Union budget has always been one of the most important events for the country as well as for Personal & Corporate finances. The government prepares its own Income and expenses statement, and figure out the areas which require more attention, and allocates the resources for the overall development of the economy.

Individual and Corporates prepare and review their own future business and financial plans based on the proposals made by the government after understanding the impact of government action or inaction on their future development.

So there is nothing called Good or Bad Budget, as that will only be a perception, which differs from person to person, economist to economist, Corporate to Corporate. We need to understand what proposals are going to impact us and in what way so we can be prepared for it, make necessary changes in our personal structure.

There are few proposals that are going to directly impact the Individual Taxpayers, Equity Investors (Direct or through Mutual funds), Non-Resident Indians, Home loan Borrowers, people travelling abroad and many others.

8 Important proposals announced in Union Budget 2020 and its impact on your personal finances.

- New Income Tax slabs announced.

With the target of providing ease of tax filing to the assesses,

and expecting them to do it themselves, without taking any professional help,

the finance minister has announced the new Income tax slabs for FY 2020-21.

Using this slab would be optional on the part of the assessee, as if opted for, then one has to forgo all the exemptions and deductions available under various sections

The new Income tax slabs are as below

| Total Income | Tax Rate |

| Up to Rs 2.50 Lakh | NIL |

| From Rs 2.50 lakh to Rs 5.00 lakh | 5% |

| From Rs 5.00 lakh to Rs 7.50 lakh | 10% |

| From Rs 7.50 lakh to Rs 10.00 lakh | 15% |

| From Rs 10.00 lakh to Rs 12.50 lakh | 20% |

| From Rs 12.50 lakh to Rs 15.00 lakh | 25% |

| Above Rs 15.00 lakh | 30% |

If you opt for the above rates and calculations, then you have to forget all the available exemptions and Income tax deductions like the House rent Allowance, Standard deduction, Deduction u/s 80C, Health insurance benefit u/s 80D, housing loan tax benefit, education loan interest benefit and all other you may be eligible for …in short no benefit can be claimed just pay tax SIMPLY.

Which option should you chose will depend on the composition of your salary, your loan profile, your savings potential, etc.? So, one has to do comparative analysis and if the old slab rates look more beneficial, then you may go with them.

For the Sake of immediate understanding below are the

old/existing slab rates applicable in FY 2019-20 and Optional in 2020-21

| Income tax Slab (Rs) | Age less than 60 | Age 60+ | Age 80+ |

| Up to 2.50 lakh | NIL | NIL | NIL |

| 2.50 Lakh – 3.00 lakh | 5% | NIL | NIL |

| 3.00 lakh – 5.00 lakh | 5% | 5% | NIL |

| 5.00 lakh – 10.00 lakh | 20% | 20% | 20% |

| Above 10.00 lakh | 30% | 30% | 30% |

- Deposit Insurance limit has been Revised.

The minimum guarantee given by DICGC towards your bank deposits has been increased from Rs 1 lakh to Rs 5 lakh. (To know more on deposit Insurance in India, click here)

- Employer benefits capped:

Employer provides various benefits to an employee in the form of EPF contribution, Superannuation benefit and NPS 80CCD (2). These benefits to some extent are tax free in nature. For high-income earners, these benefits are kind of additional advantage which an employer offers to the employee.

Now the government has proposed to consider the employer contribution in Employee superannuation plan if the amount exceeds Rs 1.50 lakh in a financial year as a taxable perquisite.

Besides this, if the total contribution by the employer in EPF, Superannuation and NPS exceeds Rs 7.50 lakh then the over and above amount will also be considered as taxable perquisite.

Also read: What is Superannuation, in comparison to NPS

- Changes in NRI Rules:

NRI is the person, who should not be

in India for at least a period or periods amounting in all to –

- 182 days in the FY and

- 365 days out of Preceding 4 FYs and

60 days in the Previous FY (Year for which we are checking the status)

Both the above conditions need to be

satisfied for one to be called as NRI

Also, when an Indian citizen residing abroad

comes to visit India, then also the 60 days condition will be replaced by 182

days.

Now Government has proposed to replace 182 days

condition with 120 days, to define the resident status for the one who claims

to be on a visit to India.

