Term Insurance plans have lost their simplicity. Yes, the plans which used to have a straight forward structure as in to pay the nominee in case of Insured’s death and nothing if no death, are now days confusing buyers with the Regular income or staggered payment options in case of claim.

Staggered payments itself are a confusing lot with different options with different Insurers. Some say that they will pay some portion of sum assured in lump sum plus balance in fixed Monthly/Annual payments, others offer increasing monthly/annual payments and some are offering both like 100% lump sum plus regular income benefits.

Every option has different premium pricing, and every buyer wants “Itne kam mein Itnaaaa”. I have got many queries from my blog readers on how to select online term insurance with income benefits or staggered payout benefits.

This made me look into these online term insurance with income benefit plans in details, and this article is about my findings.

Online Term Insurance with Income benefits – what is the offer?

I looked into online term insurance plans of 4 companies, which offer such plans. Besides the normal and “Traditional” feature of paying 100% to the nominee on death of Life assured, they also offer

Kotak online term plan – Kotak Life Insurance Preferred e-term plan

Birla Sun life online term plan- BSLI Protect @ ease

Max Life Insurance online term plan plus

So in short there are mainly 2 options,

- Taking part portion as Lump sum and balance in Monthly/Annual Installments.

- Taking part in Lump sum and balance in Monthly/Annual Installments with increase at fixed simple interest on first installment.

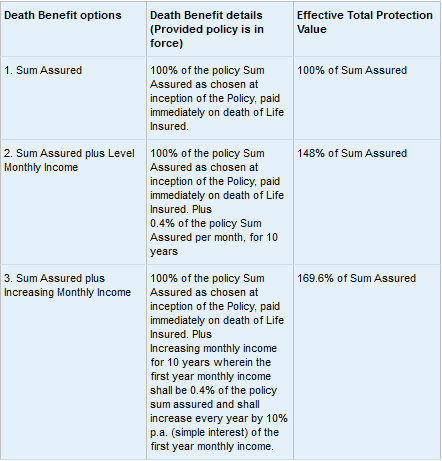

Max life options are same as of HDFC Income plus, where it will pay 100% of sum assured in Lump sum and in addition staggered payments for some years.

Now let’s do some mathematics to understand how this structure actually would work?

Online Term Insurance with income benefits – Comparative Analysis

Birla Sun life Protect @ ease

First thing you need to understand is that we cannot do any analysis on Premium amount, as every company has its own underwriting process. But still within the same company’s product you may compare premiums in different options and see that more you leave with company to pay later, lesser will be the premium.

In Birla Sun life, the choice is with nominee and not with the insured on how to take the claim payment. That is why, there is no choice of premium and options at the time of policy purchase.

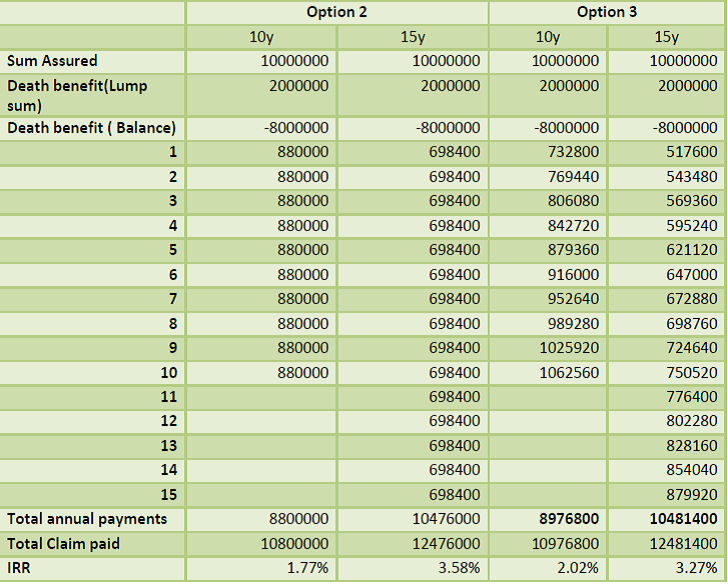

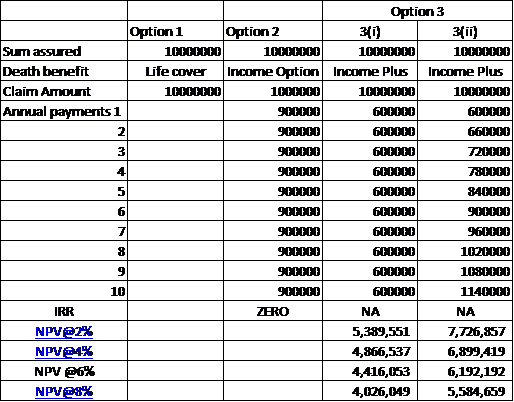

For calculation perspective I have assumed Sum assured to be Rs 1 crore in all cases.

