These days I am getting many mails from my blog readers asking for my views on newly launched LIC insurance products. Some of them want me to write a detailed review on the same. I respect and accept their request and will be doing review of some of the products . But before going ahead it would be better to understand why the new products are getting launched. Why LIC and other insurers have discontinued their existing range of products and what’s new (in general) in the new ones.

All insurers are coming up with new products to comply with the guidelines issued by IRDA in February 2013. These guidelines want insurance policies to be more transparent and comprehendible to the policy holders. Along with this IRDA through these regulations wants insurers to come up with more flexible products. Many Insurers have already announced their new range of improved products in last year. But LIC launching new products is obviously gaining attention of many and the reasons are also very obvious.

Below are some of the important changes in insurance plans meant for Individuals:

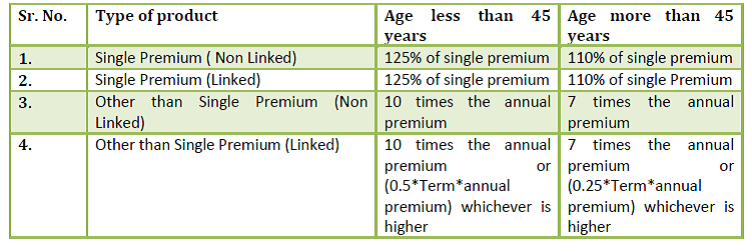

- Minimum sum assured : IRDA has specified a Minimum sum assured which each product of its category should offer.

One interesting change is announced in the suicide clause which used to say that nothing will be paid if insured commits suicide within 12 months of inception of policy. As per the new regulations, in case of Non Linked plans – in case of death due to suicide, within 12 months from the date of inception of the policy, the nominee of the policyholder shall be entitled to at least 80% of premium paid. And in the case of linked policies, nominee will get 100% of policy fund value.

For policies issued on the life of minor the date of commencement of policy and date of commencement of risk should be same.

2. Service tax

IRDA guidelines stipulates that service tax shall not be included in the contractual premium and shall be collected from policyholder separately over and above the premium. Till now LIC has been paying the service tax amount from its earnings which indirectly reduces policy holder’s bonus amount, but 1 jan 2014 onwards the Service tax amount has to be charged from policyholder directly.

3. Surrender Value clause

This is the most important change that’s coming up in the new non linked traditional policies. Unlike earlier when surrendering the plan in between the policy term costs a lot, the new guidelines are in customers’ favor. As per the new guidelines, the surrender value of the life insurance policies will be linked to the premium paying term . Where the premium paying term of the policy is 10 years or more, it will acquire guaranteed surrender value after payment of 3 consecutive premiums. And where the Premium paying term is less than 10 years, then guaranteed surrender value will be acquired after payment of 2 consecutive premium payments. The Guaranteed surrender value in case of regular premium policies will be as follows:

- 30% of premiums paid when surrendered between 2nd and 3rd year of policy.

- 50% of premiums paid when surrendered between 4th and 7th year of policy, where the term of policy is 7 years or less than 90% of premiums paid if surrendered in last 2 years of policy term.

- Surrendered value beyond 7 years shall be the factor of premiums already paid and possible asset shares on such products. Will be mentioned in the policy document.

The Guaranteed Surrender value in case of single Premium Policies will be as follows:

- 70% of premium paid if surrendered with in 3 policy years.

- 90% of premium paid if surrendered in 4th and 7th Policy year

- Surrendered value beyond 7 years shall be the factor of premiums already paid and possible asset shares on such products. Will be mentioned in the policy document.

In the case of ULIP plans, there is no surrender clause but a discontinuation clause. One cannot withdraw/surrender the policy before completion of minimum 5 years tenure, but can discontinue paying premiums. Many ULIP plans has already been launched as per the new guidelines, read there review here. HDFC life pension super plus , SBI Life Smart Power insurance

4. Benefit disclosures

Customized illustration to be provided to customer buying the policy, which illustrates the guaranteed and No guaranteed benefits at a rate of 4% and 8% respectively. Earlier these rates were 6% and 10%. This illustration should be signed by policy holder and will become part of policy document.

5. New Mortality rates

Policy premiums especially of LIC may get reduced, as the cost towards the mortality charges will come down. IRDA has made mandatory for all insurers including LIC to use the new mortality table rates. This will surely but marginally affect the LIC policies premiums as it was using the old table till now with high mortality costs.

6. Agent’s commission structure

There are some changes announced in the agent’s commission structure also, which seems to have reduced considerably. You may go through the IRDA gazette to have a look at the new structure. It has been linked to premium paying term now. Higher the term, higher will be the first year commission.