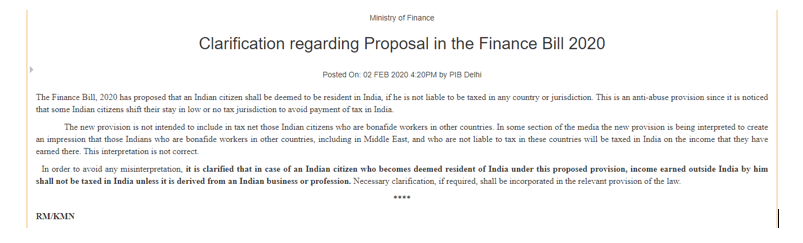

Besides this, the government has also proposed that an individual, being a citizen of India, shall be deemed to be resident in India in any previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.

This proposal has created lots of confusion among the NRIs especially living in Gulf countries where there is no Income tax. Even Merchant Navy people were among the confused lot. To answer this, the government came out with a press release clarifying the same.

The other announcement for NRIs was

related to Returning NRIs, and their Resident but Not Ordinarily Resident

Status

An RNOR is an Individual who –

- Has been an NRI in 9 out of the 10 previous

years preceding to that year, OR - Has, during the 7 previous years

preceding that year, been in India for a period of, or periods amounting in all

to 729 days or less.

One of the above 2 conditions needs to be satisfied to be eligible to be construed as RNOR. Please do note that one condition is of your tax status and the other is on your stay in India. Read more on the RNOR status here.

In Budget 2020, the first condition has been proposed to be modified by replacing 7 years with 9 years.

So, with effect from 01.04.2021 (AY 2021-2022), the RNOR would be an individual or (the Manager, in case of HUF), who has been an NRI in 7 out of 10 previous years preceding to that year.

Also read: Who is an NRI?

- Equity Dividends are now taxable:

Dividends received from Equity shares as well as from Mutual funds would be taxable in the hands of the investor. Though Mutual funds’ dividends were made taxable last year, this year government abolished the Dividend distribution tax levied on the corporates for distributing dividends and made the same taxable in the hands of the investor. So, Equity share dividends have also become taxable now in the hands of the investor.

Also, the government has proposed to deduct TDS @ 10% out of the dividend being distributed by Mutual funds.

- Affordable Housing Loan Tax benefit:

The benefit u/s 80EEA as announced in the

last budget has been extended till 31.03.2021. You may claim Rs 1.50 lakh

Interest deduction in addition to the other available ones if the following

conditions are satisfied.

A) Loan to be sanctioned by a

Financial Institution between 1st April 2019-31st March

2021

B) For the House valuing Rs 45

lakh

C) To the person buying the

First House

- Segregated portfolio taxation:

If you are a debt mutual funds investor then there are chances you have seen some segregated portfolio in your debt fund statement, as in recent times many funds have experienced the downgrades or defaults in their securities. (Please refer this article for detailed understanding)

The confusion was on the cost of the Portfolio to calculate the capital gains in case of recovery of money at a later stage.

So, the government has clarified in this budget that in case of the segregated portfolio, the cost will be the same as that of the original portfolio, from where the units were separated.

- TCS on Foreign Remittance:

It is proposed to collect TCS @ 5% from the buyer of foreign exchange to Remit the money out of India under LRS (Liberalised remittance scheme) if the amount exceeds Rs 7 lakh in a Financial Year. The TCS would be @ 10% in case of Non-PAN/Aadhar submission.

LRS is used to send money to children studying abroad, to buy property abroad or even buy stocks listed in exchanges abroad. The maximum Limit in LRS is USD 2,50,000 in a Financial year.

- TCS on International Tour Packages:

Tour and Travel Operators offering International tour packages will deduct TCS@5% from the people booking International Tour packages with them.

Both these provisions- TCS on Foreign Remittance & Tour Packages would be applicable from 1st October 2020.

Concluding Thoughts

Questioning any budget is of no use, we will waste our time in analyzing if the budget was good or bad. Let TV channels do this work.

I was also expecting some instant solution for this slowing economy and people losing the jobs, with the government announcing some immediate identifiable measures, but no. Madam Finance Minister was not in a mood to play 20-20, but a test match.

They still want to keep a broad vision and plan towards the overall wellness (as they claim), and this time also they come up with the theme of Aspirational India, Economic development and Caring society.

I am sure no government wants the slowdown to

persist for long and hope the $5 trillion economy target gets achieved, which

will surely benefit all.

– Infographics")

{kind=link}

I want to know :

(1) whether in the new tax regime, benefits u/s 80-G (for donation to qualified trust entities) would be available or not.

(2) whether carry forward of LTCL (losses) – whether towards equity/equity MF/debt/debt MF would be allowed for set-off against future profits (capital gains).

with reference to Finance Bill, both these deductions are not allowed in the new tax regime.

please refer to thepage number 24 of the Finance Bill

https://www.indiabudget.gov.in/doc/Finance_Bill.pdf