ICICI bank I wish is a very interesting recurring deposit product of ICICI bank available for its saving bank account customers who use internet banking.

The interesting part of this flexible rd product is you can create and manage your short and long term goals (in terms of money you want to accumulate) with these savings and also can share it with your friends and family on Facebook.

By sharing it with others you can also ask for their contribution in this deposit to help you achieve your goal or fulfill your wish faster.

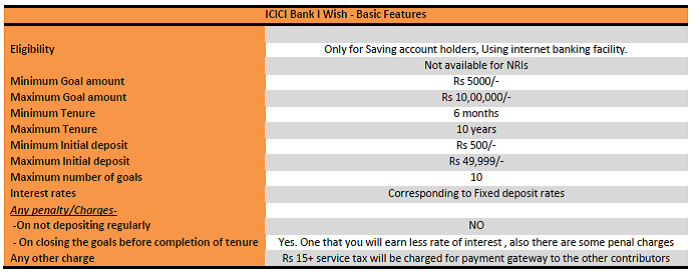

The uniqueness of this recurring deposit is the feature of flexibility. Unlike regular recurring deposits , in this flexi rd there is no compulsion on the part of the depositor to make a month on month contribution into it. You can also make multiple deposits in a particular month. This product can only be invested through internet banking. In this article, I will be covering the basic details of “icici bank i wish fexi rd” and try to figure out the pros and cons of this.Basic Features of ICICI bank I Wish

This is a recurring deposit product with a feature of flexibility in deposit. Its interest rates would be equivalent to what icici bank offers in other RD products.

To bring excitement in your savings, it has an option of Creating and Naming a goal. For e.g. you may want to buy a camera costing Rs 30000/- after a year. You can name your goal as “Camera”, tenure as 12 months and after adjusting to the interest rates, portal will calculate how much you need to save per month towards that goal.

The flexible feature of ICICI I wish recurring deposit allows you either to put a standing instruction for regular deposits or transfer the funds as and when you have towards this goal. You may also share your Goal/Wish on your Facebook account and ask for contribution into this to your friends and family. Other features are as below:

Should you invest in ICICI Bank I Wish?

Well, structure wise it’s definitely a unique product.

It is a fact that when you map your savings towards a goal, you become very much disciplined in your approach. And nothing can match the excitement of achieving the goal. The

The flexible aspect of this recurring deposit is also very attractive. But the major drawback of ICICI I wish is that this is a recurring deposit product which by its basic nature is taxable. Whatever you earn out of this saving will be added in your income and taxed as per your slab.

I mean if the intention is to save for a short-term goal, why not to use alternate options like liquid/short term mutual funds. For short term goals, these mutual funds may not be comparable on taxation aspect (due to changes announced in budget 2013) but these funds will definitely provide you with better returns than recurring deposits. (read: bank deposits vs debt funds)

Secondly, the penalty charges on pre closure of icici bank i wish account are also a negative factor. This issue can also be answered by investing in liquid/ultra short term mutual funds as there are no penal charges of withdrawing the amount.

ICICI bank I wish can be a perfect product to inculcate discipline of savings among your Kids especially major kids (Above 18 years of age). They can be encouraged to save part of the pocket money for their goals (of going on vacation or buying costly gadgets) from their own pocket money and once that benchmark is achieved you can supplement that savings with your contribution.

This way you can teach them the advantage of savings by allocating it to a particular goal and also it will not burden you with more of tax payments. As whatever earnings made on the savings will be treated as your Child income only, also the gift made by you to him/her will not attract any gift tax. (Read : tax planning tips)

What are your views on icici bank I wish recurring deposit? Does this flexi RD attract you? Share your views in the comments

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Hi, In my view “i-Wish” doesn’t cover the fundamental of disciplined saving . It is not better than saving through regular RD. Anyways some minor flexibility it does provides but as far as I think it is of no use. On the other short term saving instruments I am still not sure about the use of MF over Debt deposits.

Gaurav, this is a normal RD product with flexibility in deposits. Its upto the user how he wants to use it…through regular deposits or irregular. I have shared a link in the article where you can see the comparison between debt mutual funds and bank deposits. You can have a look at that.

Hi,

just wanted to know, on goal completion can we transfer the amount to the linked savings account or is it a physical procedure like getting a cheque or something???

Good article.. Thanks for sharing!

Thanks Sid.

On goal or tenure of RD completion you can transfer the amount in your linked savings account.

Nice article. Thanks for sharing..

I want to know that suppose let it be I wish my goal amount to 50,000.. could I save more than this 50,000 in the same goal?

As per bank terms its not possible,but you can create another Goal.Once goal amount is reached you cant add extra amount to it.Wait for tenure to complete and en-cash.

Thanks Pradeep. It was a great help! anyway another simple doubt. What if I could not reach my goal amount in the specified tenure?

Hi,

How long will it take for the goal amount be credited to the account on closing or on pre-closure?

