take from it

Please visit your nearest LIC office and get the surrender quote.

I BOUGHT JEEVAN LABH IN FEB 2018 AND PAID SECOND PREMIUM ALSO. NOW I FIND IT A WASTE AS It gives low returns . iam 43 now and got for 21 years . i did not know about the low returns.

should i pay 3rd premium or forego 60k i want to know , since i will be getting only 45k.

From the returns point of view, you are correct. These policies do not yield much, so it doesn’t make sense to continue them.

But from the financial planning perspective,it depends upon your Financial Plan and the Goals you are targeting. A holistic look at your finances is required to assess whether the product fits somewhere in the financial Structure or not.

I have bought new endowment plan from lic. N have been paying premium for 5 years. But now I feel there r better plans n I want to surrender…bcoz I pay 80k elvery year. N paying term is 20 yrs but I will get only 27L on maturity. So I want to surrender n wish to invest n plans like sanxhay plus. But i have invested 80k for 5 yrs…so I want to know what I will loose in lic if I surrender

Please visit your nearest LIC office or your LIC agent and get the surrender quote of your policy to know the surrender value. Also you mentioned that you want to invest in Sanchay Plus, we have reviewed this product, you may go through link below for the detailed review analysis:

https://www.goodmoneying.com/hdfc-life-sanchay-plus-review/

I had paid 3 year’s premium of jeevan anand lic policy 5828 premium and sum assured is 1 lac how much i will get back

Please visit your nearest LIC office or your LIC agent and get the surrender quote of your policy to know the surrender value.

I started Lic’s Jeevan Labh in 12/04/2017.i want to withdraw my amount because of my health problems. How to withdraw my amount

You have to visit your nearest LIC office or contact your LIC agent and ask for the surrender quote of the policy.

I want to surrender jeevan anand and jeevan saral policies, policy i started in 2011 and i am paying 48000 rs. Yearly for both

Can you please tell me how much i can get if i surrender my both policies

Please visit your nearest LIC office or your LIC agent and get the surrender quote of your policy to know the surrender value.

I start LIC in December 2017 what will happen if I will stop paying premium

“Please visit your nearest LIC office or your LIC agent”

apart from above quote what you suggest us how much amount we get if surrender the policy after 5 years?

It all depends upon how many premium installments you have actually paid. Generally, after paying three premiums policy attains a paid up value. Rest, you may read the policy conditions or confirm it from LIC directly.

Actually I am facing shortage of money.I am trying to gather money from all available sources.Presently, I have two LIC policies Jeevan Shri and Jeevan Saral….

I am not able to decide whether it would be a wise decision to surrender the LIC policy

It depends upon your Financial Plan and the Goals you are targeting. A holistic look at your finances is required to assess whether the product fits somewhere in the financial Structure or not.

LIC Jeevan Anand policy – can I surrender now?

Policy Tenure 35 yrs. Till now I paid for 12 yrs.

Yes, as per the policy terms, the policy can be surrendered any time after completion of 3 years. You may visit the link below for details:

https://licindia.in/Products/Withdrawn-Plans/Jeevan-Anand/benefit

Really, I enjoy your site with effective and useful information.

Want to surrender my policy which is get matured in next 4 years , so is it feasible to surrender it

We are really not sure about which policy are you referring to. First, we have to understand the product and then a holistic look at your finances is required to assess whether the product fits somewhere in the financial Structure or not, according to your financial goals and other requirements.

If the policy term of lic endowment plan is 10 years and i surrender policy after 6 years then why i am getting money less than premium however i have invested my premium for 6 years by single payment.

I have taken Jeevan Anand poliy in 2011 with Annual premium of 55k, Premium paying term =25 and Sum Assured =20 lac, IF i will surrender this poliy. What wil be the surrendered value?

The surrender value of the policy would depend upon the fund value accumulated and the bonus rates which are prevailing for this policy.

Please visit your nearest LIC office or contact your LIC Agent and get the surrender quote to know the surrender value.

