Claim settlement ratio has become a parameter of the integrity of the Insurer. People look down on the insurer having a low ratio. Every new buyer would like to go with the insurer having high Claim settlement ratio. The high ratio also has become a point of marketing for insurance companies and you can see insurers displaying and boasting of their high Claim settlement ratios in their advertisement.

But the question is what is there in this claim settlement ratio, which has become a deciding factor while selecting an Insurance policy? Why is this ratio so important and should one really decide their purchase based on this ratio? Let’s figure this out.

What is claim settlement ratio?

Claim settlement ratio in simple terms means the number of Claims paid by the Insurer against the claims received. If a Company has received 100 claims, out of which 90 has been paid, then the claim settlement ratio is 90%.

Out of remaining 10%, some claims may have been rejected by the company due to some reasons, which brings us to Claim Repudiation or Rejection ratio, and the balance is Claims pending ratio. Say e.g 3 claims have been rejected, and 7 claims are in pending status. So the claim repudiation ratio would be 3% and Claim pending ratio is 7%.

Now if you look at one side of the story, then yes high claim ratio looks satisfying to the eye and it may let you assume that this insurer may not reject your claim and your family will not have to run from pillar to post to get the life insurance claim. But if it is all about data then there are other ways too to look at the numbers.

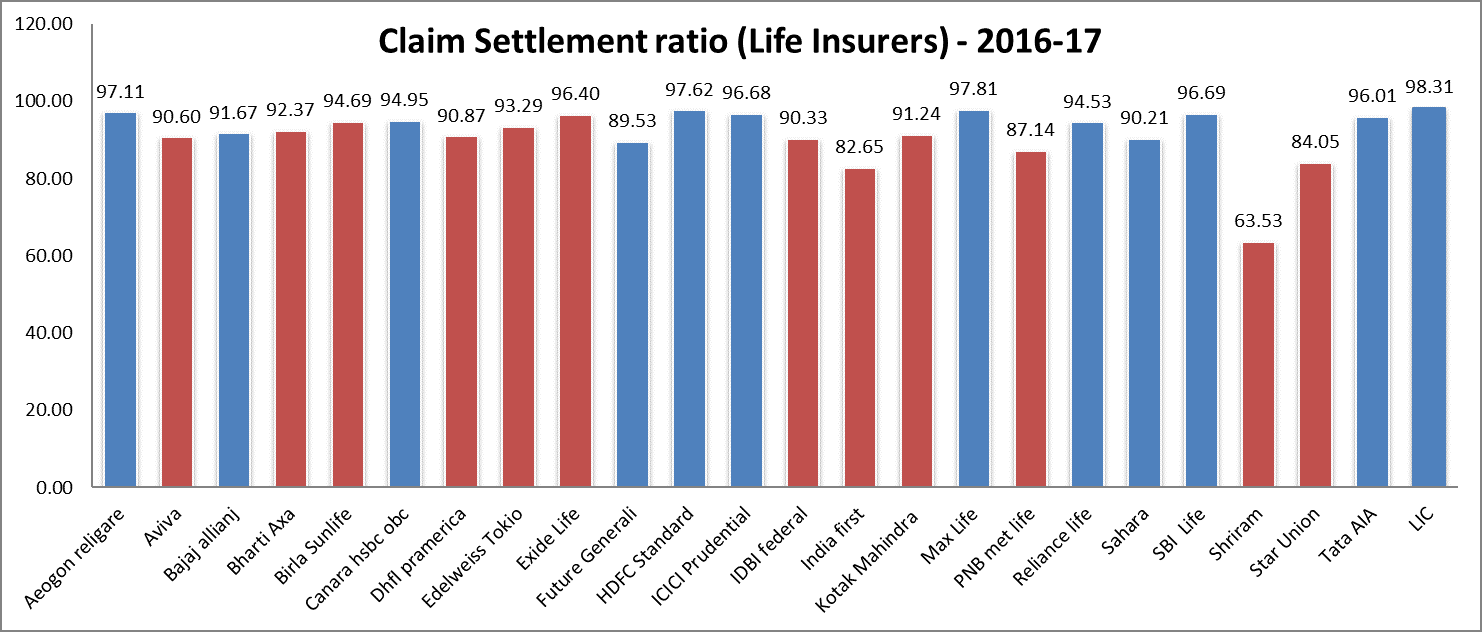

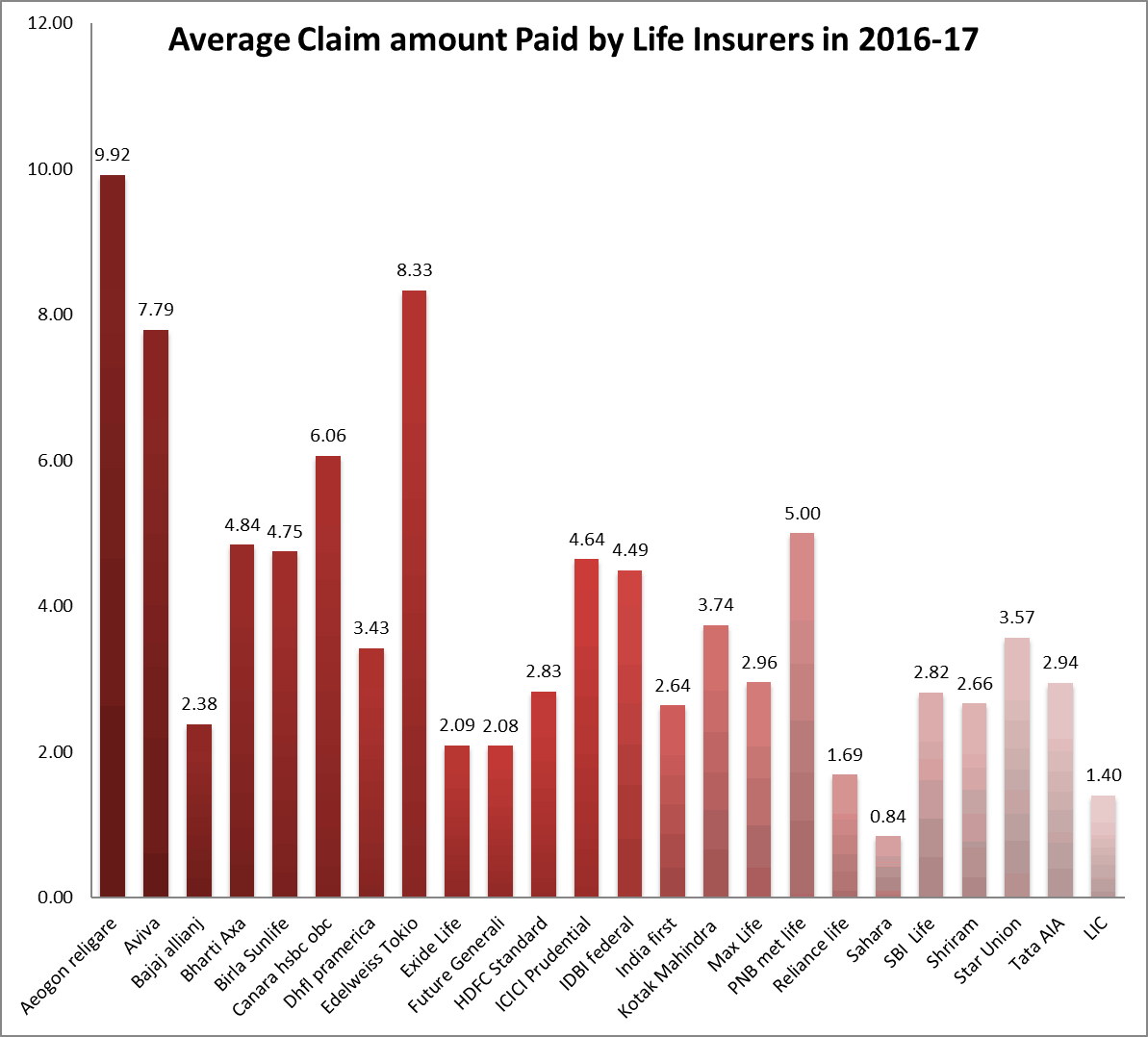

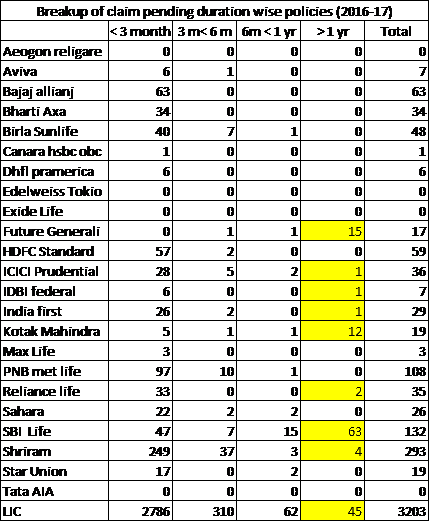

As per the 2016-17 data, LIC the most trusted Brand among the public has rejected 7432 claims with an average claim amount of Rs 2.02 lakh. 2786 claims were pending with a delay of about 3 months by the end of FY 2017. However, the Claim settlement ratio of LIC in 2016-17 was 98.31% and the average claim amount was Rs 1.29 lakh. ( Read: Should you surrender your LIC policy?)

