There have been a lot of events happening in the debt markets lately, ranging from the downgrading of papers issued by IL&FS, DHFL, Yes Bank, etc., to the shutting down of 6 debt schemes of Franklin Templeton Mutual Fund.

These events have made investors, as well as financial advisors (including me), wary of debt mutual funds that invest in low-rated papers or have a higher credit risk.

Such circumstances have led many investors to search for safe options in debt funds.

Also read: Types of Debt funds

But safety comes with low yield, which worked well in the falling rate scenario but nowadays with no scope of more rate cuts, due to rising inflation, and G sec rates going quite volatile, it is getting difficult to give an idea on the short term tentative yield on debt returns.

To answer this, mutual fund houses came out with Target Maturity Funds. These are passive or index debt funds, which mimic the holdings of an underlying bond index. And as the name suggests these have a specific fixed maturity date, which helps in understanding the expected yield from the scheme.

Let’s talk about these funds in detail in this article.

What are target maturity funds?

Not only in the equity funds, index or passive funds are now also available in the debt funds space as well, these are called Target Maturity Funds.(Read: How attractive is passive investing in India?)

These are open-ended funds that invest in Central and State Government bonds, mimicking the composition of an underlying index, like- NIfty SDL, Nifty PSU Bond, etc. The idea is to generate a return similar to that of the index and not try to beat it.

The USP of these funds is that the yields are predictable. If you hold the fund until its maturity, the return would be quite predictable i.e. Yield to Maturity of the fund less expense ratio.

Also read: All you wanted to know about expense ratio in mutual funds

The maturity period of every fund scheme is pre-defined (generally 6-8 years) as indicated in its name and is similar to that of the bonds the fund has invested in.

These funds follow a natural roll-down strategy where the overall maturity of the fund falls every day, month, and year and nears zero as the maturity comes closer. For example, a target maturity fund maturing in 2027 will have a 6-year maturity now, 5-year maturity in 2022, and thus would be reduced to zero in 2027.

This strategy helps reduce interest-rate risk as the maturity of the fund rolls down every year, protecting the portfolio from the interest rate movements in the economy.

Although the yields may fluctuate for the short-term if the interest-rate cycle reverses during the term of the fund, if held till maturity the impact reduces and the fund generates a similar return as indicated.

Also, as these funds are passive in nature fund manager risk is eliminated and the expense ratio is low as well.

These funds currently invest only in Central or State Government Securities, or AAA-rated bonds of Public Sector Undertakings, that way the Credit Risk of the fund is negligible as well.

Also read: Types of Risks in investments & how to manage them?

How are these funds different from Fixed Maturity Plans?

You must be thinking that most of the features of the targeted maturity funds are similar to those of the Fixed Maturity Plans, which were very popular some years back, especially among the HNI investors with a conservative risk profile, as a tax-efficient alternative to Bank Fixed Deposits. (Read a detailed article on Fixed Maturity Plans)

Like Target Maturity Funds, FMPs too hold the securities until maturity and the scheme maturity is similar to those of the securities. We may say that these funds are successors to FMPs. But, there are three major differences between Fixed Maturity Plans and Target Maturity Funds, as listed below:

- FMPs are close-ended. Investors are allowed to enter the scheme, only at the time of launch and would pay back the capital along with the interest only after the stipulated maturity, until then the funds remain locked-in the scheme. Unlike FMPs, target maturity funds are open-ended. Existing investors are free to redeem their units, and new investors can also enter into the scheme.

- Target maturity funds offer better liquidity than FMPs. In Fixed Maturity Plans, investors get back their invested amount only at the time of maturity, not in-between. Whereas in Target Maturity funds investors can redeem the amount before maturity at the prevailing NAV of the scheme, thereby being more liquid and flexible.

- FMPs are generally launched with a tenure of 3-5 years, while target maturity funds are launched with a longer tenure of 6-8 years.

Target Maturity Funds- Taxation:

The taxation of targeted maturity funds is similar to any other debt mutual fund. If held for more than 3 years, the gains on the scheme would qualify for the long-term capital gains and would be taxed @ 20%, post indexation. However, w.e.f 01.04.2023 the tax rules on debt funds / Non equity funds have changed, and since then no indexation advantage is available for investments purchased after said date.

