It was not a regular budget and main tax proposals generally get presented in the regular budget only. But still, Finance Minister was of the opinion that small taxpayers especially the middle class, salary earners, pensioners, and senior citizens need certainty in their minds at the beginning of the year about their taxes.

That is why, keeping the Present Income tax Slabs and Rates Unchanged, the budget 2019 was announced with the following proposals relating to the Income-tax 2019-20.

The object of Finance Bill 2019 is to continue the existing rates of income-tax for the financial year 2019-2020 and to provide certain relief to taxpayers and to make amendments in certain enactments

Income Tax Changes in Interim Budget 2019

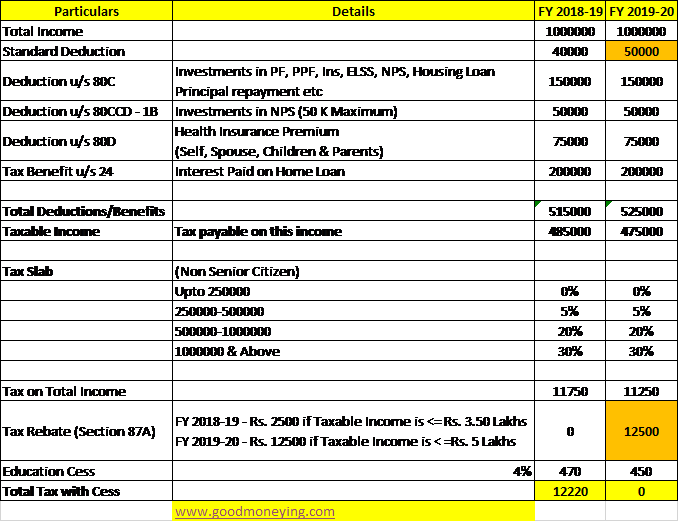

- Section 87A – Rebate of Rs 2500 available under section 87A, for the person having taxable income up to Rs 3.50 lakh has been Increased to Rs 12500, and that too for the person having total taxable income (Income after all available deductions) of Rs 5 lakh.

This means if you have a Taxable income of Rs 5 lakh or less, you will get a full rebate and you need not pay any income tax.

However, if your net taxable income is even Rs 5.10 lakh, you will be charged on Complete income as per the Slabs (5%, 20%, 30%).

Here the Income of 5 lakh means the income after claiming all the deductions under section 80C, NPS (80CCD), Home loan interest payment u/s 24, education loan Interest (Section 80E), Section 80D etc. or whatever section you may claim deduction under.

2. Standard Deduction – The amount of Standard deduction which was reintroduced last year has been increased from Rs 40000 to Rs 50000.

A Standard deduction reduces your taxable income and thus tax Liability. This will also be counted in the deductions as mentioned in the Point no. 1 above.

3. Income from House property:

If you have 2 houses, only one can be called as Self Occupied and other will be treated as “Deemed to be let out” even if it is not actually let out.

And the Notional Rent (Fair market value Rent) will be assumed for Calculation of Income from House property which gets added in your total Income.

(Read: How to Calculate Income from House property)

In Interim Budget 2019, Considering the difficulty of the middle class having to maintain families at two locations on account of their job, children’s education, care of parents etc.

The finance minister has announced exemption in levying of Income tax on Notional rent on a second self-occupied house.

This means no more tax on the second house “Deemed Income” from FY 2019-20. But if it is on Actual Rent then that is to be considered as Income and counted in Income from House property.

4. Capital gains taxation from House Property (Section 54):

While saving Long term capital gain tax on the sale of Residential House property, the assessee was allowed to invest in buying or constructing only single residential property or buy capital gain bonds. (Read: Should you buy capital gain Bonds to save LTCG?)

But In interim Budget 2019, the finance minister has proposed to extend a one-time benefit on saving LTCG on Residential property on buying or constructing 2 Residential properties. The only condition is that capital gain should be 2 crores or less.

(Read: How to save capital gain tax on the sale of the property?)

5. TDS on Interest:

The Threshold on TDS deduction on the Interest income earned from bank or post office deposits has been increased from Rs 10000 to Rs 40000.

This means no TDS will be deducted on the Interest income up to Rs 40000 by bank or Post office. But please do remember that this does not make your Interest Income tax Free.

Bank Interest is tax-free up to Rs 10k u/s 80TTA and Rs 50k for Senior citizens u/s 80TTB.

Besides all this, the budget seems to be directed more towards the rural and unorganized sector. One big announcement of a Mega pension programme for workers in the unorganised sector was done with the name “ ‘Pradhan Mantri Shram-Yogi Maandhan”

This pension yojana shall provide them an assured monthly pension of ` 3,000 from the age of 60 years on a monthly contribution of a small affordable amount during their working age.

It is expected that at least 10 crore laborers and workers in the unorganized sector will avail the benefit of this scheme within the next five years making it one of the largest pension schemes of the world.

It seems to be as big as Ayushman Bharat.

Would be interesting to see, how the things get managed, without compromising with the Fiscals.

Interesting days Ahead!!

(Read: The Budget Speech and the Financial Bill)

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

I think very analytical presentation of the gist of the Budget proposals. Even comparing the same income level between two financial years and its impact on net tax liability is also very crisp, clear and unambiguous.

Many thanks for such analysis.

Thanks Kamal Ji

Hi Sir!

I have read every single article available on your website across all sections.

This time again budget summery a was as expected, simple yet clear analysis.. thank u so much for sharing Ur knowledge with us. Sir please help us to understand the benefits of investing in NPS along with tax benefits during investment and tax treatment on corpus generated. It is entirely tax free now??

As an aggressive mutual funds investors should I consider investing in NPS more than the tax exemption limit or should I restrict it to only tax limit?

Would be grateful for Ur support.

Regards

Ketaki

Thanks, Ketaki for being a Regular reader. Your kind of comments and appreciation encourage me to keep writing.

NPS gives you tax benefit u/s 80CCD. You may claim full 80C benefit by investing in NPS or may claim 80CCD benefit by investing Rs 50k into it which will be over an above the 80C limit of Rs 1.50 lakh.

On maturity of the product, you have to compulsorily buy an annuity of 40% of the corpus and 60% you may withdraw as a lump sum.

100% of the maturity amount has been announced as tax-free i.e. 60% withdrawal and 40% transfer to buy an annuity, but still, the notification is awaited at this moment.

I don’t think you should invest more than what is required to claim tax exemption if you are managing your money well on your own.

Hope this helps.

Thanks