I am paying lic jeevan anand policy for last 44 months every month 40000 how much i get if i surrender

The surrender value of the policy would depend upon the fund value accumulated and the bonus rates which are prevailing for this policy.

Please visit your nearest LIC office or contact your LIC Agent and get the surrender quote to know the surrender value.

I have taken LIC policy “The Endowment Assurance Policy (Plan-14)”

Start Date: 11/11/2006

Maturity Date 11/11/2026

Yearly Premium Rs 24718

I stopped paying the premium after 11/05/2015 as realized it is not giving proper coverage. So took Term Insurance for 1 crore.

Now i can see policy is Paid Up and was waiting for maturity date. Because of covid, i am in financial trouble and need to withdraw money.

Any rough estimate how much money i will get.

Total amount paid till now -> 210086

Bonus, Guaranteed Addition₹ 1,78,500 (As per LIC website)

Please help with your knowledge whether i will get money which i invested i.e. Rs 2 lakh 10 thousand

Hi Amit,

As per our knowledge, you should receive the paid-up value of the policy, as applicable.

I have a LIC policy with sum assured being 5 Lakhs and the term being 35 years (paying 6125/- quarterly) which I took in June 2011. My query is what if I surrender the policy after 10 years ie if I surrender in June 2021

Please contact your nearest LIC office branch or your LIC Agent and ask for the surrender quote of your policy.

Hello

I have an LIC Jeevan Saral(with profits) policy- Table-165, term 20 years starting from April 2012 with assured maturity sum of 1205550/. I have been paying all premiums without a single break till date. Total premium paid till now-( 60650×8=485200/.)Now I want to surrender this policy this year. Can you please help me to know what will be the value I will get back after surrender.

Thankyou

This is something you would be provided by the LIC Branch office or your LIC Agent. Please contact your LIC Agent or visit the nearest LIC office and get the surrender quote.

till date I have paid my lic policy for 56 months. base premium is 1489 if I surrender my policy can I get the bonus amount?

It depends upon the type of plan you have. It may be possible that some portion of the bonus in the accumulated surrender value if the policy document says so. Please visit your nearest LIC office or contact your LIC Agent for details.

Sir isn’t the maturity value= Sum Assured + Revisionary Bonus + Final Bonus. For the above calculations of Endowment Plan you haven’t considered the Final Bonus, shouldn’t that also be factored in?

In the calculation, we have taken the bonus rates as shared on the LIC website at the time of writing this post. The final bonus figure is not fixed. It may or may not be received. If received then it would be an additional benefit and improve the IRR a bit.

: I want to surrender the Komal Jeevan policy with a Policy paying term of 18 years and the maturity term of 26 years. I had made an uninterrupted payment for 15 years and have stopped the payment since the last 2 years. Ami I eligible to get the bonus accurued during this time frame ?

You are surrendering the policy in-between the premium paying term. So, as far as we know, you are eligible for the policy’s surrender value only. Please confirm the same with the LIC branch office or your LIC Agent.

Hello Sir

Recently I bought an endowment plan called LIC Jeevan Labh for a monthly premium of 6300/-, the policy term is for 15 years and it matures on the 21st year. The LIC agent sold this product by saying that the investment would be doubled at the end of maturity. Without giving a thought I have enrolled into this plan and later got a chance to understand the details of this plan and its benefits. After analysis, I found that this plan does not worth of investing 75k per year and continuing the same for next 15 years. Therefore, I felt it is not wise to invest in this product for long term benefits. Now I have paid 6 months premium, so is it possible to surrender the policy or should I forget about the 36k I have paid so far ? Kindly need your suggestion.

Hi Karthik,

As per the policy terms & conditions, the policy would not generate any surrender value before two-year premium payments. Please go through the fine print of the policy document. I am attaching the link to the policy document on the LIC website.

https://licindia.in/getattachment/Products/Insurance-Plan/Jeevan-Labh/Final-Policy-Doc_-LIC-s-Jeevan-Labh.pdf.aspx