Not sure what you construe from the above statement. It all depends on what you want to read and also on your understanding of numbers. If you just look at 98.33% then yes, LIC has high claim settlement ratio, but this may be due to the fact that the average claim paid was hardly 1.40 lakh.

On the other side, 7432 number of claims are also not less, why were they rejected? 2700+ claims were not settled in 3 months’ time.

Let’s have a look at other companies’ numbers

19 Companies have more than 90% of claim settlement ratio.

Now let’s look at the average claim amount paid by these insurers in respective financial year

Why should Claim settlement Ratio not be the only factor to consider while buying Insurance Policy?

Though the claim settlement ratio tells how many claims a company has settled in a particular year, it does not tell why the other claims have been rejected or lying pending with them.

It’s easy to find fault in some insurance companies based on these numbers, but the reason for rejection could be fraud committed by the Insured, misrepresentation of facts while buying a policy, non-disclosure of facts. And the delay also could be on the part of insured’s nominees while submitting the required documents.

The above data also does not tell the composition of claims, as to what type of policies have been claimed. Whether endowment, ULIPs or Term plans. Looking at the average claim amount it may be interpreted that the policies could be investment-linked and not the term plans with high cover.

The data does not even tell that how many claims are early claims, means that came within 2 years of buying the policy and looked at with suspicion by the Insurer and for which investigations are going on.

These days with the spread of financial literacy and coming down of the insurance costs, people are preferring term insurance plans with high-value cover. For such claims, the Insurance company wants to satisfy itself that the claim is genuine so may take some time in the investigation, which may not be the case with low-value covers as with endowment plans.

