Rahul was very happy while working in a multinational organization. He remains out of the country for at least 3 months in a year for official purposes, which he considers an officially paid vacation.

He has got all the benefits and perquisites provided by his company. He lives in employer-provided accommodation, drives employer-provided vehicle. His pay package is also very decent, in fact, more than decent for a bachelor like him.

But Last month when I went to meet him, he was looking worried and depressed. On asking the reason he showed me his salary slip and pointed towards the Tax figure that is being deducted out of his Income.

To add to it he told me that his Chartered Accountant is saying that he needs to deposit some more tax on the income generated out of his investments.

This made me think that this is not only his concern. Everyone who’s earning well wants to save maximum tax possible.

The moment one starts earning start looking for the ways to save taxes. And why not, after all the money you retain as a result of tax saving can earn more money for you. Money saved is money earned.

Though you can’t save on every tax penny, yes through intelligent tax planning you can save a lot of taxes.

There are 4 rules in Tax planning which if followed prudently in different stages of life; you will save considerably on taxes.

A) Spreading the Taxable income among various family members.

B) Taking full advantage of tax exemptions available.

C) Taking full advantage of Tax deductions available

D) Optimum use of Tax-exempted income.

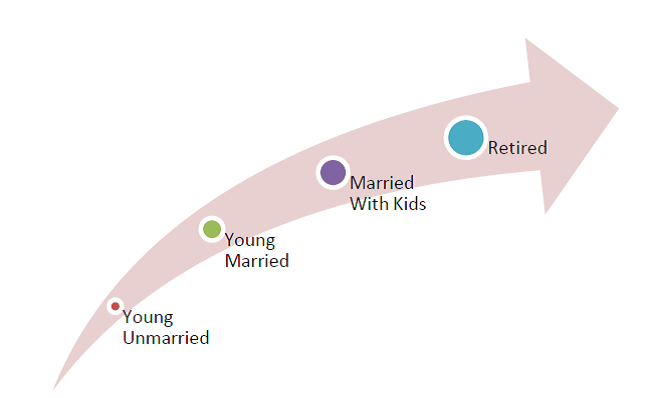

Keeping the above rules in mind, I have figured out some tax planning strategies to save tax for different life stages, which I will be covering in the series of articles. It is not necessary that all of this, you can apply on you but it is for your basic understanding which you can discuss with your employer and tax consultant and to find the suitability of these in your financial profile.(Read more: Tax offender case study)

Tax Planning strategies for Young Unmarried

This is the time when one has started off with his Job and financial life.

This means that there is only a single tax file to take care of. This is the stage we always stress on people to think of long-term and start saving, as the expenses are generally very less at this stage unless one has already burdened self under Loan.

Following are some of the ways one can save income tax through tax planning.

1.) Negotiate with your employer on the changes in the breakup of your salary structure. There are many companies which ask the employees in April to design the salary structure themselves suitable to their individual financial profile. They call it as Flexible benefit plan.

Make the most this opportunity. Sit with your planner, CA or any other Tax professional and find out what amount of HRA benefit is suitable for you, what should be the different allowances that can be added to this breakup. (Read: all you want to know about House Rent Allowance)

You may also ask your Employer to start contributing to New pensions Scheme on your behalf to reduce your in hand salary and thus helps in tax saving. (Read: All about New Pension scheme)

2.) Invest the maximum amount allowed for tax saving u/s 80C and 80D, and other permissible sections. Section 80D is for health insurance. Even if your employer has provided you with some coverage it is advisable to have a separate cover. (Read: don’t ignore health insurance)

3.) Invest in tax-efficient instruments only like Employee provident fund, Voluntary provident fund, Public provident fund, Equity linked Mutual funds etc.

Though Insurance plans also give tax-free income I will not advise to invest in Insurance plans due to the basic structure of those products. If you do not have any financial dependent, practically you do not need any life insurance cover.

If at all you have to buy any insurance policy, better to go with term insurance plans. (Read: Best Investment options)

4.) If you are in a habit of giving donations or charities than do take the receipt of that amount. This will also help in saving taxes u/s 80G.

5.) If you want to save for your near-term goal which is not possible through EPF/PPF/Equity funds or any other Tax free investment option for that matter, then it’s better to gift the amount to your parents or sister or any other family member who comes in the lesser tax bracket and invest through them.

If you are worried about the management front, then don’t worry there are lot many other ways to keep control on that.

6.) Don’t let your taxable income increase by keeping the amount in your saving bank account and bank fixed deposits. Just keep the amount required for an emergency in your saving account, for all other parking of funds use Debt mutual funds and select as per your short and medium-term needs.

Many people would be of opinion that if you have the good income you should go for home loan kind of products to help you save tax and create assets, but I do not think that would be wise. I would advise youngsters to avoid any kind of loan till they become disciplined with their savings and expenses.

As I always say that Tax planning and Financial Planning should go hand in hand, so whatever you do for tax saving should support your long or short-term goals.

