Rahul is a young IT professional in his early thirties. His wife Sunita works as a professor in a college. On the advice of a relative who’s my client, Sunita visited me to have a financial planning discussion. She came alone. Where I appreciated her to have understood the importance of financial planning in the early years of married life, I was also surprised to learn that Rahul was reluctant to see me. Sunita was looking a bit worried. After inquiring and understanding the basic concepts of financial planning and gaining confidence in me, slowly she opened up with the real concerns. (Read: only 3 reasons you need a financial planner)

She told me that Rahul has almost every kind of loan in his portfolio, ranging from personal to credit cards, car loan to home loan. Even after earning a decent combined income, they hardly save anything for their future. Their friends and relatives feel that they are living a lavish lifestyle, but the reality is known to them only. All this is taking a toll on their health as their stress level was increasing, day by day. She wanted to clean the stables of her mangled finances, as soon as possible.

I wanted Rahul to be a part of this discussion, as, without his active cooperation, it was not possible to achieve the desired goal. I also wanted to understand his mind makeup which has led him to accumulate these loans. I took his number from Sunita and convinced him to visit me for at least half an hour. After some reluctance, he agreed. I told him to bring all the loan files along.

Also read: How to evaluate a financial planner?

While going through the details, I was reminded of my own mistakes which I did in the starting years of my working life. Like him, the first loan I took was in the 2nd month of my first job, for my first-ever vehicle. What a great feeling that was!! Then I took a personal loan to invest in penny stocks, which was a big blunder. Stocks became zero but I paid EMIs for 3 full years. My loan portfolio kept on increasing with credit card, more personal loans to pay off credit card dues, car loan, and then home loan. This kept on going until I got into financial planning and got serious towards my future.

Also read: Money mistakes to avoid in 2020

It is quite natural for anyone to get tempted towards loans, the moment one starts earning. After all now one is in position to buy things on one’s own and not depend on parents. With offers like buy now and pay later, the temptation soars as it sounds so attractive and easy to act on. Be it your holidays, phone, consumer durables, etc., all are available on EMI these days.

As I used to work with a bank, getting a loan was no problem and that was too at concessional rates. At that time, CIBIL scores were not required. But now things are different. Your obsession with loans can prove to be lethal for your financial future. One should be very careful while going for loans, and if by mistake one has already got into this vicious circle, start planning to pay off the burden, as soon as possible. After Rahul knew that he was not alone in this kind of a mistake, he agreed to extend his short visit.

Besides budgeting and cash flow management, which should be their starting point, I discussed with them a few factors they should consider before deciding on which loans they should focus their energies on, to clear off.

Below are some factors which one should consider and work in reducing debt exposure.

1. Type of loan:

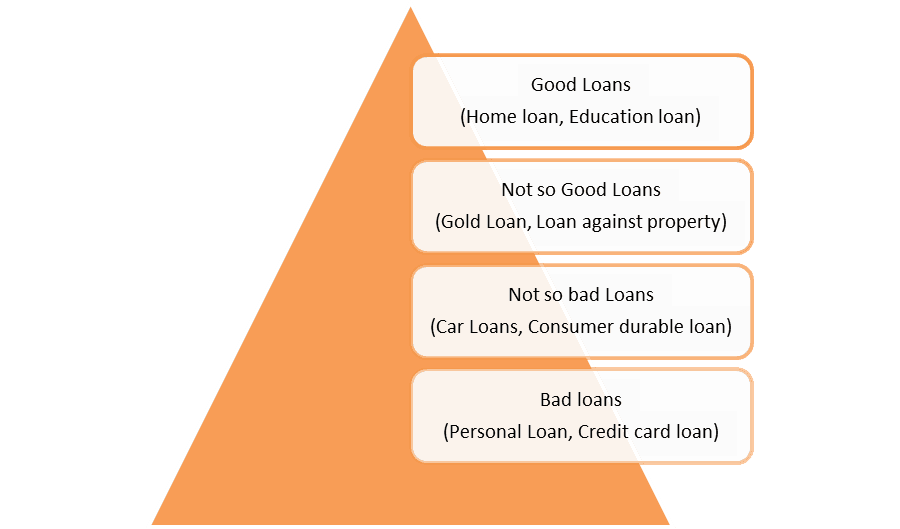

Depending on the productivity a loan brings in your personal finance, these are categorized into 2 parts – Good loans and bad loans.

