Kusum looks quite impressed with my last article on the balanced funds. For the same. She is a First-time investor and was searching for something which is less volatile and does not demand regular attention or rebalancing from the Investor side, the reason for her liking of balanced advantage funds.

Frankly, the article was quite a routine topic for me. But these kinds of replies make me wonder, how the things which seem quite simple or general to one, becomes quite useful and helpful to others. Kusum kinds of readers make me feel more responsible and caution me that I have to be extra careful while writing.

But as I replied to her that she

should treat my article just an information and not as advice. So, if she has

no professional advisor by her side to guide her, she should do her own

detailed research before doing any investment.

She agreed but further asked me one more question. She wants to know if there are such balanced funds available where she can invest and save on income taxes u/s 80C

It is commonly known that you can save taxes u/s 80C by Investing in ELSS (Equity Linked saving Scheme) Mutual funds? In case you are not aware, then let me give a brief on the same. (Read: List of all qualifying instruments under section 80C)

ELSS funds are Equity Mutual funds, which are notified and approved to be used for tax saving u/s 80C. In this, you may invest up to Rs 1.50 lakh to claim a tax rebate.

Being a pure equity product, sometimes an investor with a moderate approach prefer not to go with ELSS scheme, and for some reasons also not interested in the conservative segment of PPF or other traditional products due to high lock-in, etc. then for those kinds of Investors, are there different options available in Mutual funds?

Well, the answer is Yes.

There are some mutual funds other

than ELSS funds, investing in which you can save taxes u/s 80C, and that too

with a balanced approach. Below are the same

Conservative tax saving Mutual funds options

- Retirement

Oriented Mutual funds –

These schemes are meant to save towards retirement goals. However, these are like normal mutual funds except that these come with 5 years lock-in.

The lock-in period is 5 years or 60 years of age whichever is earlier. Post 60 years of age there is no lock-in and one may start with the dividend income or with a Systematic withdrawal plan, as per the choice and requirement of regular income. (Read: Bucketing strategy for Retirement income)

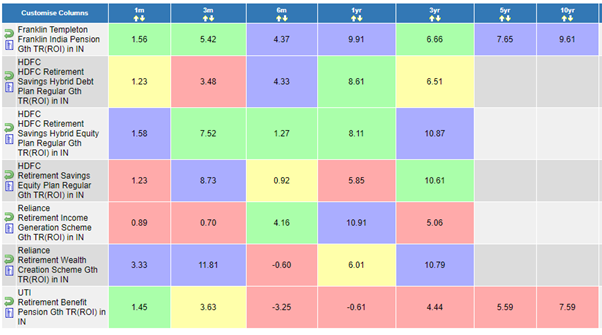

Two of the mutual funds in this category are quite old in this segment – Franklin Pension Plan and UTI Retirement fund. And both have a Hybrid conservative structure i.e. 60% Debt and 40% equity.

Post the Mutual funds recategorization in 2017, many other companies have also come up with Retirement oriented structure of funds., and that too with Hybrid structures – Equity and Debt. But not all the schemes are notified under Section 80C for income tax savings.

Some of the eligible schemes are as below:

Also, note that if you are going for a debt-oriented conservative structure, then the Capital gain taxation would be of debt mutual fund.

Also read: 3 Important rules in capital gains taxation

The interesting thing in these funds especially for Senior Citizens is that in some of the schemes there is neither any lock-in period nor any exit load. Not sure if this can be called a loophole for section 80C savings if you withdraw before 5 years.

Also read: Must Read: Why Retirement is considered to be the Most important Goal?

2. Mutual funds ULIP:

Another Non-Equity and Hybrid product in Mutual funds that will help in tax saving u/s 80C is ULIP. Yes, you got it Right – These are Unit Linked Insurance Plans, offered by Mutual fund houses.

Now, please do not confuse it with the SIP insurance products which many fund houses have started with, where they provide life insurance cover (Free of cost) to investors as a multiple of SIP amount.

ULIP in Mutual funds is also quite Old product and being offered by only two AMCs which are UTI and LIC Mutual fund.

UTI follows Hybrid – Debt/balanced asset allocation structure and LIC MF has a Hybrid aggressive structure. Both these offer 10-15 times of Insurance cover of your annual contribution but unlike SIP insurance, it deducts mortality charges from the Units.

Since the

insurance is offered under group insurance so the mortality charges would not

be that high in comparison to Individual insurance policies.

UTI ULIP has no lock-in Period and money can be withdrawn anytime within the tenure by paying the exit load of 2%, however, LIC ULIS has 3 years lock-in.

At the time of maturity in both the products, Investors will get 5% – 7.5% of Sum assured as Bonus too, which as AMC claims, is the additional benefit or can be called as covering the mortality costs.

Even if investors get 10-15 times of Sum assured on their contribution, the taxation in Mutual funds ULIP, unlike insurance policies does not come under section 10 (10)d but would be Capital gains as per the allocation structure in the specific fund.

Tax saving

Mutual funds for Conservative investors – Should you Invest?

Well, the answer to this question, can never be a one-liner. You need to weigh these tax saving mutual funds of its pros and cons based on your needs and requirements, and after understanding the risk and return features of the same.

You may find the returns in the schemes shared above quite less as compared to the regular ELSS schemes in general. This could be due to the High debt allocation as well as the high expenses in these funds. UTI ULIP has also recently seen some defaults in its debt portfolio.

You want a Hybrid product for tax saving, yes you have multiple options. You want a product with lesser lock-in, yes you have the product, but how redeeming the same before its tenure is going to be viewed by tax authorities that are not clear, You need to keep in mind the Post Redemption or maturity taxation too, and also the exit load if any, before going in for any investment.

If you have any question on these tax saving mutual funds schemes, do write in the comments section.

– Infographics")

{kind=link}

I would like to invest MF for next 15 yrs and want to keep 20 yrs tenure

Can suggest the good mutual funds schemes?

We do not suggest mutual funds like this. We follow the Financial Planning route. First, we will prepare a detailed financial plan, taking a holistic look at your financial profile, which includes your- goals, cash flow, risk profile etc. and then as per the financial plan, suitable investment recommendations are provided.

To know more, you may take a look at our service offerings, from the link below:

https://www.goodmoneying.com/personal-financial-planning-services/