This has always been a difficult task for many. Ask them to write down what they want from life and their money, they can list down so many things. But when asked to prioritize the same they find themselves in fix.

You have limited income and unlimited expenses, which results into a Limited Investible surplus. Now this surplus required to be used in the best possible way so you can have what is important to you and can keep you happy and make your life comfortable.

Listing down the goals is main, but prioritizing is more vital so the surplus can be allocated in the best possible manner. When we try to link the happiness and comfort with what others are having, then that becomes the point where we start diverting from what is important to you.

Saving for Education, buying new car, paying of loans, Retirement, vacations, Own house, Second house, another car, International vacation, home renovation, starting a new business, Inheritance, Kid’s marriage…we want everything.

So what can you do to prioritize the goals, so the investible surplus can be invested effectively? Let’s look at the probable solution

List down all your financial goals which you can think of, and follow the process laid below

Start with WHY: This should always be the first step while you are in the process of prioritizing the goals, mention the reason in front of each goal, as to why you want achieve this goal. What is the motivation behind this goal? Is it intrinsic i.e. coming from within you or Extrinsic i.e. coming from your surroundings? Is this something that you really want or something which you feel you should have because your friends, family expects you to have?

Know What ifs: When you have given a genuine reason and explained the motivation behind each goal, now is the time to look at the potential consequences of achieving or not achieving these goals. These potential consequences are the key determinant of how important a goal is to you.

Do figure out the inter linkages of different goals. For e.g. Child education and Retirement, both may be among the most important goals, and you may have valid “WHY” attached to both, but when it comes to What if analysis, child education can be funded with Education loans, but Post Retirement expenses are something that needs to be arranged/saved for. Also your children would get education loan only if you are in a position to provide collateral or give personal guarantee.

You need to do both “Best case” and “Worst case” analysis, and start with the one with worst potential outcome first.

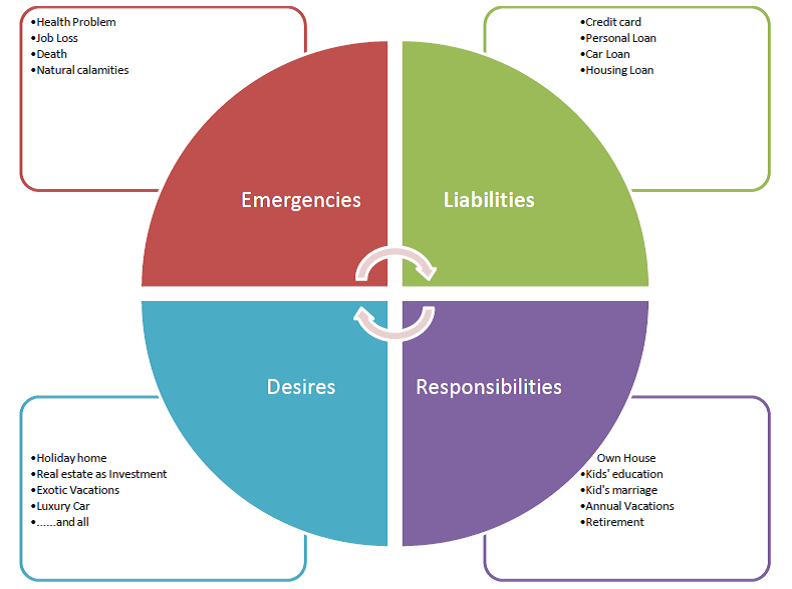

After knowing the WHYs and What Ifs, divide your goals into 4 parts.

- Emergencies

- Liabilities

- Responsibilities

- Desires / Lifestyle choices

If you have more than 1 goal in different heads, you further need to do the Why and What if analysis on those and give serial numbers to them, where 1 being the most important.

Some goals may overlap each other, but you need to be very clear and demarcate them into different heads. Say for e.g. Vacations may be called as Responsibility as you want your kids to go on vacation every year, but International vacation may come into Desire. Every profile and situation is different. That’s why it is said that financial plan cannot work with one size fits all theory.

Here also comes the role of financial plan and understanding of your finances, which will tell you that you should also have financial priorities too. For e.g. in your liabilities section you have different loans including credit card loans, so you need to use your financial wisdom and look at your goals holistically to decide what to do first. Going on Vacations (Desires/Responsibilities) or Closing down your card loan. You need to do “what if analysis” with your financial wisdom or with the help of your financial planner on your emotional priorities set above to come to financial priorities.

This will give you clear picture and action steps on how to distribute your surplus into different heads. Should you divide it equally among all 4 or should you focus on foreclosing the loans and postpone your savings for responsibilities and desires.

Conclusion:

Setting and prioritizing goals is the base of any financial plan. Unless you are clear on this front you will not be able to move forward. Goals should come from within you and not from your surroundings. It should be something that you want, then only you would like to work towards it and strive to achieve the same. And Prioritizing help you to focus on your most important one first.

As the saying goes – “It’s not an issue of Wants and Needs. It’s an Issue of Wants and Priorities”

{kind=link}