Any loan taken just to spend on personal consumption is called a bad loan. These loans generally come under unsecured category i.e. you don’t need to show any collateral and also will not require a guarantor. These loans are purely disbursed based on your earning potential and repayment capacity like personal loans, credit card loans.

Good loans result in the creation of some productive assets like home, intellectual capital, etc. Home loans and education loans come under this category.

There are some “not so good loans”, which are taken against collateral with a specific purpose like for business expansion or personal emergency for e.g. Loan against property or gold loans.

The last category is “Not so bad loans”, which though results in the creation of assets but those assets are unproductive and depreciable like Vehicle loans, Consumer durables loan, etc.

While deciding on which loan to close first, the first factor you have to look at is the loan type and its impact on overall personal finance. Do note that where bad loans do not result in the creation of any asset, it also is looked down upon by credit scoring agencies, so you have to start with Bad loans first. One needs to stay off bad loans as much as possible.

Also read: Good Loans vs Bad loans

2. Interest rates and Tenure of Loan

People tend to prepay those loans which are near completion or paying high EMIs on. They ignore the interest outgo part. Interest portion of the EMI is the cost of the loan which you are paying. So, you need to have an understanding of what savings you’ll generate out of prepaying the loan.

Interest rates on bad loans as discussed above, range as high as 16%-36%. So, technically, it makes sense to close these loans first. But the tenure of loans also plays a major role in decision making towards pre-closure of the loan.

Also read: All about External Benchmarking of interest rates and it’s impact on home and car loan

It is true that the higher the rate of interest, the higher the outflow as the interest payout would be higher for the same level of the loan. So sometimes it doesn’t make sense to repay the loan in the later years of its tenure. Let’s understand this with an example of Rahul.

Out of his multiple loans, two loans- personal loan and car loan were taken simultaneously, as detailed below

Personal Loan (5 lakh) – Tenure 5 years, Interest rate 14%, EMI = Rs 11634/-.

Car Loan (7 lakh) – Tenure 7 years, Interest rate 10%, EMI = Rs 11621/-

| Year | Interest outgo (PL) | Interest outgo (CL) |

| 1 | 65355 | 66727 |

| 2 | 54265 | 59111 |

| 3 | 41520 | 50699 |

| 4 | 26871 | 41405 |

| 5 | 10034 | 31138 |

| 6 | 19796 | |

| 7 | 7266 |

This calculation is for illustration purpose only, real rates may vary.

The above calculation clearly shows that if one has to close any among both, one should work on car loan first, as it will result in more interest saving.

3. EMI outgo :

EMI impacts your cash flow. High EMIs mean lower surpluses left for other savings. Loans are not only a financial burden but a psychological one too. Doing away with high EMI loans usually generates confidence in one’s finances. Thus, if your high EMIs are keeping you awake at night, it is better to close those loans first. Living a stress-free life is priceless. (Read: important things to understand about loan EMI moratorium)

4. Tax benefits:

There are some loan options that come with tax benefits too. Needless to say, those come under good loans category. You get tax benefit u/s 80C and U/s 24 in case of home loan repayment, and in case of education loan you enjoy tax benefit u/s 80E as the deduction of interest payment from tax payable income.

Also read: Income Tax Deduction List FY 2020-21

Both Rahul and Sunita were very happy that now they have a direction and handholding on how things are to be sorted out. Rahul promised not to indulge in any kind of debt in future and Sunita took responsibility for budgeting and sticking to it, so they may come out of this trap at the earliest.

Also read: 21 Good Money Habits for a great financial life

Many times one cannot escape taking loans, especially with the housing becoming unaffordable and with rising education costs. But taking loans on unnecessary consumer durables or for personal consumption worsens personal finances. Your loan taking the decision should not only depend on your present desires but also your future goals. To make your present perfect, you should not make your future tense.

Service your loan EMIs on time, don’t take loans for consumption or your desires, take good loans if at all required. Your loan portfolio should not compromise your future!

Hope you liked this article on Loan Prepayment.

Do you think if there’s any other factor that I might have missed to consider before loan prepayment, then do share.

Related articles across the web

- Need Money? Personal Finance Tips When Borrowing from a Retirement Account

- 6 ways to generate regular income out of your savings.

– Infographics")

{kind=link}

[…] , requirements , other savings , risk profile etc. Read this article to have more understanding : http://goodmoneying.com/loans/4-…Now coming to mindset, Loan payment is a burden and if you have surplus with you, why don't you […]

nice article.

Thanks Ankit