Reliance Mutual funds has recently come up with Reliance retirement fund. This fund will reopen for further subscriptions from Feb 20’2015. This Reliance Retirement fund is the first in its category. This is the first notified retirement oriented fund, which also has equity oriented scheme. Pension mutual funds already available in market (UTI, Franklin) do not give much of equity exposure which is advisable to have at least in accumulation stage. Reliance Retirement fund is also an answer from mutual funds to the Insurance pension Plans. Let’s go through what this fund is all about, how it works and does it make sense to go with this structure.

Reliance Retirement fund – In short

Retirement planning is something which doesn’t require any explanation at least to the regular readers of this blog. I consider this as most important aspect in financial planning. Till date this space had been occupied by Insurance companies (at least specific product wise) through their pension plans (Read: Retirement Plan is not only about buying Pension Plan). But Now Mutual fund companies have also been allowed to come up with their products for this segment. Reliance Mutual fund is the first one to have launched such scheme. Soon you will see products from SBI, AXIS and other AMCs too.

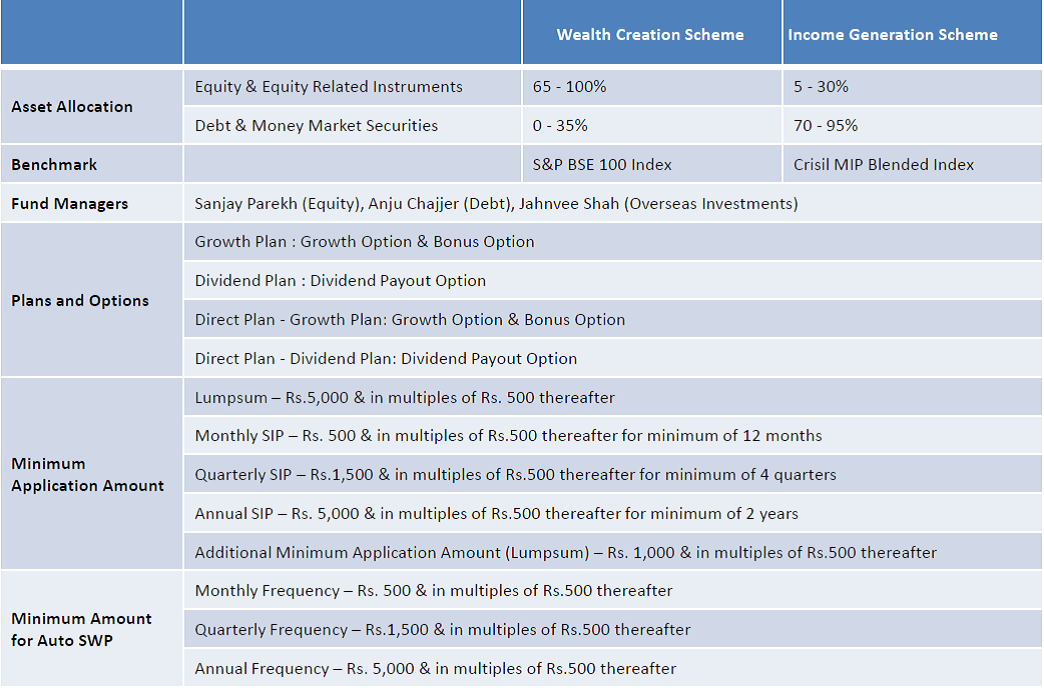

Reliance Retirement fund is an open ended notified tax savings cum pension scheme with no assured returns. It has 2 scheme options. One is with high equity exposure i.e. 65%-100% known as Wealth creation scheme and other is with high debt exposure i.e. 70%-95% in debt and money market securities known as Income generation scheme.

The idea behind these 2 schemes is to stay in equity at accumulation stage and move into debt in distribution stage. But this is up to investor to select whichever scheme she wants. There are unlimited switches between these two schemes.

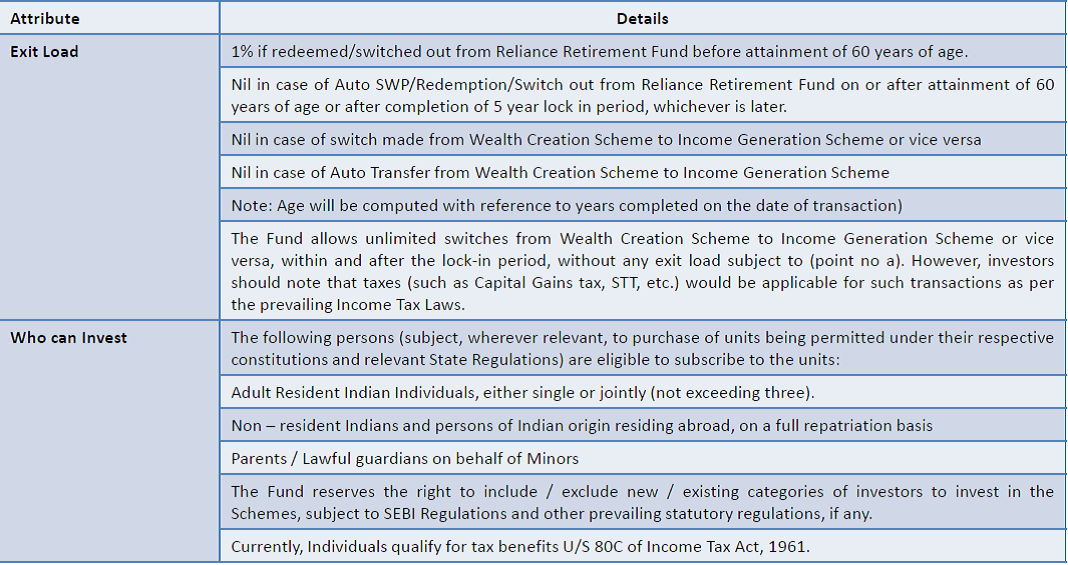

With a Lockin period of 5 years, there’s exit load of 1% on redemption before age of 60. Reliance Retirement fund is notified for tax saving u/s 80C up to maximum limit of Rs 1.50 lakh per year.