A company which prefers selling more of term plans thus may be reflecting a low claim ratio or high pending cases with them. (Read: Online Term PLan with Income benefits – Does that make sense?)

I mean there could be many Ifs and Buts when your deciding factor is only these claim settlement ratio numbers. High claim ratio does not mean that your high-value claim will be passed with ease.

To make it easy for your nominees claim the insurance money, you have to be true with your insurance company, by disclosing all the material facts while buying the policy.

If there is no misrepresentation, No concealment of material fact and No Fraud from insured’s end, No Insurance Company can deny the claim. If this is not all, then section 45 of the Insurance act comes to the rescue which with its recent amendments says:

No Policy of Life Insurance shall be called in question on any ground whatsoever after expiry of 3 yrs from

- the date of issuance of Policy or

- the date of commencement of risk or

- the date of revival of Policy or

- the date of the rider to the Policy

Whichever is later

However, this also means that company can question your policy and details provided by you within first three years, and may cancel your policy if any misrepresentation or fraud is found.

Conclusion:

One should not go finicky about the claim settlement ratio while selecting a Life Insurance Policy. This can be one of the parameters, but should not be the only one.

If you have bought the insurance policy by disclosing all the material facts, then no company can deny the insurance claim, and if you have concealed the facts or done some fraud then no “High claim settlement ratio” will be of any help and your claim is bound to get rejected. However, Section 45 of Insurance act comes to your rescue after 3 years.

{kind=link}

Indeed an very good article on claim settlement ratio. this

is one of the important factors that you should consider while deciding on the insurance provider to buy a term life insurance plan. Claim settlement ratio is published every year.