If you are a debt fund investor, you must have received an SMS from your fund house at the beginning of this month stating the Potential risk Matrix of your debt scheme. This message cautioned many investors and queries started pouring in on what this is all about.

Does this mean that the Otherwise stated “Safe” or “Comparatively Safe” Asset Class, now has risk into it? And how to select debt schemes based on this matrix?

How does Risk-O-Meter different from this Risk matrix?

I have answered briefly to them, but now I thought to write a detailed post on this subject for the benefit of our readers.

What is the Potential Risk Matrix in Debt Mutual Funds?

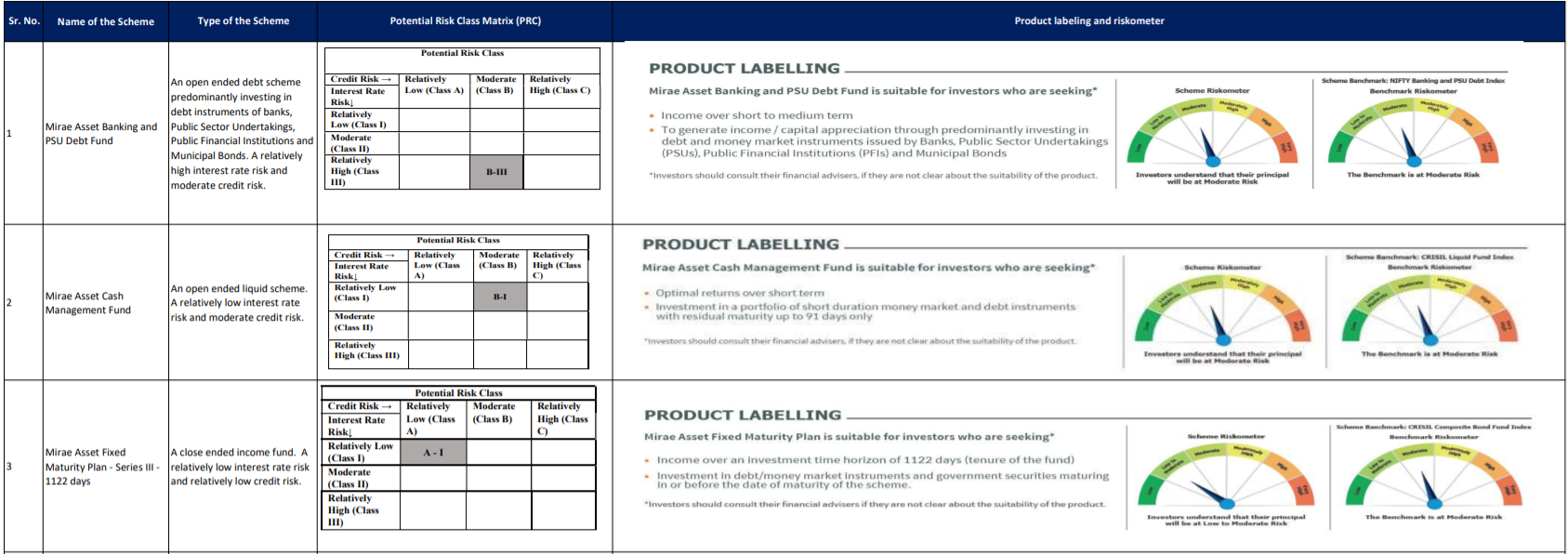

Let me start with the Actual SMS that Investors got. This one from Mirae Asset Mutual Fund

“This is to inform you that in accordance with the SEBI Circular no. SEBI/HO/IMD/IMD-11 DOF-3/CIR/2021/573 dated June 07, 2021, on ‘Potential Risk Matrix for debt Schemes based on Interest Rate Risk and Credit Risk’, the Potential Risk Class Matrix (PRC) for Mirae Asset Cash Management Fund is B-I i.e. A relatively low-interest rate risk and moderate credit risk.