In the coming articles, I will be sharing the Tax planning strategies for other life stages like for newlyweds, Small Family with Kids, Post Kids’ marriage and own Retirement. So keep watching the space. (Also Read: tax planning tips for couple with Kids)

Do share if you have any other tax planning strategies to save tax at this Young life stage. It will be beneficial for readers.

{kind=link}

Dear Manikaran,

A gr8 article !Can you explain more abt gifting to parents for saving taxes

Thanks Krishna. From tax planning point of view if you want to invest some thing in a taxable instrument then rather than investing in your own name, you can gift that amount to your parents(if they come in the lower tax bracket) and thus transferring the taxation aspect in their name. Gifting to parents would be tax free in their hands and also it does not attract any clubbing of income. But better to chk with a tax professional before doing such transaction to find out suitability in your profile.

[…] the topic “Tax Planning for different life stages.” In the earlier 2 articles I have covered –Tax planning Tips for young person and Tax planning Tips for young married couple. It’s better to read all the articles in […]

[…] article is in continuation to the previous one (Tax Planning at different Life stages – I), where I have discussed the various ways where a young person can save his tax outgo by using the 4 […]

hi

i am giving half of my monthly salary to my parents in FY13. how can i make it help in tax saving?

Hi pankaj

Gifting money to your parents will be tax free in the hands of parents and if they generate any income out of it than that income will not be clubbed in your income, which if invested in you name would have been increased your tax liablility.

There’s one more way to get some tax benefit out of this arrangement. If you are a salaried employee and recieves HRA as a part of salary and the house you are living in belongs to your parents then this payment to parents can be showed as a rent arrangement and you can claim tax benefit on HRA. But please note then this payment will be added into the income of your parents.

Dear Sir,

I wanted to purchase a house property, plz advise me, i have individual, huf and my wife file as tax paying assessee. how should i structure the purchase so as to avail maximum income tax benefits for myself, wife as well as in huf and also be eligible for bank loan. As i was told by the bankers that if the property is in the name of HUF loan will not be sanctioned.

Also can i avail similar benefits on purchase of a commercial property.

Kindly advise me by mail

Ramesh JP

Ramesh, the best way would have been if your HUF have enough capital to but the property. In that case you and your wife can take loan from HUF and claims tax benefit u/s 24 for the interest payment.

But now when this is not possible, then its better to buy property in joint ownership ( you and your wife) and also as you both have separate tax files then you both should be a co borrower of the loan and pay EMIs jointly. This way you both can enjoy tax benefit u/s 80C and U/s 24.

No such benefits are there on purchase of commercial property

Hi,

If we borrow from HUF it will inturn become the income of HUF and morever the HUF will not be entitled to claim 80c and interet paymen 24 benefits.

But in that case HUF will not be able to avail the 80c and interest payment benefit. What if I make the HUF along with myself and my wife as co-owner, and myself and my wife as co-borrower, can then all three can get the benefit of 80c and interest payment.

If i am right, HUF is also entitled for benfits of 80c and interest payment in addition to Husband and Wife as individual, under income tax act. But the banks or FI do not give loan to HUF. So plz advise me in what way documentation should be done or procedure be followed, for purchasing the property or in between the husband, wife and HUF, to avail the benefits by HUF.

And also by co-owner you mean we 2 or 3 should be party in a single sale deed or can we also execute separate sale deed in each name for a particular portion or extent of the property.

plz advise

thanks & regards

Even if the interest payment becomes income of HUF it will help you in 2 ways. One no cash flow will go out of family and second you can still claim tax benefit u/s 80C. HUF can also save u/s 80C, it can buy ELSS or do 5 years bank deposits to save taxes.

As HUF can’t get loan , so it can’t avail any kind of benefit available in housing loan.

Making HUF co owner will only complicate the ownership, so not at all advisable. and when it is not a co owner then it can’t take housing loan benefit even if bank accepts it as co borrower.

Why to have separate sale deed when you are buying property along with family members? better to have single sale deed.

[…] you should properly use the provisions available in Gift tax and create separate tax files in familyhttp://goodmoneying.com/tax-plan…Embed QuoteWritten just now. 1 view.Upvote0DownvoteComment Loading… Write an answerRelated […]

Sir ji ,Namaskar. I am central govt employee . My spouse is house wife .we both file IT returns . I have 3 houses in my name. 2 have given on rent .one is for our resident . How can I show rent in my wife’s earning . Moreover ,I am going to receive 5 lakhs from my wife’s brother . Is it taxable .?

Rent will be counted in the account of the owner only. You cannot transfer the income, but Assets. You may gift the property to your wife, then the rental income will be hers. But in this case, you have to bear the stamp duty and other transfer charges.

If your brother in law if gifting you, then it is not taxable. Just take the money by cheque and it’s better to take one letter from him that he is giving you money under love and affection, mentioning both of your Pan number on the letter. This is just for records if sometimes IT authorities ask for this.