Reliance Retirement Fund – Some important terms and associated features

1. AUTO Transfer: It is an optional facility where in investor’s entire investment shall be switched automatically from Wealth creation to Income generation scheme at any date specified by Investor (within or after the lock in period) or after completion of 50 years of age.

2. AUTO SWP: This is an optional facility aims to provide a regular inflow of money to investors (monthly/quarterly/annual) by automatic redemption of units on or after 60 years of age.

Analysis shows that SWP in debt oriented funds actually proves to be a tax efficient way of income generation. (Read: MIP works best with SWP)

3. Step up facility: This is a facility where investor has option to increase the amount of SIP installment by a fixed amount at predefined intervals.

Reliance Retirement Fund – Other key features

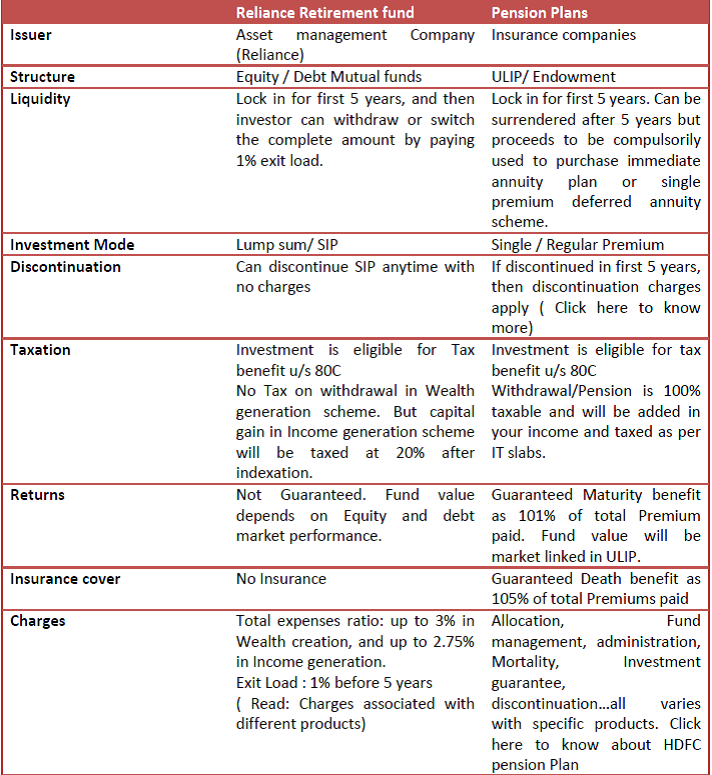

Reliance Retirement fund Vs. Insurance Pension Plan

Reliance retirement fund has come up as a direct competition with Insurance pension plan and also New pension scheme. The word Retirement has the required emotional appeal which is one of the main factors in sale of Insurance pension products ( Also Read : Child Plans in Mutual funds).

To put a comparison between pension plans and Reliance Retirement fund you first have to understand how Pension plans actually works in India.

Reliance Retirement Fund – Should you Invest?

Structure wise I don’t find any specific difference in this scheme and other normal mutual funds. Wealth creation scheme is more or less like Hybrid equity oriented, which may go to 100% equity allocation and Income generation is like Hybrid debt oriented. Packaging of the product with Auto transfer, Auto SWP and unlimited switches makes it attractive for saving towards Retirement.

But I still think that the investments structure under Retirement plan should be customized as per one’s requirement, tax profile, and other cash flow needs. You can have mix of different products which are flexible enough to manage, allocate and reallocate. The SWP, and Transfer features are available separately too which can be used if required, otherwise at distribution stage there are many other different products which can be used for regular income generation.

In nutshell, I believe that it’s better to keep the things simple and one should make his own structure towards goal achievement with less number of products. Reliance Retirement fund will suit those who needs an emotional appeal while investing and staying in the fund as this will also bring the necessary discipline in the investments. But for others who have a set structure and understanding of their personal finance is at place, they should consider open ended diversified equity and debt funds along with other instruments like PPF, EPF towards retirement goal.

Hope this review will help you in decision making. How did you find Reliance retirement fund? do share your opinion or ask any question in the comments section below.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

I m a businessmen I find this fund is very attractive because I will not get any pension from any body so I have to strictly invest some money for my retirement because of lockin and 1 exit load I have to invest this money till my 60 after that I can enjoy my retirement life with that money

Its good to know Rohan that you are concerned about your Retirement. But may i know why this particular fund, when you can plan your retirement through other open ended and well structured funds too?

Great work Manikaran Sir … The features of Reliance Mutual Fund is simple attractive and not so many rules and regulations too. But I’m unable to get your point i.e. Auto Transfer feature. What exactly it means and how it is beneficial for us. Can you explain us little bit more ???

Auto Transfer is an optional facility wherein investors’ entire investment (Lump sum/SIP) shall be switched automatically from Wealth Creation Plan to Income

Generation Plan (with nil exit load) at any date as specified by the investor (which is within or after the lock-in period) or upon completion of 50 years of age.

As a general rule one should be less on equity when nearing the goal, so this auto transfer will help in automatically moving the funds from equity to debt (income ) portion as per your planned date or upon 50 years of completion