For detailed disclosure, click here- shorturl.at/muCJK

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

When you click the link, a document appears, which looks like this-

According to the above circular issued by SEBI in June 2021, AMCs must disclose the “maximum risk” a debt scheme can take – both credit risk (from holding risky papers) and interest rate risk (from holding longer maturing papers). As soon as this is established, the fund needs to be sure not to exceed it. (Also Read: How to manage debt fund risks in an investment portfolio?)

An AMC must inform you if its holding has moved to a higher risk category than that stated in the potential risk matrix. This would imply a fundamental change to a fund, calling for an exit option.

The deadline given to fund houses was December 1’2021, the reason you received such a message.

Post recategorization of the mutual funds, though SEBI has given a demarcation on the type of funds (Short/Medium/Long/Corporate Bond/Credit Risk etc.) still there is some overlapping. (Also Read: Types of Debt Mutual Funds)

Like- What if one likes to go with a Short term fund, will the papers be highly rated or risky ones?

What about Corporate bond funds? What would be the duration of the papers in the portfolio?

Though in the beginning, you may check the Fund fact sheet, what if the fund house changes the portfolio tomorrow which may impact the overall riskiness of the portfolio, and which if disclosed at the time of investment you may not be comfortable taking it.

So, this Potential risk matrix came into the scene. But do remember that this is “Potential” and may not be actual. This is the maximum risk a debt scheme may take.

How to Interpret Potential Risk Matrix of the Debt Mutual Fund Scheme?

Let’s understand this with an example of Mirae Banking & PSU Fund:

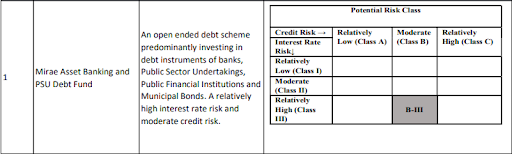

The Potential Risk Matrix depicts 2 major risks that a Debt Mutual fund has i.e. Credit Risk and Interest rate risk.

Credit Risk comes from the Credit Rating of the Invested Securities, and Interest rate risk comes from the Macaulay Duration (MD) of the scheme. (Also Read: Types of Risks in Investment and how to manage them?)

MD in simple terms is the Sensitivity of the portfolio to the Interest rate movement. Higher the MD, Higher would be the Volatility in the portfolio due to interest rate movement.

In the Interest rate Risk column as shown in the above image/matrix, there are three Classes. Each class has a different Macaulay Duration.

- Class 1 – MD is less than or Equal to one year

- Class II – MD is Less than or equal to three years

- Class III – Any MD

You can see in the case of Mirae Banking & PSU debt fund, the classification of Interest rate risk is Class III. It means that the fund can keep any duration/maturity of papers. It has chosen to be flexible, so as not to take your approval every time the fund manager chooses to go for a long duration portfolio or reduce the duration later on. (Also Read: How to select debt funds in volatile interest rate scenario?)

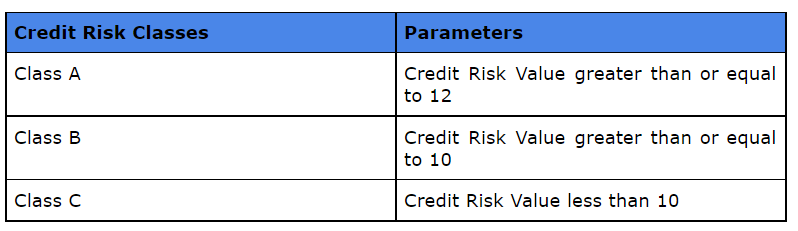

Let us now look at the Credit Risk or the Default Risk that is derived from the credit quality of the papers the fund has.

