LIC has come up with a new child plan with name LIC Jeevan Tarun. Whatever the product is, I love the way LIC name all its policies. This post is a review of this new LIC jeevan tarun policy.

LIC Jeevan Tarun is a participating endowment child plan, with a structure of money back plan. Plan is structured in such a way that one can map it with requirement of children and use the money back amount for education needs. Though there is also one option of taking the entire benefit on maturity and thus one can use this plan as normal saving instrument too. But does this plan make sense to invest in to make your child future ready? Let’s try to figure this out.

LIC Jeevan Tarun – in Brief

LIC Jeevan tarun is a limited premium, participating endowment plan, designed to meet the educational needs of growing children through annual survival benefit from ages of 20-24 and maturity at age of 25 years. However there are different options in which investor can chose different survival and maturity benefits as per the requirement.

Survival benefit would be the annual fixed percentage of sum assured which will be paid in the first 4 years of benefit period and in last installment the balance left along with the vested simple reversionary bonus and final additional bonus will be paid

Being an Insurance policy there’s death benefit too. Insurance cover will be given to the Child.

LIC Jeevan Tarun – Benefits

Death Benefit-

The life assured in this particular policy would be the child. In case life assured is of less than 8 years of age, then the risk will commence either after 2 years of starting of policy or on first anniversary if life assured attains required age within the policy term.

Benefit before commencement of risk– All premiums paid (excluding the taxes, extra premium or rider premium) will be refunded back

Benefit after commencement of risk– in case of death during the policy term, in an inforce policy, sum assured on death along with vested simple reversionary bonus and final additional bonus if any shall be payable.

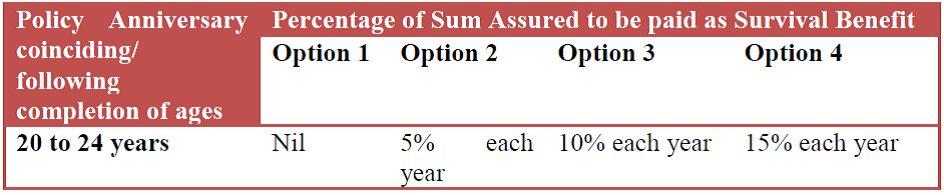

Survival benefit-

A fixed percentage of sum assured will be payable on each policy anniversary , coinciding with or immediately following the completion of 20 years of age for next 4 years, as per the option chosen as below

Maturity benefit:

It depends on the option chosen for survival benefit. In this the balance sum assured left after deducting survival benefit, plus the vested simple reversionary bonus and final additional bonus (if any) will be paid

