There were not many expectations from this budget. I mean it’s just 5 months back the same government had presented its Budget (though Interim), so it was likely that Finance minister will not announce anything major this time.

But still, looking at the state of economy some statements or viewpoint on the painful areas like slowing down of economic growth with a major impact on the auto sector, the Unemployment situation in the country, NBFC Crises, Banking defaults, etc, were expected.

Government has not completely ignored them and addressed the issues in its own way.

The feeler came from the budget speech and reading the Finance bill was that government thrust is more on the broader economy and bringing the Long-term Capital into the country and thus announced reforms to streamline some processes to make things easy for NRIs, Foreign Investors to bring FDI in the country. Which is good for long term growth and Stability of the country.

Banks are going to be Recapitalize with Rs 70000 crores to boost credit. Banks have been given with a Partial Guarantee to take over good quality loan book of NBFCs

Announced some provisions on Income Tax filing rules and proposed to come up with Prefilled tax forms which will cover the salaries, interest income, and Capital Gains. Government has shared its intention to come up with faceless e-assessment of ITRs which may soon be launched in Phases

Making it mandatory to file Income tax returns for some certain persons entering into High-value Transactions

It has also announced some measures to promote the Less cash economy, and thus announced TDS @2% on Cash withdrawals of Rs 1 crore and above from a bank account.

Corporate tax at a lower rate of 25% has been extended to companies having a turnover of up to Rs 400 crore (the limit was earlier up to Rs 250 crore)

Below are some of the proposals presented by Finance Minister in the Budget 2019 impacting Personal Finance.

Budget 2019 and Personal Finance

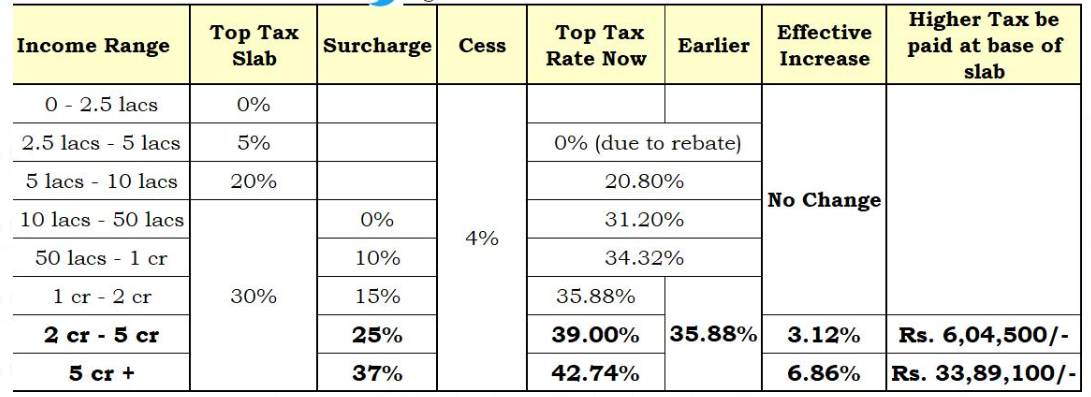

- Increase of Surcharge on the Total Income

While calculating Income Tax, Surcharge of 10% of Income-tax amount be levied on the assesses having an income of Rs 50 lakh and up to Rs 1 crore. For Income above Rs 1 crore, the surcharge percentage increases to 15%.

In Budget 2019, the Finance Minister has announced 2 more slabs:

A) A surcharge of 25% on total Tax for the Income above Rs 2 crore to Rs 5 crore.

B) A surcharge of 37% on total Tax for the Income above Rs 5 crore.

2. Additional Rs 1.5 lakh exemption on Home Loan for Affordable Housing

It is Proposed to Insert Section 80EEA to provide additional Tax incentive on Interest payment towards the home loan. With the conditions as below:

A) Loan to be sanctioned by a Financial Institution between 1st April 2019-31st March 2020

B) For the House valuing Rs 45 lakh

C) To the person buying the First House

This amendment will take effect on 1st April 2020

3. Tax exemption on Buying Electric Vehicle on Loan

To encourage people to buy Electric vehicles and further improve the environment and reduce pollution, a new section 80 EEB has been inserted which will give Tax deduction of Rs 1.50 lakh on the interest paid on Loan taken to buy Electric vehicles. This is w.e.f.01.04.2020, as you have to have electric vehicles available first in the market to buy.

4. Pan and Aadhar be made Interchangeable

W.E.F 1st September 2019, to ensure ease of compliance, it is also proposed to provide for inter-changeability of PAN with the Aadhaar number.

Accordingly, the provisions of section 139A are proposed to be amended so as to provide that, –

(i) every person who is required to furnish or intimate or quote his PAN under the Act, and who, has not been allotted a PAN but possesses the Aadhaar number, may furnish or intimate or quote his Aadhaar number in lieu of PAN, and such person shall be allotted a PAN in the prescribed manner;

(ii) every person who has been allotted a PAN, and who has linked his Aadhaar number under section 139AA, may furnish or intimate or quote his Aadhaar number in lieu of a PAN.

In short, PAN is mandatory, but if you don’t have it, for the time being, you may quote Aadhar number. And if you have your PAN and Aadhar linked, then you may quote any of this for the prescribed transactions.

5. TDS on Life Insurance Policy proceeds

Government has cleared a big doubt by making this change. Now the TDS on taxable Life Insurance policies i.e. where the proceeds are not tax-free u/s 10(10) D, will be deducted at 5% rather than 1% earlier, And this TDS will be deducted on the amount which is actually taxable i.e. Surrender/Maturity Proceeds less the premium paid.

Earlier since it was being deducted on the complete proceeds so there was a complete confusion on the taxable portion of the Policy.

6. Mandatory furnishing of Income Tax Returns:

If the Person enters into specific below mentioned transaction then the ITR filing has been made compulsory even if his/her total income does not exceed the maximum amount not chargeable to Tax i.e. Rs 2.50 lakh/ Rs 3 lakh / Rs 5 lakh

A) If the person has deposited an amount or aggregate of the amounts exceeding Rs 1 crore in one or more current accounts of the bank;

B) If the person has spent Rs 2 lakh or more on self or another person, for travel to a foreign country

C) If spent Rs 1 lakh or above on the consumption of Electricity

Concluding Remarks

This was called a Modi 2.0 Budget. The budget was clearly about the future priorities of the government. Though Finance Minister calls it a Gaon, Gareeb and Kisan Budget, but to me that feeling did not come at all.

It has addressed the areas like Attracting capital, tried to address the Pain points like banking and NBFC, but still something like Electric vehicles tax incentive when there is no such Vehicles and its Infrastructure at place, Aadhar for NRIs (not sure why), affordable housing benefit when prices still are not in the range of affordability are the things which are beyond my understanding.

I believe that every government works with good intention only and for the benefit of Citizens. And calling every year achievement and comparing it with “till 2013” should stop as its high time to come up with some concrete steps and let the growth that they want to show in numbers get felt by its citizens.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}