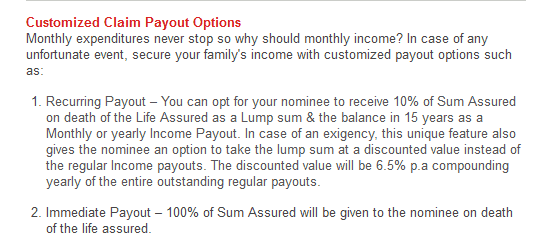

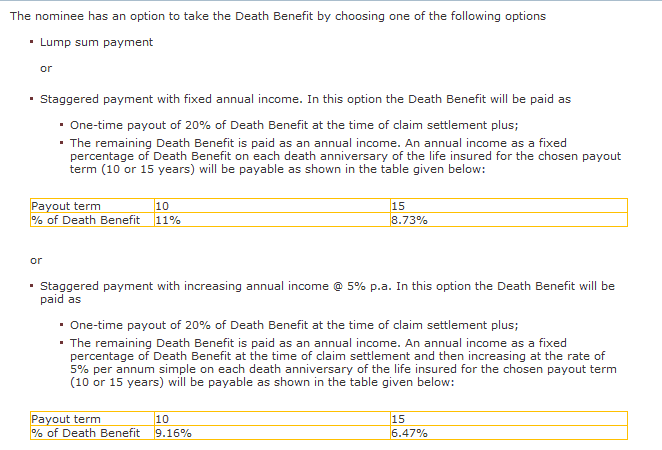

In Birla protect@ease option 2 i.e. Staggered payment with fixed annual income – It will pay 20% as lump sum and rest 80% in 10 years or 15years time frame as per choice of nominee. In 10 years option, nominee will get 11% of death benefit per year, and in 15 years option nominee will get 8.73% of Death benefit per year

This means Rs 20 lakh will be paid as lump sum and balance can be taken as Rs 880000 lakh per year for next 10 years or Rs 698400/- per year for next 15 years.

Option 3 is with staggered annual income increasing @ 5% per annum (Simple Interest).

You can see from the calculations above that Nominee would have to leave Rs 80 lakh with insurer to get the staggered annual payments, and IRR ( Internal rate of return) coming out to be very less.

Kotak e preferred term plan

In Kotak Life insurance there is no increasing annual income option, but a simple option of paying 10% as lump sum and balance in 15 years monthly or annual installments, which makes IRR to ZERO.

Though I do not find much of difference in premium amounts in my age (35y) for Rs 1 crore of Sum assured, but even if there is difference you need to understand that later on if policy gets claimed then family would lose interest on 90 lakh of amount, which in itself would be considerable.

HDFC life Click to Protect Plus

Options summary

Option 2 (Income Option) is similar to that offered by Kotak Life Insurance. Option 3(i) and 3(ii) (Income Plus) are similar to Max life online term plan plus, so I am showing only HDFC calculations, and not of Max life and kotak.

In Option 2, nominees would lose on the interest amount on Rs 90 lakh, which I feel would be considerable.

Option 3 (i) and 3(ii), I think is a combination of 2 term policies. One which pays in lump sum and other pays as staggered amount. Calculation of NPV (Net Present value) shows that how much nominees would have to invest at what rate to generate the same cash flows what this insurance company offers. Thus, NPV values can give you a choice whether to go for a bundled product, which may be equal to buying 2 insurance policies or 2 separate policies. That means if you need to compare the premium of the policy with this option to two separate simple policies of a higher amount.

Online Term insurance with income benefits – Should you buy?

Whatever we say that people have understood the importance of Life insurance and seek out term insurance policies, but this is also true that everyone wants to have term insurance on least premium possible. And that is why when some online term insurance with income benefits plans offers low premium, it is quite natural to attract eyeballs and becomes the first choice for the buyer.

