For most of you investments to save tax are the only investments that you could be able to make in a single year. Reasons are many like low income, large number of dependents, high expenses, bad financial habits etc. Look out the 3 cases below which are real life situations as shared by some of the readers. All 3 persons are from different backgrounds but have same requirements.

Navdeep kaur’s (21) annual income is Rs 4.5 lakh. She contributes in her family expenditure and gives a fixed sum of Rs 20000 every month to her parents. After keeping some amount for her personal expenses she could be able to spare around a lakh per annum .She asked guidance to invest this amount in the best possible way for her long term security.

Randheer Singh’s (28) annual income is Rs 6 lakh, but has 5 dependents on him including his parents. After providing for the basic family expenses, he could not be able to save much. He wanted to start his saving with some investments that can help him save on his Income taxes, grows his money to achieve goals, and also provides safety of return. He knows the maximum limit of Rs 1.50 lakh and would try to spare at least that much from his surplus.

Mukesh (35) though earns in 7 figures but due to some medical issues in family and also due to his bad financial habits (Credit card loan, personal loan, car loan), is unable to focus on his long term goals. Seeking my advice to plan investments for tax saving which may suit his long term needs too.

Since all of these people have almost the same requirement, so I decided to write a complete detailed post on this subject to save tax the financial planning way or how to derive maximum (not only returns) from Section 80C investments for tax saving.

Before going ahead, let me first quickly take you through the various options available for tax saving under section 80C.

Investments options that comes under section 80c covers medium and long term products like – Public provident fund (PPF) , Equity Linked saving Scheme (ELSS), Life insurance policy Premiums, New Pension scheme (NPS), Employee Provident fund (EPF), 5 year bank fixed deposits, National savings Certificate (NSC), Pension products from Insurance companies/Mutual funds, Senior citizen saving scheme, Subscription to notified deposits or bonds like of HUDCO or NABARD.

There are few expenses also as notified under section 80C which qualifies for tax saving , but in this article we’ll discuss only about making the best use of tax saving investments under section 80C for long term goals achievement.

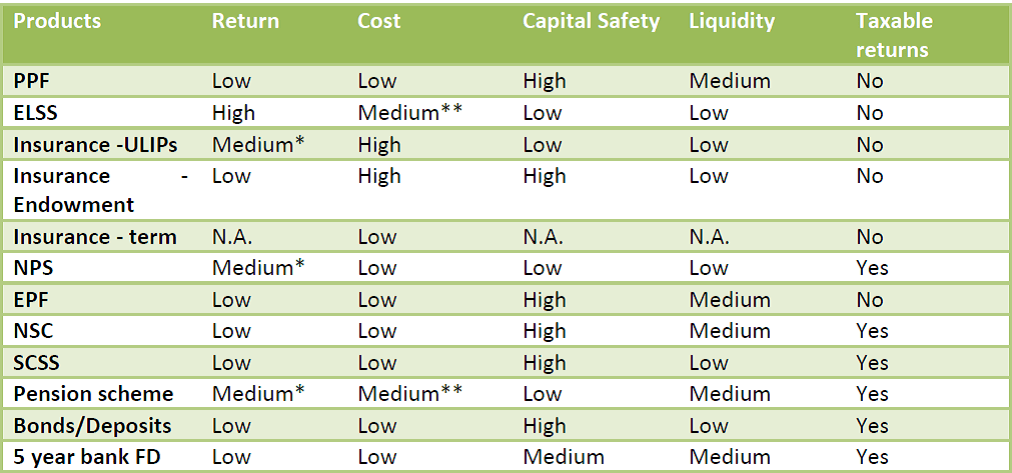

Categorization of tax saving products to save tax under section 80c

Returns: Equity linked products are categorized under High return category, and where the investment allocation of product is hybrid or optional with investor is categorized as medium. Products having a fixed rate of interest will generate low returns.

Cost: If there’s some cost attached like Fund management expenses, or administrative expenses etc. then that product is categorized under Medium to high. Products with ZERO cost are under Low category. (Read more on Investments products related expenses)

Safety: The one with guaranteed and fixed returns are considered as safe products and those which are market linked or partially guaranteed are under low to medium.

Liquidity: Generally products that offer tax saving have low liquidity, but still there are some which offers partial withdrawal or can be taken loan on some conditions those have been put under Medium liquid products.