For this Potential Risk matrix, SEBI has come up with 3 classes of Credit Risk, as explained below:

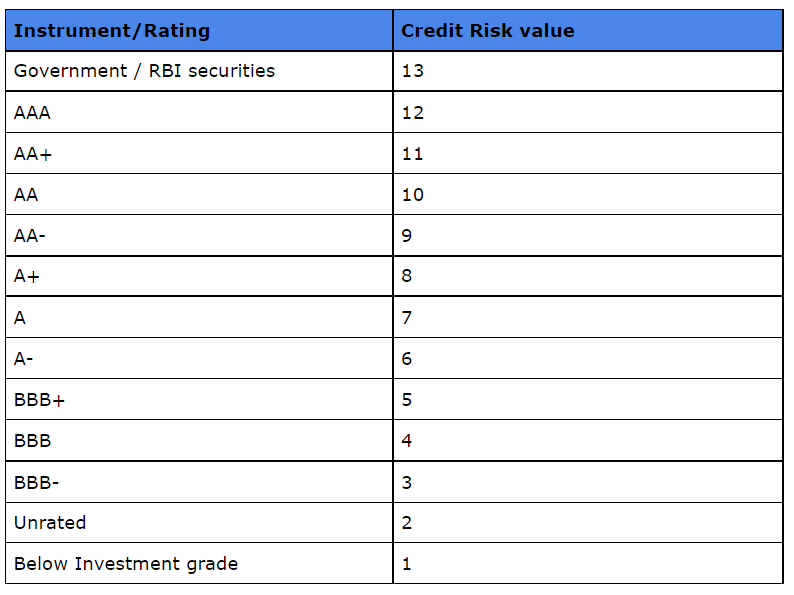

Now we need to check the values assigned to each Credit Rating. The safest instrument/rating has the highest Credit Risk Value and the instrument carrying the maximum credit risk is valued the least. The below table explains the same:

Revisiting Mirae Banking & PSU Potential Risk Matrix, you will see that it is classified into B Risk Class. This depicts that the fund will take the exposure to only AA & Above securities, and will not go below AA-rated papers.

The overall rating of B-III says the fund could go with High-Interest Rate Risk and Moderate Credit Risk. Please remember that it does not say that at this moment, with the current portfolio, the fund house is following this approach, but this is the maximum Risk the scheme can take.

How to make use of the Potential Risk Matrix?

Here comes the confusing part. These kinds of changes are good to appreciate, but practically quite difficult to make use of. Now when you have Risk-o-meter, also at a place that may show a different risk grade of the fund, the selection becomes more difficult.

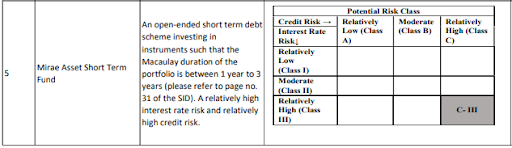

Let’s take Mirae Short term fund. Check the Risk Matrix and Risk-O-Meter below:

When you look at both these tools separately, you will find that when the Potential Risk Class of the fund is C-III ( High Credit Risk and High-Interest Rate Risk), the Risk-O-Meter says the Risk Grade is “Low to Moderate”.

The difference is that C-III is the potential risk which a Fund house may take, and Risk-o-Meter tells the current risk the fund house has taken, after accounting for Interest rate, Liquidity, and Credit Risk. (Read more on Mutual Fund Risk-o-meter in this article)

So, it may not be wise to select or exit a debt fund based on a potential risk matrix, which is good for the understanding purpose on the maximum level of risk a fund scheme may take. But to select, retain or exit a fund, you better access the portfolio composition and do a periodic review. Risk-O-meter may also help as it is reviewed on a monthly basis. (Also Read: When is the right time to exit your investments?)

You also have to be in touch with the current interest rate environment, so to take the duration call of the scheme.

All in all, these tools require regular reporting from the fund houses which may keep them on toes, but from an investor’s perspective selecting schemes on the basis of any single one of them may not be wise.

{kind=link}

I think one can just look at Yield to Maturity in order to understand the risk in the debt product. Higher it is than a simple FD, more risk that particular fund is taking.