These days LIC has been launching new products almost every alternate day. The reason of coming up with new products is the new IRDA guidelines announced in February ’2013 which all the insurers have to comply with till or before 1st January 2014. LIC’s new products honor the new guidelines. Among the latest product launches, LIC has come up with the 3 new versions of its LIC money back plans. LIC money back plans are among the most popular plans of LIC, but financially speaking the costliest product in its range. Now has the new guidelines brought any change in LIC money back plans for customer’s benefit or not that has to be seen. Let’s review the plans in detail

LIC Money back plans new version – in short

LIC has announced 3 new LIC money back plans under the new guidelines of IRDA.

- LIC New money back plan – 20 years (15 years Premium paying term)

- LIC new money back plan – 25 years (20 years premium paying term)

- LIC’s new BIMA Bachat – Single Premium Plan

The names may sound familiar, but the products have been revamped. I will be doing review of LIC money back plans regular premium (20/25 years).

Money back plans as the name suggest are the plans which pay back some fixed amount after every specified intervals out of the basic sum assured. Being an endowment and participating plans, it will also announce regular bonuses depending on the profitability of corporation. Also being an insurance plan, it offers a risk coverage / death benefit.

As LIC website says – “Money back plans offer an attractive combination of protection, against death throughout the term of the plan, along with periodic payment on survival at specified durations during the term. Thus LIC Money back plans offers 3 benefits:

Death benefit, Survival benefit and Maturity benefit.

Death benefit in these policies are as per the new IRDA guidelins. As per LIC money back plans death benefit is the sum total of “Sum assured on death” along with all kind of bonuses declared. “Sum assured on Death” is defined as higher of 125% of basic sum assured or 10 times of annualized premium. This amount should not be less than 105% of total premiums paid.

Survival benefit: in case of 20 years policy – 20% of basic sum assured will be paid at the regular intervals at the end of each 5th, 10th and 15th Policy year. And in the case of 25 years policy – 15% of basic sum assured will be paid at the regular intervals of end of each 5th, 10th, 15th and 20th policy years.

Maturity benefit: This benefit will be comprised of the balance amount of basic sum assured not paid in previous years ( 40% ) along with the bonus amounts if any.

Bonus amounts will be as per the LIC’s profitability and experience.

Insured may also opt for Accidental death and disability benefit rider by paying extra rider premium.

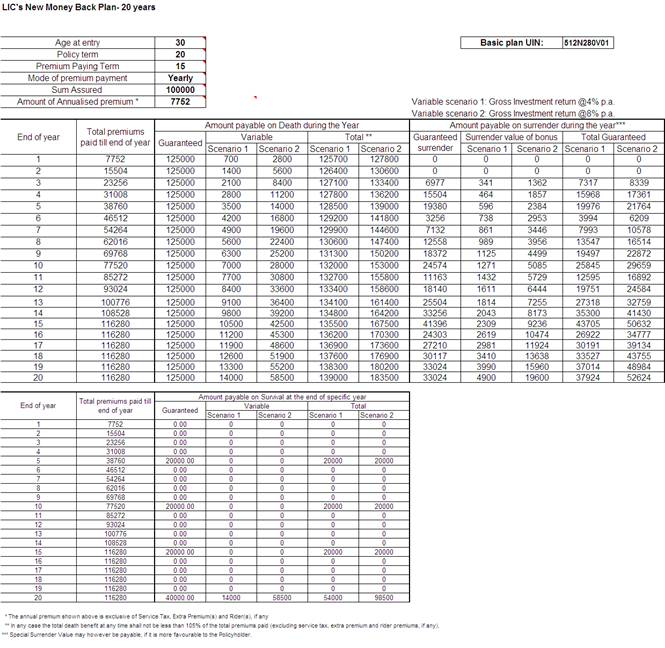

LIC Money back plans – Illustrations

Below is the illustration from LIC money back plan 20 years (new) taken from LIC website (click on the image to visit lic site). Do note that in this illustration premiums are exclusive of service tax. Now onwards LIC will charge service tax over and above the basic premium. (Read : New rules by IRDA)

The above calculations are on the basis of assumed return of 4% and 8% of the net investible premiums (i.e premium after deducting all the applicable charges). IRR (Internal Rate of Return) in case of 4% comes out to be almost negligible and in case of 8% as 3.97% p.a. When service tax gets adjusted to premiums the IRR will surely come down.

