Bank Lockers are not a new service by Banks to its customers. A lot of people use these safety deposit boxes in the banks to keep valuable items like- jewellery, gold, other precious items, or even documents like property papers, will, etc. which they feel are not safe to keep at home.

Also read: Open DigiLocker Account- Keep your Documents safe

The Bank charges a fee for the locker services provided in the form of annual rental. It varies depending upon the size (small, medium, or large) and the city (metro, urban, or rural) in which you want the locker. The amount ranges from Rs.1500- Rs.15,000 (including GST), although may vary from bank to bank. In addition, a small amount is also charged every time you visit your locker.

The Reserve Bank of India has set some guidelines for the Bankers as to operations and management of Bank Lockers but it has come to the notice that in some cases, Bankers are trying to bend or break these rules for their own benefit. It was found that they are mis-selling some products or were unnecessarily harassing the ordinary customers, who are not aware of the rules. (Also Read: Mis-selling or Mis-buying). Also, to bring clarity on the liability on the banks in case of any thrft, burglary etc. and also where banks may not be at fault.

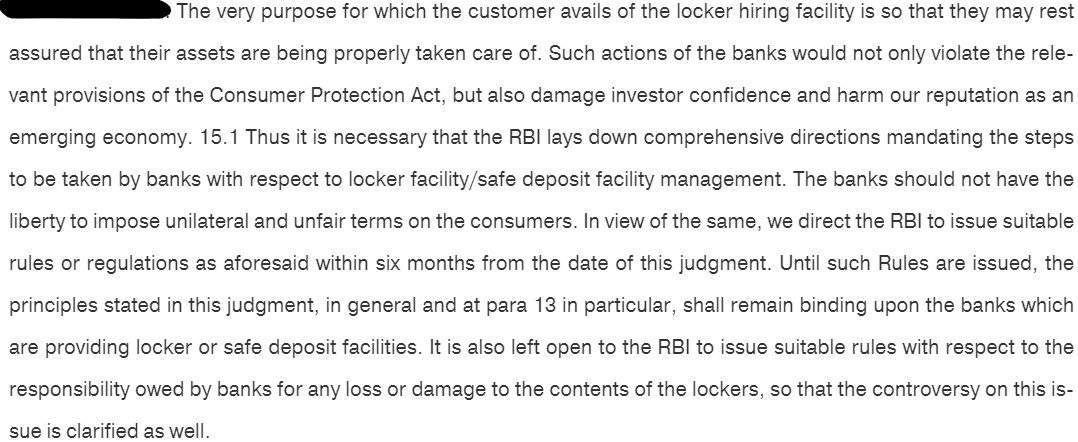

In Feb 2021, the Honourable Supreme Court in the judgment of the ‘Amitabha Dasgupta vs United Bank of India’ case directed the RBI to come up with comprehensive guidelines on Bank Lockers to protect customers’ interests within 6 months. Here are some of the highlights of the Judgment which led to the framework for the change of Bank Locker Rules.

Thus, the Reserve Bank has issued new Bank Locker Rules in August 2021. These new bank locker operation rules will be applicable to both existing and new lockers and would come into effect from 1st January 2022 (unless stated otherwise). Let us understand what these rules are and are these going to help curb the malpractices of the Bankers, in detail.

Important Bank Locker Rules 2022:

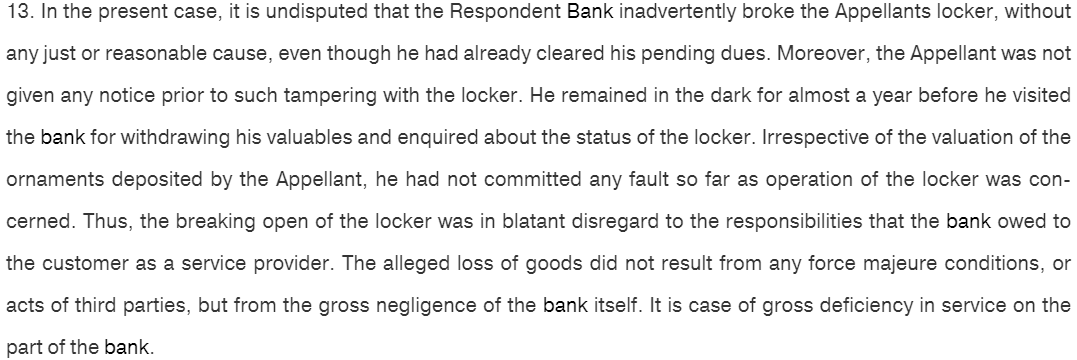

1. The liability of the Bank in case of loss of contents:

Earlier, there was no clarity as to how much compensation the bank is liable to pay in case of loss of the contents in the locker, or whether there exists any liability or not.

But these new Bank Locker Rules have made this aspect clear. The liability of the Bank is fixed at 100 times the annual rent of the locker if the contents in the locker are lost due to negligence or fraud committed by the employees, fire, theft, robbery, collapse of the building, etc.

For instance, if the annual rent of the locker is Rs.5,000 the bank is liable for a compensation of Rs. 5 lakhs.

However, Banks do not have any liability if the locker contents are lost or damaged due to natural calamities like- earthquakes, floods, thunderstorms, etc.

These RBI rules further clarify that the Bank employees’ should take proper care, maintain due diligence and make every effort to prevent such damage. Also, the Bank should also have branch-level insurance against such happenings to minimize the risk.