As it is a normal recurring deposit product, so i think it should not take more than 24 hrs. Infact 24 hrs is also a long time for this.

does anyone has any experience of hidden charges\deductions?

As I see in the site itself its written, “On pre-mature withdrawal of the deposit:

– interest will be calculated at the rate applicable for the period the deposit has actually remained with ICICI Bank”

I am afraid by the words ” rate applicable”.

Does it mean if the rate is 7.75 for 6 months, on premature withdrawl at 3 months we get prin +7.75 % for 3 months?

Or is it at icici’s decretion :S

Shruti…there’s nothing hidden, but you have to read everything 🙂

rate applicable is the rate for the tenure for which deposit has remained with the bank. If for 6 months deposit rate is 7.75% and for 1 year rate is 10%, and you kept the money for 6 months only, then you will get 7.75% p.a for 6 months, means effectively 3.875%. Rates mentioned are always on annual basis.

A very good Article!!

Is the amount taxable?

Yes, it is. ICICI Bank I wish is taxable like a normal recurring deposit

is that possible to take loan from the amount?

What is process of after completion of tenure.

Will the amount automatically transferred to my account or I need to manually request for it in the ICICI bank branch?

Ankush you have to request for the closure. You can do it online too

Hi,

Suppose I deposit 10,000 in the starting of first months and 20,000 in the starting of 2nd month. Tenure period is of 12 months. So, will I be getting the interest of 10,000 for 12 months and on 20,000 for 11 months?

Goal amount is the maturity amount or the principal amount? If it is the maturity amount, will we be notified the pending amount to be deposited every month to reach the goal?

Mr Ahuja

I have not used this product personally, but i can answer this question based on how recurring deposit works.

Yes, you will get interest of 12 months on Rs 10k and for 11 months on 20k. Bank will pay interest for the complete tenure they have used your money given for.

I guess, goal amount is the maturity amount (i.e. Principal Plus interest).

Mr Ahuja , If you are really serious on investing in this product, then you may raise such queries to icici bank customer care or even visit any Branch. and share your experience and feedback of the product here for the benefit of other readers.

Mr Singal, Firstly this article was good. Just wanted to ask as you said that interest will be paid on the tenure bank uses your money, so will it be day-wise calculation?

I mean if I put 5k on 10th January, so will i get interest from 10th January?

Technically Yes. You earn interest from the day of deposit.

Sir,

I have open iWish Flexible Recurring Deposit now I want to transfer money from my saving account how can i transfer.

Pl. suggest

Naresh, Pls contact icici bank customer care for your query

Just go to manage goals, in that “add funds”. Then select your source account & click add.

Hi,

what if we don’t deposit the target amount within the specified time? example.. if target amount is 50k and have to deposit it in an year but wasnot able to deposit that much then what will happen?

HI Singal ,

Wven i have same concern what Miss soumya had. if we don’t reach the gaol amount in targeted tenure . what will be the situation. we will get any charges or interest or not able to withdraw ?

Please advise .

Thanks

Dinesh

No there are no charges. You can withdraw whatever you accumulate.

HI Singal ,

Even i have same concern what Miss Soumya had. if we don’t reach the goal amount in targeted tenure . what will be the situation. we will get any additional charges or interest or not able to withdraw ?

Please advise .

Thanks

Dinesh

Hi,

The question comes here what is the % of the taxable amount on the RD? Suppose if any individual has a goal of Rs 500000/- in 2 years and they achieve the goal with the interest amount, let see it around 547000/-, then how much amount should be deducted (taxable amount) and how much and how much an individual will get.

Is there any % of the taxable amount ?

Does the tax also applicable on the interest earned amount or the total amount?

Regards, Sanat R

Tax will be on the interest income earned. Interest earned in one financial year will be added in your income and taxed as per IT slabs you fall in. This is a recurring deposit only with different features.

sir, suppose we deposit RS. 10000 on 17th of any month then how much interest will we get means will we get interest for whole the month or only for remaining 13 days of the month or no interest during that month??

You will get interest for the remaining 13 days.

IF i dont meet my Goal amount than with will happen ??

Hi, I am NRI, holding both NRO and NRE account with ICI. I heard about I-wish and I am pretty much intersted in this flexi deposit plan.

My question:

1. Is NRE account holder cant open this I-wish deposite?

2. May I know some better plans for short term saving, for example 5 years(installmnts 5k to 10K)

I closed iwish goal prematurely. When will my money be credited??

These days it is best not to trust banks with our hard earned money.

Why do you think so?

Mai apna goal dicide karti hu I wish scheme me 2 lakh one year ke liy aaor mujhe need hho jjaay 10 month pr hhi to Kya Mai aapne paaisse Pahle nikal ssaakugi and interest rate Kya hoga mean kitne milgge

Currently, the RD interest rate is 5% for a one year deposit. If you withdraw prematurely, proportional interest would be received.

How I can track my iwish account details…I not able to check where is my money saved and how much.

You may do it through the ICICI I mobile app. If you face any issues, please contact the ICICI Bank customer care.