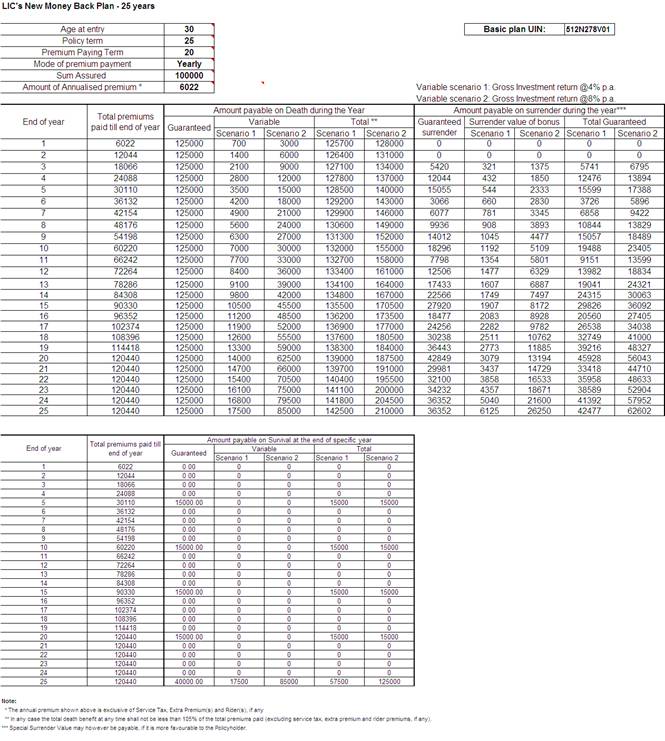

LIC Money Back Plans – 25 Years- illustration

The above calculations are on the basis of assumed return of 4% and 8% of the net investible premiums (i.e premium after deducting all the applicable charges). IRR (Internal Rate of Return) in case of 4% comes out to be almost negligible and in case of 8% as 4.34% p.a. When service tax gets adjusted to premiums the IRR will surely come down.

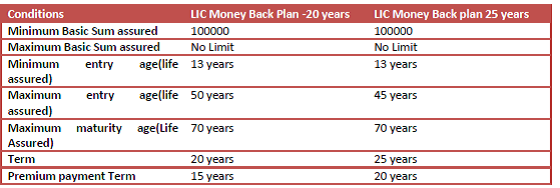

LIC money back plans – Other features

There are some eligibility BASIC conditions in these LIC money back plans

LIC Money back Plans – Should you invest??

The good part in these new plans is that the surrender value factor has been clearly mentioned in the product features. Now one would not have to run pillar to post to get to know his policy surrender/paid up value, and with these transparent features one can easily estimate what one would get on surrender or continuation.

The returns will surely vary after consideration of services tax, age and different rebates (on Mode of premium and sum assured)which LIC is offering along with. The illustrations generated at the time of product pitching or buying will give tentative idea as to what should one expect in particular case. Do ask for illustration from agent and check what IRR will be generated in your case. Tell your agent to calculate IRR for you or mail your illustration to us, we’ll do it for you. You may be told by the agent that corporation is making profits and the bonus amounts will improve going forward but looking at the distribution expenses and other costs associated with endowment plans I believe that you will get tentatively the same or less amount as would be mentioned in the illustration.

My view still remains the same. I don’t advise to mix investment with insurance. I am sure you don’t invest to get the surrender or paid up values and neither you want your investments to generate 3-5% of return in this high inflationary economy. If you have investment horizon of 20-25 years with you there are many different good options available in front of you. For Insurance covers go with pure term cover which is cheapest form of insurance. Keep your investments simple and flexible.

The LIC Money back plans, even in the new avatar sounds like old wine in new bottle. My advice – AVOID

{kind=link}

Sir please note that as per circular no 7/2003 dtd 05/09/2013 CBDT has clarified in para 10.3 of the circular that in an event where the procceds are insurance are not exempt under section 10(10D) , its only the amount in excess of premium paid.(excluding premium paid)

Thanks for sharing Mr Shenoy. Well, this thing need to be probed now, since what you’ve shared is quite old info with mention of section 88. After coming up of section 80C many things got changed. I will get back on this…after consulting with some tax experts and fellow planners. If you get more info then please do share.