Taxation: Though all products mentioned above provide income tax saving while investing, but for some of these returns generated are taxable in nature.

Now when you have understood the products and factors on which you have to select products to save tax, you should zero on to your requirements/needs. As per the requirement of Navdeep, Randhir and Mukesh, they wanted to have long term portfolio suitable to their financial planning needs. What I can figure out from their profile is that they have financial dependents on them, they are young and don’t have any near term requirement of money and thus have long term view on investments. So this kind of profile people should invest in below mentioned tax saving investments:

- Start with Life Insurance Policy: When there are financial dependents on you, the first thing that you need to do is to secure their future, by making yourself adequately insured. This will ensure that your dependents will be taken care of financially even in your absence.You may get advise from your banker or some insurance agent to put money into ULIPs or endowment kind of product, and looking at the structure of these products you also might get tempted too. But when you have limited resources available at your disposal and you want to make the best of them then you should go with low cost and easy to manage options. So keeping things simple you should buy Term Life Insurance Policy, which will provide you with decent cover at low cost. This will result into liquid surplus available which can be invested as per the risk tolerance and goals targeted.

You should also consider buying health insurance policy too which will take care of your savings in case of medical emergency. The Premiums paid towards health insurance will provide tax saving u/s 80D of income tax act.

- Public Provident fund: PPF is a best investment option which provides you safety along with tax free returns. Being a fixed return investment, this will bring the necessary safety and low volatility in your investment portfolio which saves tax also. You may open PPF account in your name or in the name of your child. This way you may allocate some portion of your savings to your child’s future and take advantage of tax saving yourself.

PPF has a minimum lock in period of 15 years, but can be partially withdrawn after a particular tenure. (Read more about PPF here)

- Equity Linked savings Scheme: After getting adequately insured and investing for safe returns, you should also invest part of the money in the equity linked products to provide the growth Push in your portfolio. Equity is a volatile asset class but will only bother you in short term. In the long term it has potential to generate exponential return which on one side beats inflation and on other multiplies your portfolio for future.

ELSS has a minimum lock in period of 3 years, which is the lowest in the tax saving products category but it should never be invested for such low time frame. Always invest in equity for more than 5 years, if you really want to benefit out of it.

Check out the best Mutual funds to invest in 2014-15

Products like Employee provident fund also works in the similar way as PPF but has some withdrawal restrictions in it. Moreover EPF is a compulsory saving which gets deducted from your salary, so you may want to balance the allocation in PPF accordingly. For e.g. you decide to invest 50% of savings after buying insurance into safe long term product, and you already have invested some portion into EPF, then for balance you may go with PPF. Choose the allocation between safe and volatile investments as per your risk tolerance and your goals targeted.

The word pension also attracts to some, but i believe that at accumulation stage every thing works the same and one should consider the low taxation and inflation beating returns with adequate liquidity.( Read : Retirement plan or pension plan?)

If the investment requirement is for short term then you may have to accept the taxation of returns and chose products like bank Fixed deposits or national savings certificate. But if you can clearly define your requirements, then you may be able to take advantage of partial withdrawal feature as available in PPF/EPF and keep your returns tax free.(Also Read Tax Planning case Study)

Conclusion:

Financial planning is about arrangement of finances to help you achieve your long and short term goals comfortably. Financial planners do take care of the taxation in your investment portfolio and make sure that your portfolio generates decent returns that should beat inflation. The products like PPF and ELSS will definitely come under long term portfolio advisory for any financial planner.

Tax saving investment Products that comes under section 80C serves all purposes of investors. You can use different products for different time frames and for different risk appetite. If your investment resources are limited, then allocating money in available products, can serve your tax saving requirements along with overall financial planning too. Though here it is assumed that when your resources are limited, your requirements are also limited, otherwise no arrangement could be able to satisfy your needs.

Financial planning is not only about investments, but still if you start investing in these products early in your life and start investing as per your goals and requirements, you are already on the way to financial betterment.

Are you one of those who invest only for tax saving? how do you find the suggestions above? Do you agree that PPF and ELSS are the best products to invest in to save tax under section 80c. Do share your views.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Which is better – IFO or the running?

Mutual funds new products are termed as “NFO- New fund offer”.

It is always better to go with experienced and running fund as it has seen all kind of market movements and emerged as clear performer after managing through volatile market movements. So in my view Running fund is always better to invest in.