I am always of the view that one should not mix insurance with Investment, which is why my advice has always been to buy a term policy for Insurance cover, and keeping the investments in flexible instruments like Mutual funds or tax-free products like PPF, to have a decent liquid and growing portfolio by your side.

But what if the Mutual funds start offering Insurance?

It is quite normal to get confused here. When Insurance company offers Investment, then the advice is to avoid it due to high charges and low liquidity? but what if Investments start offering insurance, then what should investors do?

And post-budget 2018, when Mutual funds are no longer tax-free instruments, does the Insurance Cover being offered by the AMC, make them tax-Free and put them under section 10(10)d investments?

These kinds of questions keep cropping up in Investor’s mind when they hear products like Sip Insure, SIP Shield, Century SIP.

Yes, nowadays some mutual fund companies have started offering Life insurance cover along with the Systematic Investments. Life cover will be some multiple of the monthly SIP installments. This article is about to understand and do a comparative analysis of these SIP with Insurance products. And to understand if this is an advisable product or just a marketing gimmick by MF houses.

SIP with Insurance products – in brief

Some Mutual fund houses have started offering Life Insurance cover along with the SIP investments. These are specifically named product/feature which is available in some of the existing schemes and the total cover depends on the amount of monthly SIP installment.

Just like Insurance companies promote themselves with monthly premium payments as SIP, same way now AMCs have come up with Insurance covers. But one should not get it confused with Insurance products as they are completely different in structure, working and conditions.

Since Mutual funds work under a regulated cost structure and have defined TER (Total expense ratio), as mandated by SEBI, so one may find comfort in SIP with Insurance products that no extra mortality cost will get charged in mutual funds, unlike ULIPs or Endowment Insurances.

The Insurance cover offered is not to make the Long term capital gain tax free, as Mutual funds do not come under the purview of section 10(10) D. It is just an additional feature to attract and retain clients for the long term.

Plus, in mutual funds, there is a limit on the maximum cover, but the investor will not be required to go through medical tests. The company will get a Good health declaration signed from the Investor and thus the onus of disclosing the facts will be on Investor only.

The Life Insurance cover will be provided through Group Insurance cover, and expenses will be borne by the mutual fund company

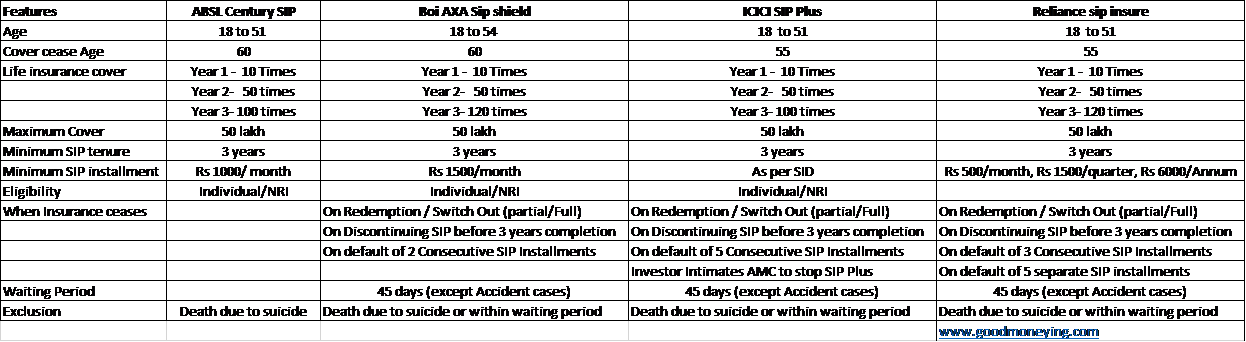

SIP with Insurance – A Comparative analysis (Click here to view the image)

SIP with Insurance – The Good Health Declaration

This is the most important part in Sip with Insurance products. Mutual fund companies are offering Life insurance under a group insurance plan in a tie-up with some life insurance company. Since no medical check-ups are required to have this insurance coverage, so the insurer will completely Rely on the declaration that you will provide in the respective forms.

This good health declaration asks 3 questions, and depending on the answer you give the final call will be taken by the Insurer whether to give insurance coverage to the investor or not.

The questions as asked on BOI AXA SIP Shield are as below:

- Have you ever been treated for Symptoms of high bp, diabetes, heart attack, or heart disease, stroke, chest pain, kidney disease, AIDS or AIDS-related complex, cancer or tumour, asthma or respiratory disease, mental or nervous disease, liver disease, blood disease, digestive and bowel disorder, disorder of bones, spine or muscle?

- Have you within the last 2 years taken any form of medication for more than 14 consecutive days to treat an illness or disease?

- Have you within the last 2 years consulted any medical practitioner for any condition other than minor impairment such as cold or flu?

I am not sure how Insurer looks at the answers, or how sellers pitch to buyers, but from an Insurance perspective, these are quite broad questions and if someone answers in “Yes”, then would the insurer ask for further documents or conduct some medical tests? Or leniency is a norm in the group insurance policy.

And if the investor hides the facts and answers in “NO” which should otherwise be “Yes” and the policy results into an early claim, then will the insurer remain lenient at the time of claim too? These are some of the important unanswered questions which make these products not that dependable.

Mutual funds SIP Insurance – Should you Invest?

Well, there is no extra cost of insurance, so this is an advantage. FREE definitely attracts but then you should not depend only on this insurance and avoid the paid insurance covers.

No Medical tests also look attractive but then the onus is again on you to give the disclosures fully and completely. As good health declaration is also too broad, so it leaves scope for insurers challenging the same.

Continuation of Insurance cover even after discontinuation of SIP post 3 years may also look like a benefit, but the benefit will not be of 100 times of the monthly SIP amount cover, it will be equal to the fund value or 100 times of monthly installment or maximum cover allowed.

All in all, there is no harm in taking SIP with insurance cover, but select the product wisely. Do not stick with the product just because of SIP Insurance, and the most important part, is to consider this as a Top-up Life cover, and buy the basic and required cover through Term Insurance plans only.

{kind=link}