Sonali bought a Unit linked insurance policy (ULIP), in December last year to save taxes. It was a last minute purchase so she did not inquire much about this product. It was easy for the bank’s relationship manager, she has her account with, to persuade her to buy this product. Her main requirement was only Tax saving at that moment.

Now as one year has passed and she’s being reminded of the next premium payment she’s trying to understand how this insurance product works and how does she be benefitted out of it besides Income tax savings. After googling around and reading out few articles on why insurance should be bought and why ULIP should be avoided, she’s repenting on her last year mistake and wants to discontinue life insurance policy by stop paying the premiums and later surrender the policy.

Almost same thing happened with Ravinder, who took Voluntary Retirement last year. His old friend who also happened to be an Insurance agent convinced him for ULIP policy from the part of the Retirement benefits he’d received. Now after a year when Ravinder realizes that he should have worked on his requirement first and should have planned for his retirement income, he’s finding it difficult to continue with the ULIP payments and wants to discontinue the same.

In both the cases where it may make sense to discontinue life insurance policy, it is also important to understand the tax implications on discontinuance of Life Insurance. This will help in making the wise decision.

Discontinuance feature has been standardized in ULIP policies and now investor should not be worried on deduction of heavy charges.

Unlike earlier wherein many ULIP policies, first premium gets forfeited if one doesn’t continue with the premiums, now the things are different. Nowadays there are some standardized discontinuation charges which would be deducted from the Fund value and then the balance amount would get moved to a discontinued fund, where the fund will earn saving bank interest rate. After the completion of the basic lock-in period which is usually 5 year, the fund value will get paid back to the policy owner.

But when you have to decide onto discontinuation, you also have to consider the taxation aspect, which is as follows.

Tax implications when you discontinue life insurance policy

In Life insurance policies taxation is involved at 2 steps – one at the time of Premium payment which comes under section 80C, and the other one is under section 10(10d), which makes the maturity proceeds tax-free if the sum assured is at least 10 times of the Premium amount.

When you discontinue life insurance policy by stop paying premiums, then the sum assured (Death benefit) attached with the policy gets lapsed, which means that policy will cancel any Insurance cover attached. Thus, at the time of claiming the money back while surrendering the policy, it will not be satisfying the condition of 10(10d) and this makes the policy proceeds taxable.

Insurance policy’s proceeds neither come under category of “Interest”, not under “capital gain”, so whatever proceeds you get on surrender becomes 100% taxable. Yes, including the capital invested.

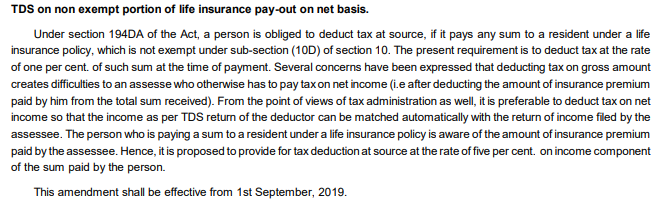

With the clarification issued in Budget 2019, only the gain amount i.e. proceeds after deduction of the premium payment is taxable. Below is the excerpt from the memorandum of Budget 2019.

To make people understand the taxation and also to ensure the tax collection, from October 2014 Government has made mandatory for Insurance companies’ to deduct TDS @ 5% on taxable surrender proceeds. In case of NRIs, TDS rate is at highest marginal rate i.e. @30%.

Let’s understand this with an example of Sonali:

She bought one ULIP in December 2014 for an annual premium of Rs 1.50 lakh. She falls in the highest tax slab i.e.@ 30%. If she discontinues life insurance policy premiums from 2015, then the fund value as on date would be transferred to discontinued fund account after deduction of some charges. In that account, she would be getting an Interest equal to the savings bank rate.

As the minimum lock-in period of her policy is 5 years, so in 2019 when she gets her policy surrendered and whatever be the fund value at that time…let’s assume as Rs 1.75 lakh, will get added in her total income and taxed accordingly. Only Rs 25000 will be taxable and added in the total income of Sonali. Means in Sonali’s case she will have to pay a tax of around Rs 52500 on surrender.

Tax implications on Policy issued before 1 April 2012

Earlier to April 2012, the minimum insurance cover to qualify under section 10(10)d, was 5 times of premium payment and there used to be no standard Discontinuation clause. Every plan works in different way, with terms mentioned in the Policy document.

In some policies same insurance cover continues even after discontinuation of premium, in some it gets reduced. Some policies did allow Top up on Premiums but don’t provide proportionate 5 times cover on that amount.

Tax implications if you discontinue life insurance policy remain the same as mentioned above if it does not satisfy the minimum Insurance clause under section 10(10)d. So if you have any old policy which was discontinued due to any reason, do check out the latest sum assured position before surrendering.

Should you discontinue your Life Insurance Policy?

Now this is a difficult one to answer. You are in a catch 22 situation. If you continue with the premium payments you would be losing on allocation, administration and mortality charges, along with the opportunity that you may earn better by putting money somewhere else.

But if you discontinue life insurance policy, then you may be making the proceeds taxable,

So the decision to continue or discontinue life insurance insurance policy varies with case to case. It will depend on the number of premiums you have paid, charges associated with the policy and Income tax bracket you fall into. Comparative analysis has to be made at that moment to make a wiser financial decision.

Conclusion:

First thing first you should not invest in any product without understanding how it works and where the investments get fit into your requirement. But if you’ve already invested and now planning to discontinue the premium payments, you should check out the tax implications on discontinuance of your life insurance policy, before making the final decision.

Did you find the article- Tax Implications when you Discontinue life insurance policy, useful? Do share your opinions in the comments section.

Disclaimer: I am not an Income tax expert. The Information shared in the article and the comments below are to the best of my understanding, from different sources, articles, and discussions with other experts on this subject. Before acting on any of the statements, do consult a tax professional.

– Infographics")

{kind=link}

I have read somewhere that there won’t be any tax liability if we discontinue the policy that have been paid for more than 5 years, am I right??

Dear Manikaran, The information is quite elaborate and an eye opener.There is no use t cry over spilt milk.”Main yeh bhool ta umar karta raha; dhool chehrey par thee par main aena saaf karta raha”. Thanks.

Thanks sir.

I had surrendered a policy Exide Life New Best Years Plan before maturity date and received the surrendered value credited to my bank. However no TDS was applied. I wanted know the tax liability on this amount and M/s Exide Life has informed that Exide Life New Best Years Plan is a pension plan. Hence, there is no TDS (Tax Deducted at Source) applicable to this policy.

I would like to know whether the amount which I have received should be included with my taxable income or not.

Exide people are correct. Pension plans are not subject to TDS. But the complete proceeds you have received is taxable , so you need to add it in your total income of the year of surrender.

If we read the contents of circular7/2003 issued by CBDT then does it not mean that the proceeds in excess of premium paid should be taxable.

See, its about interpretation. There is no Court case, Applette Tribunal decision on such a case. I am not a tax expert and whatever I have written is only as per my discussion with other financial planning professionals, and reading other articles on this topic. If any Tax professionals want to keep 7/2003 as a base and help the clients save on taxes, then it would be as per his/her interpretation.

This is to continue today’s chat with you Sum assured in case of both policies is Rs,3,50,000 each and annual premium Rs. 50,000/-. each . (ICICI Pru guaranteed Savings Insurance Plan policies taken in No. 2011 and surrender after lock in period of 07 years during this financial year. Both policy holder and proposer are senior citizen

Great, well explained and very comprehensive information about ULIP surrender.

Thanks