With the Franklin, Nippon and UTI Mutual funds paying their Unitholders back the recovery proceeds of Vodafone Idea Security lying in its Segregate Portfolios, queries have started pouring in How will these proceeds be taxed?

(Also Read: What is Segregation or Side-pocketing in mutual funds?)

First you worry on the Investment Returns, then recovery from the segregated portfolio, and after that you worry on the taxes, this is how Debt Investor’s life is going on these days.

Well, Jokes apart. Knowledge of taxation of segregated portfolio is important. And this was cleared in the Budget 2020. This post is to explain to you in simple terms.

Taxation of Segregated Portfolio:

You know that to calculate Capital gains taxes in Mutual funds, you need 3 things

Cost value, Tenure of Investment Holding and Redemption value.

Based on these 3 you calculate if there is gain or loss, and if that gain or loss is short term or long term.

If the holding period is 3 years or less then the Gain in Debt Mutual fund would be Short term and the same will be added in your Total Income and will be taxed accordingly;

and if the holding period is more than 3 years then the Gain would be Long-term and will be taxed at 20% Post Indexation (After March 31, 2023, if you sell debt fund units you purchased, the profits will be added to your income and taxed based on your income tax bracket. But for investments made before March 31, 2023, the tax rate on gains remains at a fixed 20%, and you can continue to take advantage of indexation to account for inflation.)

(Also Read: Taxation of Mutual Funds 2020)

In the case of Segregated Fund Units, to calculate the Holding period, you need to refer the purchase date in the Main Portfolio i.e. from where the Segregate portfolio was Actually created.

For example – You Invested in Franklin Short term bond fund on 01.07.2015, the Segregate portfolio in question was created on 24.01.2020, and the Money Received in your account on 13.07.2020, so in this case, the holding period would be calculated from the date of the first purchase i.e. 01.07.2015

Now, coming to the next aspect i.e. Cost of Investment. Well, technically this would be the proportion of the difference between the NAV the day before and on the date of segregation, like in the above example the difference in NAV of 24.01.2020 and 23.01.2020, multiplied by the cost of first purchase.

For example – Nav on 01.07.2015 (Date of First purchase) = Rs 10; Nav on 23.01.2020 (one day before segregation) = Rs 20; Nav on 24.01.2020 = Rs 18. So, the Cost of purchase of these segregated units would be Rs (20-18)/20*10 = Rs 1.

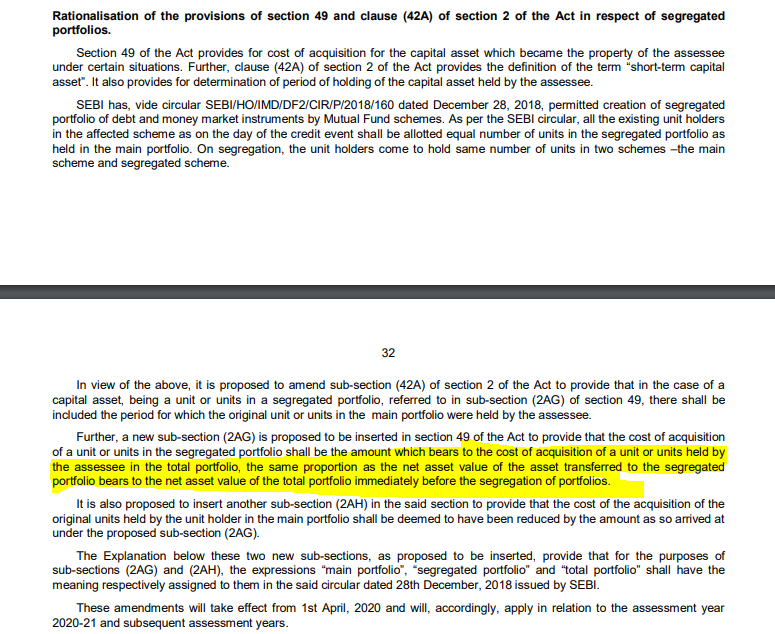

Below is the screen shot of the excerpts from Finance Bill 2020.

Since the Vodafone securities were already marked down in the Respective fund portfolios before segregation, so you do not find any impact on the NAVs after the segregation, but the impact was there in the NAVs on the date of marking down. The email sent by Franklin to the investors also says the same.

The third aspect to calculate the Segregated Portfolio taxation i.e. the redemption proceeds is what you will get in your account post redemption of units.

Now when you have all these 3 details available with you may come up with the Tax.

In the end:

Please note that this article on segregate portfolio taxation is for general understanding purpose, as you can get the cost of Investment, and even capital gain details from the AMC concerned. So, there’s no need to get into such a detailed calculation. However, it may be required to explain to your Tax professional or even for you to do the cross-checking with the AMC records for the first time (If you want).

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

Dear sir,

What will be the ‘purchase price’ in Segregated Portfolio as cost of acquisition is ‘0’ , For the purpose of filing Income tax return?

If the cost of Acquisition is ‘0’ it implies that you are mentioning about Franklin funds. In this case, the whole amount received by you against this segregated portfolio would be taxable in your hands, that too under short-term capital gains. For others, you may refer to the fund statements, there the cost of acquisition should be mentioned.