Earlier when RBI announces any interest rates cut (Repo and Reverse repo) if you remember, every news channel and newspaper, used to write on how that might reduce your home loan, car loan interest rates and thus your EMI. But in reality, nothing of that sort used to happen (at least not every time) as the cut was by RBI and not by your bank.

It was all under anticipation

that now when RBI has cut down the rates, banks will follow the course and ultimately

consumer be benefitted. This is how RBI controls the money supply in the

economy and thus impacts the interest rates.

Just FYI, the Repo rate is the rate at which RBI lends to the Banks for their very short-term money requirements. (Know more on how RBI controls the money supply and interest rates? Click here)

In the last 1-year, RBI has reduced repo rate from 6.50% to recent 5.15%, but not much of change has been seen in the bank loan interest rates. This was due to the MCLR rate system that banks were following which was a function of the cost of funds (deposit rates) of the bank. And deposit rates are something internal to every bank with no RBI intervention. Thus, with high deposit rates, higher will be the lending rates, with not much of the impact of the RBI policies.

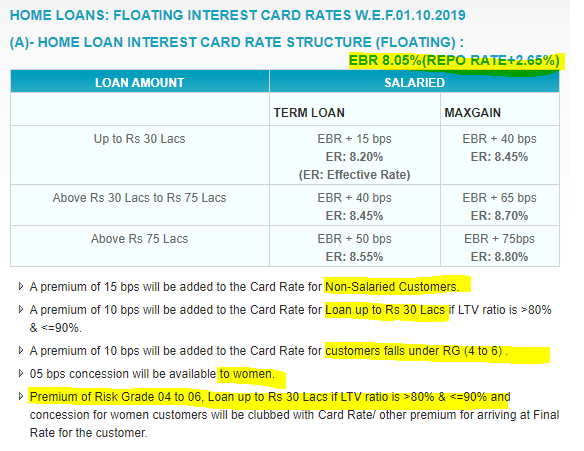

So, RBI has now mandated that

w.e.f 1 October 2019, all Commercial and scheduled banks to link their loan

interest rates to some external benchmark, which could be Repo rate, Treasury

bills rate (3M/6M) or any benchmark rate published by the Financial Benchmarks India Pvt. Ltd.

If the benchmark is external then banks will not have any

control or influence on the lending rates movement. All this was done to

effective and faster transmission of rates to the consumer, which was not

getting possible in the current MCLR rate regime which was started in 2016.

External benchmarking – How does the Borrower be impacted?

All new borrowers of Floating Home loans may find the change in their EMIs or tenure every 3 months. As in the Repo rate linked loan, your loan interest rates will be frequently impacted, with the announcement of RBI.

For now, given the current Repo rate i.e. @ 5.15%, one can expect a lower bank loan interest rate. And if RBI brings it further down than the loan rates will also be impacted and will further go down.

Banks have been asked to reset interest rates under external benchmarking at least once in three months. Resetting means reviewing the rates keeping in view the benchmark rates. In the existing MCLR rates system, some banks even have 1 year Reset clause and some 3 months. So, now this resetting procedure and tenure have also been standardized.

It is important to understand that the actual Interest rate will be higher than the benchmark. Banks just have to link their loan rates to some external rate, so any changes in the benchmark may be applied to the loan rates on reset.

But Banks are Free to charge “spread” to cover up its cost, risk, and profit margin. And these spreads may vary with a different set of borrowers, having different credit ratings, loan requirements, type of loan, etc. The Spread will vary from bank to bank.

Also, banks are allowed to change the Risk premium portion in the spread for a specific set of borrowers if their credit rating changes substantially.

As published in Economic times (10.10.2019):

“Under the new external benchmarking regime, Bank of Baroda, for instance, will be using three credit score slabs from the Credit Information Bureau (India) Ltd (Cibil) to price new home loans. Customers with high credit score, defined in excess of 760 out of a maximum 900, will pay 1% lower interest compared with those reporting scores in 675-724 range — the lowest score slab at which loans will be offered.”

But, please note that this applies to only floating-rate loans. Though other loans like auto and personal will also be impacted but the rate at which borrower has borrowed the money will remain fixed for the entire tenure in case of fixed-rate loans, whereas for floating-rate loans, the rate will go up and down depending on the RBI decision and other benchmarks which banks will follow.

Rates may go up also. Yes. Do not consider the rates to go down only. This is not a one-way street. If current rates are looking attractive to you than here is the word of caution. The current repo rates are at a multiyear low. So, if tomorrow RBI starts hiking the key policy rates, then that will also impact you, and your loan rates may also go up. And thus, increase your cash outflow.

Repo rates have a quite volatile past, see the 10-year chart below:

source: tradingeconomics.com

External benchmarking applies to bank loans only. This change applies to bank loans only, and not to NBFC provided loans, like HDFC Ltd or LIC housing finance, etc. Though market forces and competition may lead them to rework their lending rates, for now it is not mandated for them.

This applies to only New borrowers. The Borrowers going for a home loan, Vehicle loan or personal loan after 1st October 2019, will get loans on Interest rates linked to external benchmarks, but old borrowers will not be switched to this new rate structure automatically. They have to apply to the bank, pay the administrative or legal cost to the bank and then banks will switch them to new structure.

Should the old borrowers move to External benchmarking linked loans?

Firstly, the borrowers need to understand that today’s rate may look attractive, this is going to be more fluctuating since the reset will happen at least once in 3 months (as per the contract with the bank). Rates today are the result of a slowdown in the economy, but going forward if you see revival and high inflation, then RBI would try to control the money supply by increasing the repo rates, which will impact your borrowing cost too.

Secondly, before moving to the new rates you have to do some maths, to find out if there is actually going to be some saving for you or not. You should consider the Outstanding Loan amount; Outstanding Loan tenor; Interest rates differential; and Expenses (like switch fee, processing charges, filing charges etc.), to see if at all they should move to the new rates or not. Check out my article on MCLR where I have shown how you may do the maths.

Conclusion:

This has to happen someday. RBI’s job is to manage the money supply and growth, in the economy through the banking network, and if its decisions do not get transmitted to the ultimate consumers then how would it do its job properly.

This is quite an old issue and RBI has tried in many ways to manage it by tweaking the formulae of banks’ lending rate calculation, but now with the external benchmarking be it through Repo rates or Treasury bills, RBI has kind of linked all the loans to the market forces. This, in turn, has also nudged banks to review the deposit rates, as with lower lending rates they would not be able to continue with high deposit rates for long.

All these changes though are bringing transparency in the financial system, but it also is making your deposit and borrowing rates more volatile. And requires you to have more hold onto your cash flows, and thus a better and structured financial planning and regular reviews.

If you have any questions, opinions, experiences to share, please feel free to use the comments section below.

{kind=link}