7. Furnishing account statements

This is not a product specific change but an added advantage among others. Now it has been made mandatory by IRDA to send Statement of Policy account to policyholder at least once a year. This will give idea to the policyholder as to the status of the policy. The statement will cover complete breakup including Opening balance, Premium received, deduction towards charges, bonus accrued etc.

After understanding the above mentioned major changes announced in Traditional Policies it will be easy to understand and compare what different new policies offer. The above mentioned features are standard ones which all the companies have to add in their products. I am also attaching the complete IRDA gazette here, if someone wants to read the guidelines in detail.

IRDA Gazette (16 feb’2013) for Linked Insurance Policies

IRDA Gazette (16 feb’2013) for Non Linked Insurance Policies

{kind=link}

Nothing has been stated about medical health insurance.

Rakesh the article is about life insurance policies only.

Hi,

I bought new Term Insurance from HDFC Life. After accepting their excess premium amount and paying it on the spot, I received email saying your policy is accepted and an attached policy document.

It is also mentioned that this policy is not enforced till i get physical document. I just wanted to know if there is any rule imposed by IRDA for issuing physical policy document?

They are saying it will take Month to issue the physical document. Now i want to understand, why i am not getting cover for 12 months and one month is wasted in sending physical document?

Please advice.

Regards,

Anand

Anand, you have also raised one very valid point, but there’s no rule imposed by IRDA on issuing of Physical policy documents.You may go through the attachment which has been shared on your mail, if there’s any date of commencement of risk mentioned or not. If the date is there then technically your risk cover should start from that date, but if HDFC has specifically mentioned that policy will be enforced only after issuing physical document then we have to go by company’s words.

I think that IRDA should also work out a system of ASBA ( Application Supported by Blocked amount) as in case of MF NFOs or IPOs. Why these insurance companies earns interest on the premium amount for which we are not sure whether we will get cover or not?

Hi, can you please clarify about the guarenteed surrender value clause.If my policy has 15 yr and 21yr terms whatwill be the % if 4 premium (annual) have already been paid.Lic policy bought in2010.

These new rules are applicable to the policies issued after 1st january 2014. Due to these new rules all insurers had to come up with new products which should comply with the new guidelines. Since your policy is 4 years old, so it does not apply to you.

Sir, I seek your clarification on risks covered by Life Insurance Policies. Can any Company issue a policy covering death by only few selective risks such as Heart Attack, Dysentery etc., (I have not yet studied the IRDA guide lines of February 2013) Because, the Sarva Suraksha Policy covers only5 causes for death such as 1) First Heart Attack of specified severity; 2)Open Chest CABG 3)Stroke resulting in permanent symptoms; 4) Cancer of specified severity 5) Kidney failure requiring regular dialysis. Which means that the Bank is not liable to pay in case of death by other causes. And I am sure, since most of the Policy Holders are borrowers of huge amount of housing loans, they will not read and understand the policy conditions. Is this legally permitted.

No, Life insurance policy cannot put such restrictions. I guess the Sarva Suraksha policy that you are referring to, must be a Critical Illness policy

Hi I m Vishwas from Mumbai,

I have bought Term plan from Bajaj… I have applied the same before my birth date i.e. 11th April and paid the premium. Now before issuance they are asking for Extra premium as they are saying bcs of birthdate. As per my understanding premium should be charged based on last birthday..

Please help.

This sort of case happened with one of my clients too. If the policy was proposed by you well before your birth date, with all the formalities like medical happened before that date and the delay was only in the issuance of the policy then you may write to the grievance department of the insurer to get the premium revised

Hi I m Vishwas from Mumbai,

I have bought Term plan from Bajaj… I have applied the same before my birth date i.e. 11th April and paid the premium. Now before issuance they are asking for Extra premium as they are saying bcs of birthdate. As per my understanding premium should be charged based on last birthday..

Please help.

Hi ,

Please could you explain about suicide death clause as my banker told me that even suicide is covered and whole 1 CR term plan insured value would be paid ….Asking for sake of knowledge…Not otherwise so that could correct her so she could get corrected…

Do life insurance policies like sbi shubh nivesh for 20 yr and 15yr term will hav to pay any tax on maturity sum.We hav started these policies from 2016 and sum assured are 1200000 and 330000 respectively.We pay the premium yrly.

Taxation depends on the Premium amount and the sum assured you have in the policy. Started in 2016, your premium should not be more than 10% of the Policy sum assured to make it a tax-free one on maturity.