LIC has launched a new product LIC Jeevan sugam, a single premium endowment plan. Last year during the same time period it had launched “LIC Jeevan Vriddhi” and continuing with its strategy of luring customers in the tax saving investment months it has come up with “LIC Jeevan Sugam”. This product offers multiple benefits, takes care of your financial growth, provides risk cover and ensures attractive returns too. No, I am not promoting LIC Jeevan sugam; I have just reiterated the words that LIC Jeevan sugam’s advertisement says in newspapers. I have gone through the product to understand if what they are saying is correct or not. Let me summarize this for you in this review article.

LIC Jeevan Sugam –In short

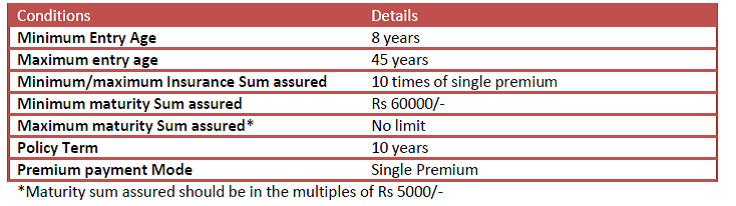

LIC Jeevan sugam is a single premium traditional non linked plan. The insurance sum assured will be 10 times the premium paid. You will get section 80C tax benefit on the premium payment and section 10(10d) benefit on maturity proceeds.

Maturity benefit will be the maturity sum assured plus loyalty additions if any, and

Death benefit will be insurance sum assured plus loyalty additions if any.

The Loyalty additions which depends on the corporation’s experience with the policies issued is payable

- on death , if policy has completed 5 policy years ,

- on surrender during the last policy year, and

- on maturity

At rates declared by the corporation.

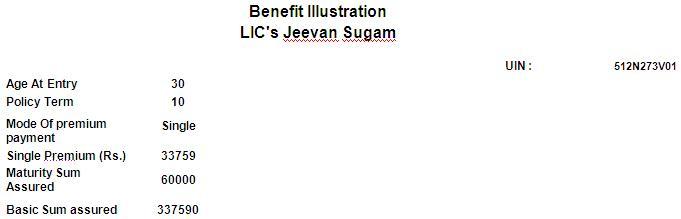

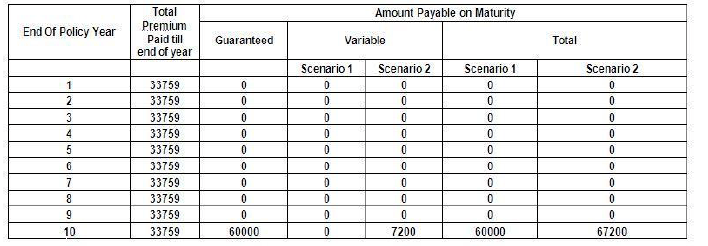

Eligibility conditions and other Restrictions in LIC Jeevan Sugam The Premium amount is dependent on the Maturity sum assured you select. Higher the Maturity sum assured, higher will be the premium. And to attract high premium, there’s some incentive offered in LIC Jeevan Sugam plan, which is as under. Incentive for higher Maturity sum assured by way of increase in the Maturity Sum assured is as under This means that in LIC Jeevan Sugam plan, if you opt for Rs 2 lakh of maturity sum assured, then on maturity instead of Rs 2 lakh, you will get Rs 2.07 lakh plus loyalty additions if any. Other features of LIC Jeevan Sugam Loan facility is available @ 60% of surrender value. Surrender value – First Year 70% of Single Premium paid, Second year onwards 90% of Single Premium paid. Let’s look at the Benefit Illustration of LIC Jeevan Sugam The non-guaranteed benefits (1) and (2) in above illustration are calculated so that they are consistent with the Projected Investment Rate of Return assumption of 6% p.a. (Scenario 1) and 10% p.a. (Scenario 2) respectively. In other words, in preparing this benefit illustration, it is assumed that the Projected Investment Rate of Return that LICI will be able to earn throughout the term of the policy will be 6% p.a. or 10% p.a., as the case may be. The Projected Investment Rate of Return is not guaranteed. Source of illustration : http://www.licindia.in/Jeevan_Sugam_benefit_illustration.htm

The above illustration clearly shows that @ 6% the policy could not be able to generate return more than the Maturity/guaranteed sum assured, so the column is blank in scenario 1.In that case the return from investment came out to be 5.91% p.a. At 10% it is showing that the Investment has generated 7.12% p.a. But all this is before adding service tax in the premium. When you inflate the premium with 3.09% of service tax the return comes down to 5.60% p.a and 6.80% p.a respectively.

But the question arises, isn’t the 10% rate on a traditional Insurance plan which invest in debt oriented instruments on higher side. In an economic scenario where the 10 years gsec is yielding around 7.8%, it is not wise to assume rate of 10% on such expensive investment instrument which involves a heavy distribution cost. I think that rate should be between 6%-8%, which means that in the above illustration the overall return should be between 5.60% – 6.80% p.a. This return will improve if the investor’s age is less than 30 years and also if someone claims tax benefit on the premium paid. But will decline in the opposite scenarios too. Also note that returns will vary among different personal financial profiles.

Should you invest in LIC Jeevan Sugam?

For young investor who wants a very safe product, looking for tax free returns and tax benefit on investment too, definitely this product can be considered. But it may not suit those who have completed his tax saving investment u/s 80C and also comes in higher age bracket. Being a financial planner, I always advise my clients and readers to invest in only those products which supports in achievement of financial goal targeted. Investment options should not be selected only on tax benefit or returns, but how it will help in achievement of the financial goals. That’s why I always favour keeping investments flexible and free from any lock in. Buying Term insurance and making investments in PPF/Bank FD or any other instrument based on one’s risk profile will always be a better and suitable investment. To enjoy the benefit of planning you just need to manage your investment behaviour.

Before selecting LIC Jeevan Sugam, you should compare this with the other flexible investment combinations available.

Do share your views on LIC Jeevan Sugam? If you have any question on LIC Jeevan Sugam, feel free to ask in comments section.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Hello ! I need to know if the single premium is 60,000 rs, then what will be the figure on maturity?

It all depends on your age and loyalty additions accumulated. As i wrote that premium will be calculated on the basis of age and maturity sum assured selected, so better to visit any LIC office or contact any agent for the same. Also pls note that Loyalty additions are not guaranteed.

I called an Insurance broker and told that I want to talk to “Max Saccha advisor”, lady on the other line asked my identity and i said that i am ” accha banda”, reply came…sir agar choti choti baato pe itna dhyan dete ho to life insurance lete hue kyo nahi? She further said ,” Sir, LIC hai to kahi aur kyo jana”.