Also read: New Debt fund tax rules

Any gain on debt investments purchased after 01.04.2023, will be considered as short term capital gain and the same will be adeed in your total income and taxed as per slabs.

Also read: Taxation of Mutual Funds In India

So, now you will find a Re investment risk on the schemes of target Maturity funds which will be maturing post 01.04.2023.

Target Maturity Funds- Options Available:

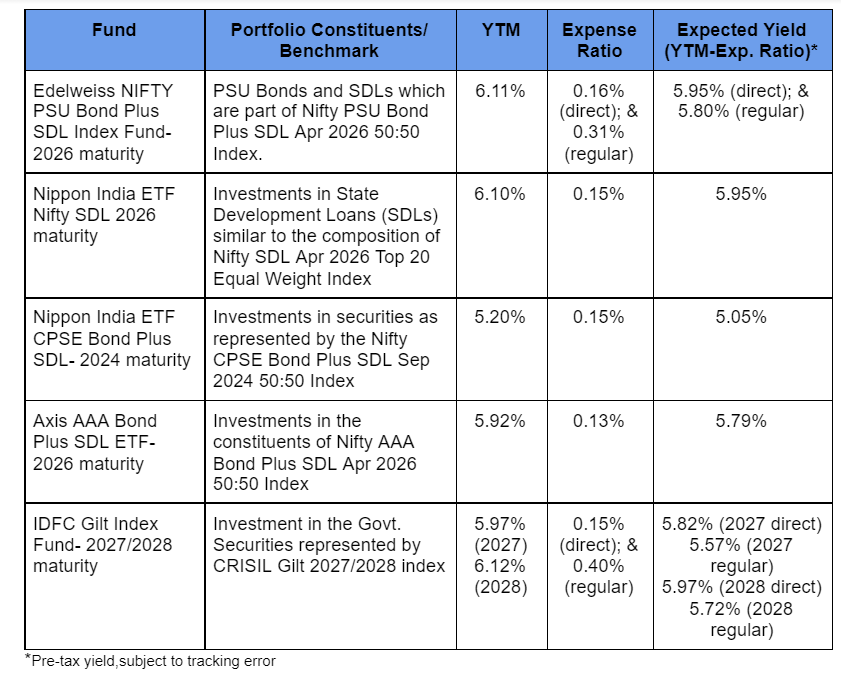

As listed in the table above, Edelweiss NIFTY PSU Bond Plus SDL Index Fund (2026) and IDFC Gilt Index Fund (2027 & 2028) are index funds and the rest are ETFs. With some MF houses, you may also get fund of funds with these ETFs as a base, but in that case, the expense ratio may be high.

Target Maturity Funds- Should you Invest?

As mentioned above, target maturity funds come with a lot of advantages. These funds invest in high-quality securities, majorly Govt. bonds or PSU papers rated AAA or above, that way credit risk is minimum which means the safety of capital is ensured.

Passive structure means low expense ratio and fund manager risk is also eliminated. Decent and predictable returns and tax efficiency are like icing on the cake.

However, it is also important to note that yields are too not 100% guaranteed. These are subject to tracking errors and may fall shorter than the benchmark.

Also read: How mutual fund benchmarks help in selecting the right fund?

The returns may also get impacted by the interest rate movements during the term of the fund. Unlike the active debt funds, where the fund manager changes the strategy when the interest rate cycle turns by accumulating higher coupon bonds, which may not be possible in target maturity funds.

In the ETF structure, liquidity would also be an added concern. You may not be able to withdraw your investment in case you need the money back (although not recommended).

So, if you are satisfied with returns in line with inflation, with the safety of capital being the topmost priority and can stay put with your investment till maturity, target maturity funds can be a part of your debt portfolio.

Also read: What is Inflation & its impact on your financial plan

It can also be used to fund a medium-term goal with the requirement being in line with the maturity period.

For big investments and people under the highest tax bracket, these can be a good alternative to Bank Fixed Deposits, to park their surplus money.

Also read: FD interest rates are rising in 2022- looking attractive again?

Also read: Should you invest in G-Secs through the RBI Retail Direct Gilt Account?

This article on Target Maturity Fund is written by Mr. Varun Baid, CFP professional

{kind=link}