Also read: Deposit Insurance in India- How safe are Bank Deposits?

2. Transparency in Locker Allotment:

To protect the customers from the corrupt practices adopted by the Bankers due to high demand and lack of transparency in the locker allotment process, the new Bank Locker RBI rules in India direct the banks to maintain a branch-wise list of vacant lockers, electronically on the Core Banking System (CBS) or any other such mechanism, issued by the RBI.

Also, if the locker is unavailable, the customer has to be provided with a wait-list number, to each and every customer. The Banker cannot deny any locker application.

3. Cap on the Security Deposit:

The new Bank Locker Rules, clearly state that the Banker is allowed to take a term deposit equivalent to not more than 3 times the annual rent + locker breaking charges as security at the time of the locker allotment. This is in lieu of the recovery of unpaid locker rent by the Bank, from the new customers only. The Bank cannot force the existing customers with active accounts for such a deposit.

For instance, if the annual rent of your bank locker is Rs.5,000, then the maximum amount of fixed deposit the bank can ask is 15,000 plus a nominal locker breaking fee, not more than Rs.500.

But, the Bankers to meet their sales targets used to sell ULIPs or Endowment Plans, or force them to have an FD of an exorbitant amount. Hopefully, this rule would put an end to this mis-selling.

Also read: When should you surrender your LIC Policy?

4. SMS and email Alerts:

Now, the bank will send you SMS and email alerts the same day you accessed the locker. Alerts would also be sent if the locker is not properly closed or the Bank has to open the locker due to any genuine reason. This would help prevent any unauthorized access to the locker.

5. CCTV Footage of Locker Room Operations:

The new Bank Locker Operation Rules, mandate the Banks to install CCTV cameras in the locker room and keep the footage of the operations for 180 days and should ensure its proper security. They may also install an Access Control System which will create a digital record of the access with a time log if required.

6. New Locker Agreements:

All existing Bank Locker customers have to sign new Locker Agreements on or before 1st January 2023. The new agreement will include all these revised Bank Locker Rules. This has to be approved by the Bank’s Board. A model agreement is to be drafted by the Indian Banking Association (IBA). A duplicate copy of this agreement would be provided to you and the original one would be kept at the branch where the locker is situated.

7. Disclosures on the Website:

The Bank will have to disclose the model agreement along with the updated Terms and Conditions and Standard Operating Procedures (SOPs) related to bank locker operations on their website. In addition, they are also required to display the list of branches where the lockers are available and the details about all kinds of locker charges.

8. Closure of the Locker:

If you want to close the locker, you have to fill the locker surrender form, remove all the locker contents, and return the key to the Bank. The Agreement would be terminated and the rent collected in advance at the time of allotment would be refunded.

Some Common FAQs on Bank Locker Rules

No. As per RBI guidelines, Banks cannot offer any insurance product for the locker contents, directly or indirectly.

Yes. In certain circumstances, Banks are allowed to open your locker according to the Bank Locker RBI rules.

i) If the rent of the locker is unpaid for 3 years.

ii) If the locker remains inoperative for 7 months and the banks cannot locate the customer, even if the rent is paid regularly. However, the Bank may consider if the reason for in-operation is genuine and provided in writing by the customer.

iii) If you lose the key to the locker and request the bank to open it.

iv) In case of a court order or any other investigation agencies want to access or seize the locker.

v) Non-cooperation or non-compliance with the terms and conditions as mentioned in the agreement.

But, it needs to be opened in the presence of Bank officers and two independent witnesses, and the video of the same needs to be recorded. The list of inventory needs to be duly recorded by the Bank and communicated to the customer.

So, it would be prudent to visit your locker regularly, at least once in 6 months, and pay your locker rent on time.

Although one key to the locker is always available with the Bank, as per Bank Locker Rules you would be liable to bear the cost of replacing the lost key. You need to inform the Bank immediately if you lose the key and return it if you find it in the future.

Yes, just like Bank accounts, Lockers can be held in joint name, and a nomination facility is also available. So, in the event of death or unavailability of the first holder, the joint holder can access and operate the locker. If both the holders die the nominee can access the locker by providing the required documents along with the claim form.

Also read: Joint Account or Nomination- what is better?

On the death of the customer, the nominee(s) or the legal heir(s) would be allowed to operate or remove the locker contents within 15 days of the receipt of the required documents like- death certificate, KYC of the claimants, etc. In this case too, before giving permission to the nominee/legal heir to open the locker, Bank would have to prepare the inventory of the contents in the presence of two independent witnesses. (Also Read: Why you should not ignore the Bank, asking to re-submit KYC Documents)

Well, not 100%. As mentioned above, as per the Bank Locker rules, the liability of the Bank rests to only upto 100 times the annual rent, that too if something happens to the locker contents due to the negligence of Bank employees. It may be possible that the value of the contents in the Bank locker far exceeds this amount.

Conclusion:

Let’s hope that these new RBI Bank Locker Rules curbs the malpractices done by the Bankers in locker allotment. If you find any banker pitching any insurance plan or FD to you in lieu of the locker, you may tell him what the rules say.

If you are dealing with a PSU Bank, you can also file an RTI to the Bank Manager to know the Bank Locker operation rules. In extreme cases, you may also approach the Banking Ombudsman with your grievances.

This article on New bank locker rules 2022, written by Mr Varun baid, CFP Professional

{kind=link}