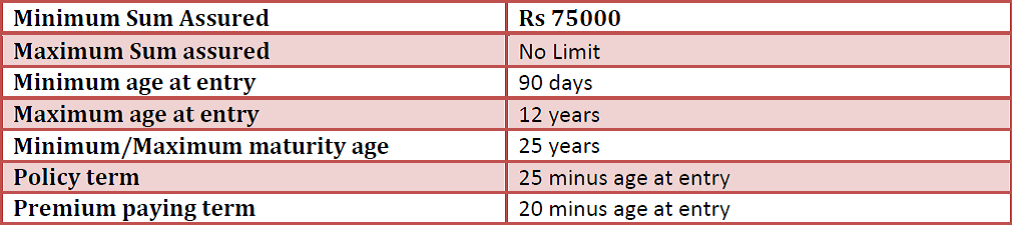

LIC Jeevan Tarun – Eligibility Conditions

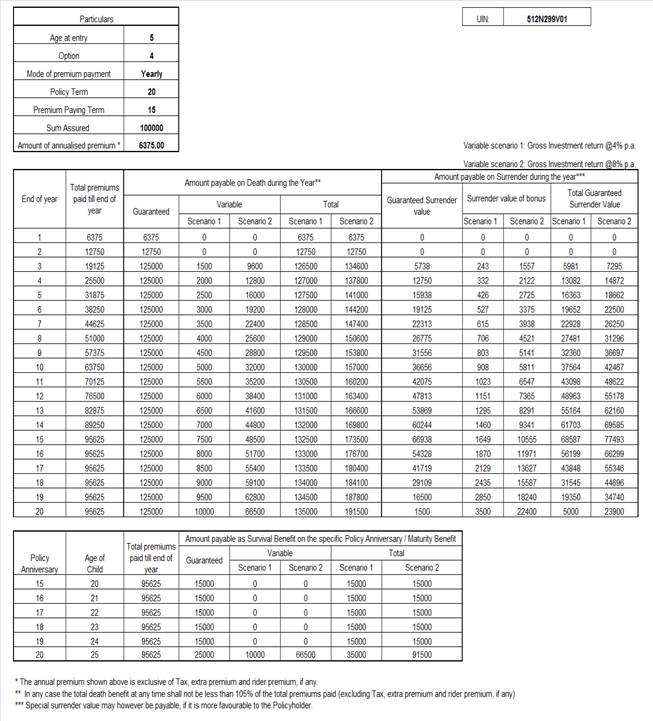

LIC Jeevan Tarun – Benefit Illustration

From the illustration as shown on LIC website it can be easily derived that @4% assumed return the IRR would come as less than 1% and @8% assumed return IRR would be around 4%.

Do note that in the illustration premiums are exclusive of service tax, which once applied will further reduce the return. Though one may argue that for high sum assured and yearly mode of payment there are some discounts on tabular premium, but I don’t think that will bring any special change in the returns.

LIC Jeevan Tarun – Should you invest?

Insurance policies have lost innovation. There’s no USP left in any of the insurance product except the attractive names and emotional touch like Child plans, pension plan etc.

The feature of giving life assurance to the kid in itself is not encouraging. Why would the child need insurance cover? May be to reduce the mortality expenditure and to push the returns, but I don’t see that push in the illustrations.

There’s one optional waiver of premium rider for the proposer (parent) who pays the premium. This is to keep the policy continuing in case of untimely death of proposer. This again has a cost attached. Though it is optional, but if not taken the policy will go lapse if something happens to the proposer, as with no regular payments policy will go into paid up status.

Other thing which restricts me to advise any insurance cum investment plan is the structure itself. As this plan is meant to support children education expenses, so assuming a 10 year old child would need Rs 100000 per annum to support education when he will be into college. Now the way inflation is rising and in education it is somewhere 10% plus, so this 100000 would become Rs 2.60 lakh. Now to get Rs 2.60 lakh per annum in LIC Jeevan Tarun option 4, sum assured should be around Rs 17.50 lakh. This would require annual premium of around 1.77 lakh per annum.

After looking at the returns and just to make sure the regular payments, would you yourself like to put your money in this product? Don’t you think PPF would be a better option? Even if you are not an equity person, which is very much suitable to this time horizon, then also I think even FD’s Post tax returns will serve your purpose and that too with sufficient liquidity.

To me LIC Jeevan tarun is a clear NO NO policy. Neither for insurance, nor for Investment.

How do you find the review of LIC Jeevan tarun? Do share your observations or query if any.

{kind=link}

Seems like people are looking for child education investment products these days. This is LIC’s 2nd child policy this year. People should think 10 times why they are buying a child plan to build education corpus for their child.

Jeevan tarun is yet again a new policy with old typical features provided by LIC of India.

Regarding Life insurence there are lot of talks everywhere. But insurence for a woman life is always given a 2nd priority. Here my concern is related to that matter only. Considering the tenure of a woman work life, which is mostly obstructed by factors like marriage, kids, family management, what can be the options for them to make their life insured. I am not sure if this is a right place to ask this question, but still if you could answer it, would be great.

Very valid point raised gaurav. GoodMoneying is definitely the right place to clear any of your personal finances doubts and also speak your mind and share your ideas.

See, the purpose of life insurance is to cover the financial responsibilities of the insured in case of his/her untimely demise. When there is some financial dependent on a woman she should also take adeqaute insurance cover and she will comfortably get it.

But in case of Home makers there are some restrictions as she doesn’t have any financial dependent and also any earning. What she’s offered with is 50% of the insurance cover her husband is having.

Sometimes we as financial planners do look at the financial angle and if required advice clients to take insurance cover for home maker spouse too.

But practically if there’s no financial dependent, no life insurance is required.