Staggered payment options may sounds good emotionally, as it makes sure that family should keep getting regular money cheques and thus suits where insured does not have confidence on financial management capabilities of the family after him/her. But, financially it does not make sense at all.

As shown in the calculations above, if company is paying sum assured in parts, then your family would lose heavily on interest income, which can be very decent if finances are managed properly.

And if the policy is being offered with additional income besides sum assured then that is nothing but a combination of 2 policies, one pays in lump sum and other as monthly or annual benefits. In this case also you may be better off buying 2 policies, and put down a financial management structure at place.

If you are really serious on family’s financial wellness, then involve them in your financial decision making. Financial planning does not mean buying products, but if done and understood properly it will also help in proper distribution and usage of funds as and when required. No single product can give you the solution, it’s the process and understanding that will help.

So do your families a favor…make them financially aware. Stick to the basics and have an adequate insurance cover that pays in lump sum and help your families learn financial management.

What are your views on these online term insurance with income benefits? Do share

{kind=link}

The choice of income (as compared to lumpsum) is clearly and only for those (and there are really a big many of them) who do not know how to handle large sums of money. e.g. a lot of housewives (due respect to them) – give them a crore rupees and they will not be able to manage it. They typically turn towards relatives and friends for help, and quite a few of them end up getting duped. So it is not about logic and time value of money, etc.

That’s exactly my point. Don’t let them take advantage of your weaknesses, empower the housewives. If husbands are wise enough to understand the importance of insurance, they should extend their wisdom by helping their spouses get financially literate too.

If someone is prone to getting duped with crores, then the same thing can happen with lakhs too. A product cannot be a solution.

In Economics there is a term used; “All things being equal”, Only if the matter was specifically about financial sense…

With due respect sir, even an educated person earning decently good are not to be trusted with money with many of them coming to you seeking help for choosing a simple term plan, it is almost impossible to teach Housewives, children and other family members(with exceptions of course) financial prudence. Also such decisions fall on them when they at most vulnerable emotionally and therefore prone to major bad decisions.

What you are saying is perfectly alright for those who are financially educated or have support from Advisors like you but for rest it might not be ideal product.

I am not favoring any version of term plan per se but I think it is alright to factor in other things(mentioned in your post) apart from financial calculation. And in that regard I think it is a good thought from the target segment it caters to even if at the cost of lower returns in future.

All the best 🙂

Good job Manikaran.Thanks for your valuable guidance and motivation.

Thanks Amrit

Pragmatic approach and guidance to non-financials.

In the unfortunate death of bread-earner, getting a lump-sum benefit for the family ensures that the family could achieve their future financial goals and commitments but it might be possible that the initially-available corpus could not meet their regular expenses over time due to low profile income. In such a scenario, choosing a combination of partial or full sum assured (SA) as a lump-sum and 0.5% of the sum assured as regular flow of monthly installments with an increasing payout at the rate of 10% every year over 10 years can be made a viable option. This will adjust for one’s family regular expenses to account for inflation. This could also prove be invaluable option for those who need to get insurance coverage more than 20 times of their annual salary due to high financial commitments as many insurance companies do not give coverage more than 20 times of one’s annual income. Moreover, the additional benefit of getting a lump-sum as well as monthly payout is that receipts in both cases are tax-free. In case you get only a lump-sum, the income generated from investment of the lump-sum in safe products, like fixed-deposits (FD) with scheduled commercial banks, would be liable for taxes. The family’s financial literacy is important while choosing a lump-sum benefit term plan versus income distributed overtime. Even financially literate people find it difficult to keep money safely, if they get a large amount as a lump-sum. The consistent income overtime can prevent a situation where the recipient fritters away lump-sum payment and will help the family to stabilize and live with dignity.

A Short and logical article provided up there. Term insurance offers a high cover amount at a nominal premium. Other than that, term insurance plans are designed to be reasonably priced – a combination of affordability with simplicity. It also you provides an option to pay premiums on a monthly, semi-annual, or annual basis. Buying it online makes it more convenient.

Thanks a lot for this amazing article on online term insurance benefits. Anyone with financial dependents should buy a term insurance policy

. This includes married couples, parents, young professionals, SIP investors and in some cases, even retirees.